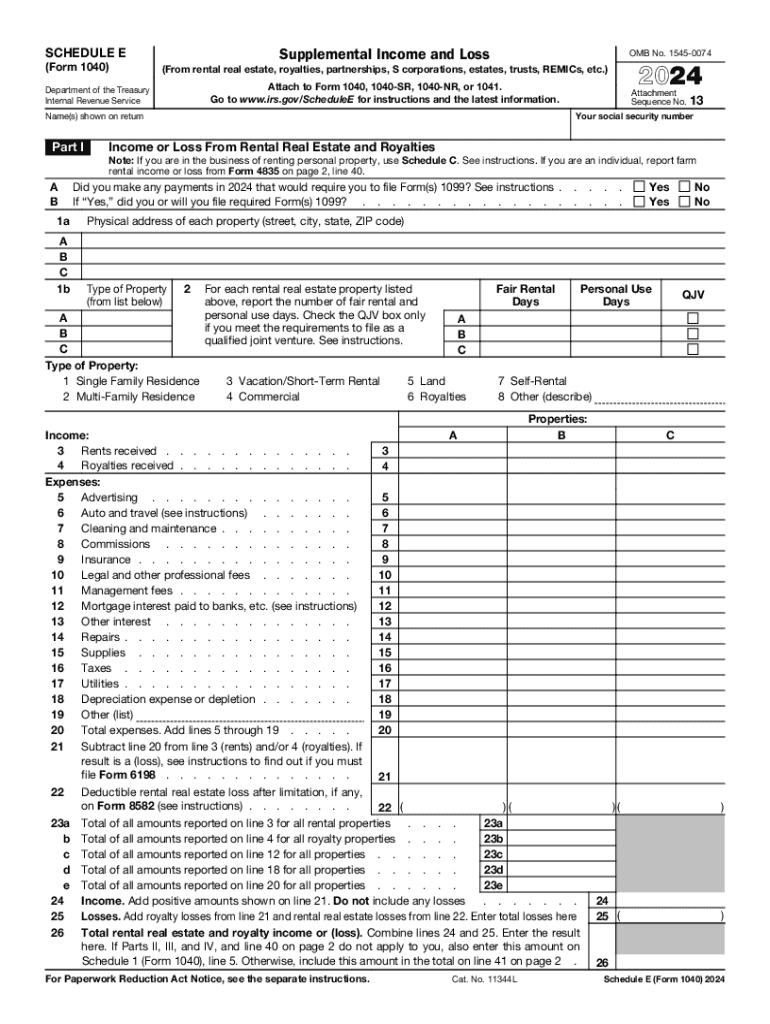

Definition and Purpose of Schedule E (Form 1040)

Schedule E (Form 1040) is designed to report supplemental income and loss that individuals accrue from passive income sources. This encompasses income derived from rental properties, royalties, partnerships, S corporations, estates, and trusts. By providing a structured format, this form allows taxpayers to detail various income sources, related expenses, and losses, ensuring accurate tax reporting. Given its complexity, Schedule E is crucial for those engaged in multiple income-generating activities outside of traditional employment.

Supplemental Income Sources

- Rental Properties: Schedule E reports earnings and expenses from rental real estate, crucial for landlords and property managers.

- Royalties: Income from intellectual property, such as publications or mineral rights, is detailed here.

- Partnerships and S Corporations: Distributions from business entities are recorded, reflecting an owner's share of profits or losses.

- Estates and Trusts: Beneficiaries receiving distributions from these sources must include them in their income.

Steps to Complete Schedule E

To accurately report supplemental income and losses, taxpayers must follow specific steps:

- Gather Required Documents: Collect statements, receipts, and financial records related to all supplemental income sources.

- Fill Out Part I for Rental Income: Here, you document income and deductible expenses associated with real estate properties.

- Complete Parts II through V for Other Income: Use these sections to report income from royalties, partnerships, and trusts.

- Calculate Total Income and Expenses: Add up all sources and related deductible expenses to ascertain your net income or loss.

- Transfer Data to Form 1040: Once completed, transpose the figures from Schedule E to the appropriate lines on your Form 1040.

Practical Example

Consider a taxpayer with two rental properties. Part I of Schedule E would detail each property's income, mortgage interest, property taxes, and repairs. If they also hold a stake in a partnership, Part II would capture that income or loss, alongside the rental figures, to provide a comprehensive supplemental income report.

Key Elements of Schedule E

Several elements within Schedule E are essential to its completion:

- Income and Loss Sources: Segmenting income types ensures clarity in reporting.

- Deductible Expenses: Only authorized expenses, such as mortgage interest and maintenance costs, reduce your taxable income.

- Passive Activity Loss Limitations: Losses from passive activities might be limited under IRS rules, affecting overall tax liability.

Important Terms

- Passive Income: Earnings from activities not actively managed by the taxpayer, like rentals and investments.

- Material Participation: A concept differentiating active involvement in trade or business from passive activities.

IRS Guidelines and Requirements

Abiding by IRS guidelines is crucial when utilizing Schedule E:

- Documentation: Maintain meticulous records of all transactions, ensuring support for entries made on the form.

- Meet Filing Deadlines: Adherence to IRS deadlines is essential to avoid penalties.

- Use the Most Current Form Version: Tax laws change; employing the latest form is crucial to compliance.

Filing Deadlines

Generally, Schedule E should be filed alongside your Form 1040 by the April tax deadline. Extensions may be available, but late submissions without them attract penalties.

Penalties for Non-Compliance

Non-compliance with Schedule E requirements can manifest as:

- Monetary Penalties: Fines for underreported income or unfiled taxes.

- Interest Charges: Accruing on any unpaid taxes from the original due date.

Avoiding Penalties

Proactively managing your records, seeking professional advice, and double-checking entries can mitigate the risk of penalties. Ensuring full and accurate reporting will align with IRS standards and prevent unnecessary costs.

Digital vs. Paper Submission

The decision between digital or paper submission:

- Digital Submission: Allows quick processing and immediate submission confirmation, often seen through IRS e-filing systems or via tax software like TurboTax.

- Paper Filing: While reliable, it entails longer processing times and is more error-prone.

Software Compatibility

Software solutions simplify Schedule E completion, offering step-by-step guidance and real-time error checks. TurboTax and QuickBooks are popular choices, though it's crucial to verify compatibility with the latest IRS requirements.

These comprehensive guidelines ensure that taxpayers efficiently navigate IRS Schedule E, accurately reporting their supplemental income and adhering to federal tax obligations.