Definition and Purpose of Form 2

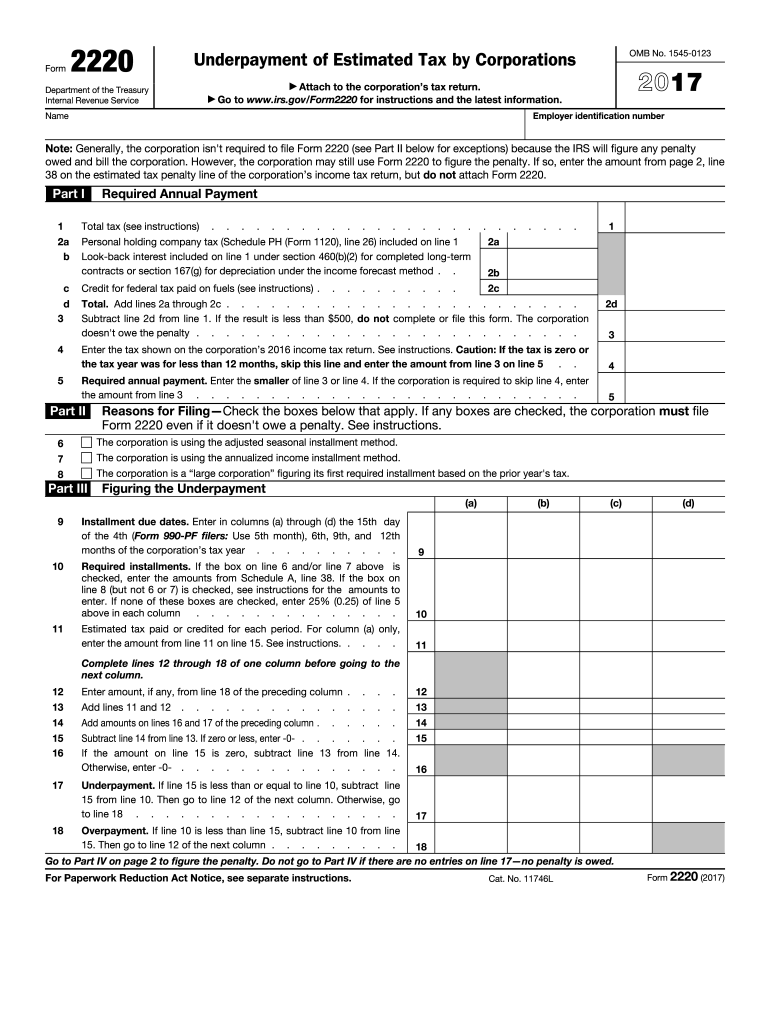

Form 2220 for the year 2017 is utilized by corporations to report underpayment of estimated tax. Designed by the IRS, the form determines any penalties related to underpayment, calculating based on criteria such as required annual payments, installment due dates, and penalties for late or insufficient payments. The form is essential for organizations to remain compliant with federal tax obligations and to avoid potential fines stemming from underpayments.

Steps to Complete Form 2

- Calculate Estimated Tax: Begin by determining the estimated tax due for the year, factoring in anticipated income, deductions, and credits.

- Calculate Required Annual Payment: Use Part I of the form to compute the required annual payment, based on last year’s tax or 100% of this year’s anticipated tax.

- Assess Installment Due Dates: On Part II, determine the due dates for each installment in line with IRS guidelines, including any quarter-specific payments.

- Determine Underpayment: Record any instances where installments have not met the required payments. This is essential for evaluating potential penalties.

- Calculate Penalties: Use the final sections of the form to calculate penalties based on the amount and duration of underpayment, applying IRS-directed interest rates.

Who Typically Uses Form 2

Corporations, including C-corporations, and possibly S-corporations, utilize Form 2 when their estimated tax payments are less than the required amount. The form is particularly crucial for those who regularly experience fluctuating income, which may lead to inconsistent tax estimates. By employing Form 2220, these entities can address discrepancies between their estimated and actual tax obligations, minimizing penalties.

Importance of Filing Form 2

Filing Form 2220 offers several advantages, primarily helping companies avoid penalties associated with tax underpayment. Penalties can accrue quickly, impacting a company's financial stability. By accurately completing and submitting this form, businesses can demonstrate compliance with federal tax laws, thus preserving their financial health and averting legal issues related to tax filings. Additionally, the process fosters accurate financial planning, encouraging businesses to project their tax obligations with greater precision.

IRS Guidelines for Form 2

The IRS provides specific guidelines for completing Form 2220, which must be followed to ensure accuracy and compliance. Key elements include:

- Estimated Tax Calculation: Make sure calculations reflect the current tax year's stipulations.

- Installment Computations: Each payment deadline must correspond with IRS-scheduled dates.

- Annual Payment Requirements: Comply with either a 100% or 110% threshold of the prior or current tax year liability, as outlined by the IRS.

- Penalty Calculation: Apply the established interest rates to any underpayments to determine precise penalty amounts.

Penalties for Non-Compliance

Non-compliance can significantly impact a corporation financially. Penalties typically include interest on underpaid tax amounts, calculated from the due date of the payment until the amount is paid in full. In extreme cases, additional penalties may be imposed if negligence or intentional disregard of payment responsibilities is identified. Therefore, timely and accurate filing of Form 2 is crucial to avoid such repercussions.

Required Documents for Form 2

To accurately complete Form 2220, corporations must gather several essential documents:

- Prior Year's Tax Return: Essential for verifying past tax liabilities and calculating current estimates.

- Current Financial Statements: Provide a snapshot of income, expenses, and potential deductions.

- Records of Any Estimated Payments: Confirm what has been paid within the current tax year.

Ensuring that these documents accurately reflect the corporation's financial situation helps avoid errors in the filing process.

Business Entity Types Using Form 2

Form 2 is relevant for various business structures, primarily those with more complex tax obligations:

- C-Corporations: Typically face significant tax liabilities and require detailed projections of income and expenses.

- S-Corporations: May also use this form when income distribution among shareholders affects estimated payments.

- Multinational Corporations: Often utilize Form 2220 due to diverse income streams and regulatory compliance needs across different jurisdictions.

These entities benefit from using Form 2220 to accurately address estimated tax payment obligations and avoid subsequent penalties.