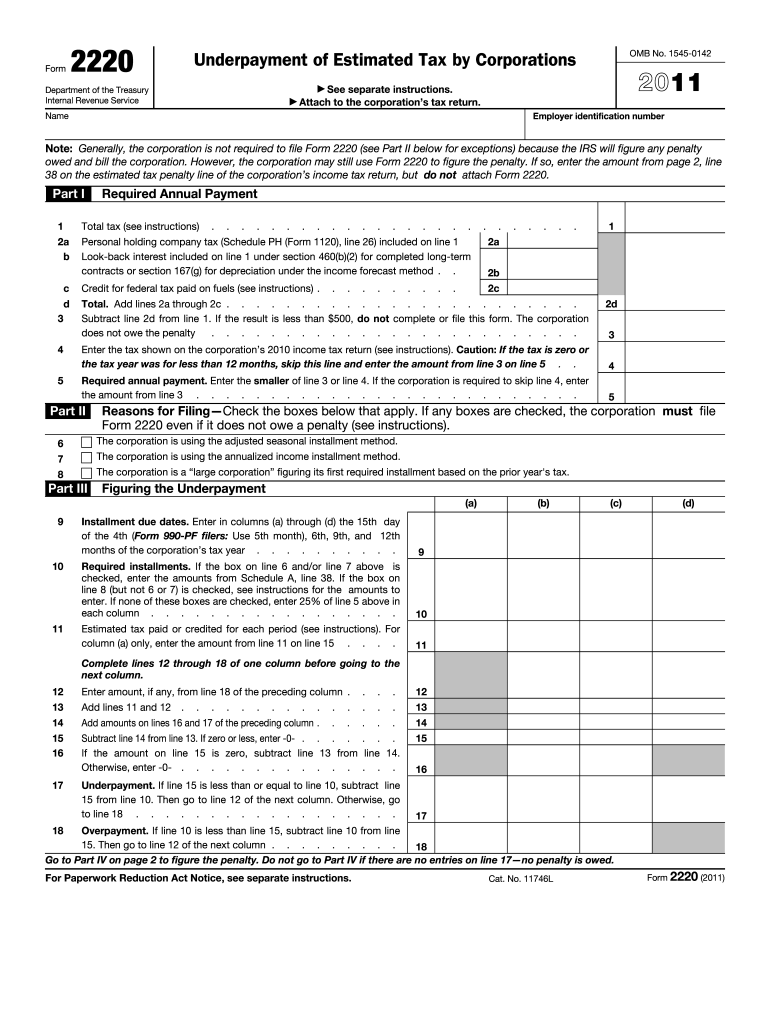

Definition and Purpose of the 2011 IRS Form Estimated Tax

The 2011 IRS Form Estimated Tax is a crucial document for taxpayers who need to make periodic tax payments throughout the year, rather than waiting until the annual tax return deadline. This form is primarily used to report and pay estimated taxes on income that isn't subject to withholding, such as earnings from self-employment, interest, dividends, and rental income. The key purpose of this form is to help individuals avoid penalties for underpayment of taxes by calculating the appropriate amounts to be paid quarterly.

How to Use the 2011 IRS Form Estimated Tax

Using the 2011 IRS Form Estimated Tax involves calculating your expected annual income and the associated tax liability. You'll need to:

- Determine your estimated gross income for the year.

- Calculate deductions and credits you are eligible for.

- Apply the relevant tax rates to estimate your total tax liability.

- Divide your total estimated tax by four to determine the quarterly payment amounts.

These steps ensure that your quarterly payments align with your projected tax obligations, reducing the risk of underpayment penalties.

Steps to Complete the 2011 IRS Form Estimated Tax

Completing the form requires attention to detail and accuracy. Follow these steps for successful completion:

- Gather Financial Information: Collect details of all income sources that are not subject to withholding.

- Calculate Adjusted Gross Income (AGI): Use projections and past data to estimate your AGI.

- Determine Deductions and Credits: Consider all possible deductions like student loan interest and credits such as the Child Tax Credit.

- Compute Tax Liability: Use the estimated AGI, deductions, and credits to calculate the expected tax using the prescribed tax rates.

- Allocate Payments: Divide the calculated tax by four for equal quarterly payments.

These steps ensure that you consistently manage your tax obligations throughout the year.

Key Elements of the 2011 IRS Form Estimated Tax

Understanding the form is easier when you know its critical components:

- Identification Information: Includes taxpayer name, address, and Social Security number.

- Income Estimates: Sections for reporting various income types and expected amounts.

- Deductions and Credits: Fields to input estimated deductions and tax credits.

- Payment Calculations: Worksheets provided to calculate estimated taxes and quarterly payments.

- Payment Vouchers: For mailing payments to the IRS.

Each element helps structure the taxpayer’s financial information for accurate tax payment.

Filing Deadlines and Important Dates

For the 2011 tax year, the IRS set the following deadlines for making estimated tax payments:

- April 15, 2011, for the first quarter.

- June 15, 2011, for the second quarter.

- September 15, 2011, for the third quarter.

- January 15, 2012, for the fourth quarter.

Meeting these deadlines helps avoid late payment penalties. It's advisable to mark these dates well in advance to ensure timely compliance.

Penalties for Non-Compliance

Failing to file or pay estimated taxes on time can result in penalties. The IRS may assess penalties if:

- Payments are late, even if calculated amounts are correct.

- The total tax liability by year end exceeds the withholding and estimated tax payments.

- The withheld amount and estimated payments are less than the lesser of 90% of the tax liability for the year or 100% of the tax shown on the prior year's return.

Being aware of these penalty conditions helps taxpayers avoid fines and interest charges.

Who Typically Uses the 2011 IRS Form Estimated Tax

This form is most commonly used by:

- Self-employed individuals with no withholding from payroll.

- Investors with substantial interest, dividend, or capital gains income.

- Retirees with significant, non-withheld pension or annuity income.

- Corporate taxpayers and partnerships required to make estimated tax payments.

Understanding who uses this form aids in determining applicability to one's personal tax circumstances.

Important Terms Related to the 2011 IRS Form Estimated Tax

Familiarize yourself with these essential terms:

- Adjusted Gross Income (AGI): Total income minus adjustments.

- Tax Liability: Total tax owed for the year after deductions and credits.

- Quarterly Payments: Payments divided into four installments.

- Underpayment Penalty: Fine for not paying enough taxes through withholding or estimated payments.

Grasping these terms ensures a clearer comprehension of form requirements and tax obligations.