Definition & Meaning

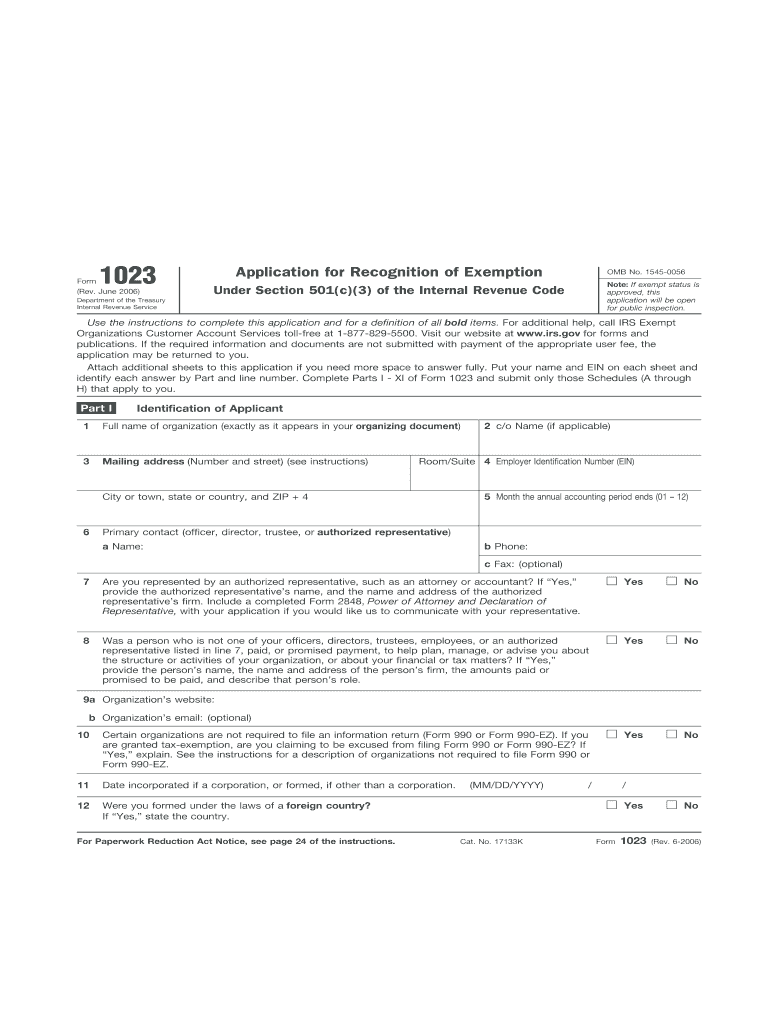

The 2 Form is an application used by organizations seeking recognition of exemption under Section 501(c)(3) of the Internal Revenue Code. This form is essential for entities that aim to qualify for tax-exempt status, indicating their charitable, educational, scientific, or religious purposes. The form provides a comprehensive overview of the organization’s structure, governance, financial details, and planned activities to meet IRS requirements for tax exemption. By completing this form, organizations demonstrate their commitment to fulfilling specific legal criteria to operate as a nonprofit entity in the United States.

Steps to Complete the 2 Form

-

Organization Information: Start by providing basic details about your organization, such as its name, address, and date of incorporation.

-

Purpose Statement: Clearly articulate the organization's primary purposes in alignment with the exemption criteria outlined by the IRS, such as charitable or educational activities.

-

Financial Data: Include a detailed financial statement covering the current fiscal year and projected budgets, which help understand income sources and budget allocation.

-

Governance and Management: Provide information on the organization's board members and executives, demonstrating effective governance practices.

-

Public Charity Status: Determine the public charity status by selecting the appropriate reason for exemption based on the organization's contributions and income type.

-

Narrative Description of Activities: Create a narrative that describes the organization's activities and how they support its nonprofit purposes.

-

Attachments and Schedules: Be prepared to include additional schedules and attachments, such as detailed financial data, conflict of interest policies, or additional narrative descriptions as necessary.

Important Terms Related to 2 Form

-

Tax-exempt Status: The status granted to nonprofit organizations under IRC Section 501(c)(3), allowing them to be exempt from federal income tax.

-

Filing Requirements: Various mandatory disclosures and documentation that organizations must submit along with Form 1023 to qualify for exemption.

-

Conflict of Interest Policy: A policy outlining how potential conflicts of interest will be managed within the organization, which might be required depending on its activities.

-

Public Support Test: A calculation used to determine whether a nonprofit organization receives sufficient public support to qualify as a public charity.

-

Advance Ruling: Previously a method to conditionally hold public charity status for a defined period, now phased out in favor of using a definitive approach based on actual support metrics.

IRS Guidelines for the 2 Form

The IRS provides specific guidelines to assist applicants in completing the 2 Form accurately. These guidelines explain the eligible activities, the criteria for public charity or private foundation status, and details on required financial data and organizational history. They also highlight the importance of thorough documentation and transparency in declarations, aiming to prevent errors that could delay approval or result in denial of the application. The guidelines support organizations in gaining recognition efficiently by adhering to updated regulations and submission standards.

Filing Deadlines / Important Dates

Although there is no strict deadline for submitting Form 1023, applicants are encouraged to file within 27 months from the date of incorporation to be recognized as tax-exempt from the date of formation. Filing after this period might lead to tax-exempt status being granted from the date of the application only. Monitoring timelines ensures that an organization remains compliant and reaps the full benefits of tax exemption swiftly. Additionally, it's advantageous to stay aware of the IRS processing times for approval.

Eligibility Criteria

To be eligible for filing the 2 Form and receiving tax-exempt status, organizations must operate exclusively for the purposes stipulated under Section 501(c)(3). They must not substantially engage in legislative or political campaigns and are required to serve public interests rather than private. Meeting these criteria is essential to qualify for the benefits of a tax-exempt entity, such as receiving tax-deductible donations and potentially being exempt from certain state taxes.

Penalties for Non-Compliance

Organizations failing to comply with the requirements of Form 1023 may face severe penalties, including the revocation of their tax-exempt status. Inaccurately reporting financial data or engaging in prohibited activities such as excessive lobbying can trigger these penalties. Nonprofit organizations face the risk of paying taxes on previously exempt income and potential fines if they do not rectify compliance issues promptly. Adhering to accurate and reliable filing procedures is crucial to avoid such repercussions.

Application Process & Approval Time

The application process begins with complete preparation of all required materials and submission to the IRS for review. Once received, the IRS examines the completeness and correctness of the information provided. Approval times may vary, but organizations generally receive a determination within three to six months. Real-time tracking of the application status helps organizations anticipate when they might need to provide additional information or clarification for successful exemption approval.