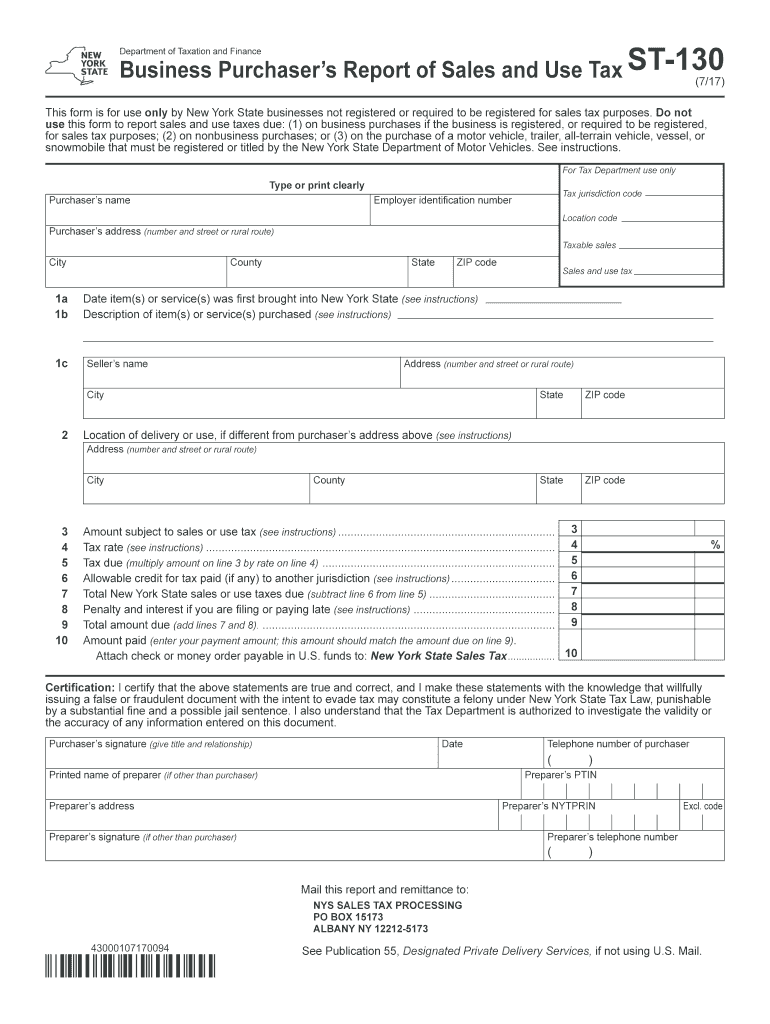

Definition & Meaning

The "Use Tax and Casual Sales Forms - Department of Taxation and Finance" are essential documents used by individuals and businesses in the U.S. to report and remit use taxes on purchases where sales tax was not collected by the seller. Use tax comes into play typically when goods are purchased outside the taxpayer’s state of residence and brought back for use. This form helps ensure compliance with state tax laws and helps states capture revenue from these transactions to fund public services.

Understanding Use Tax

-

What is Use Tax?

Use tax is a levy assessed on goods purchased without sales tax applied. It is similar to sales tax and applies when a taxpayer buys goods from an out-of-state seller. -

Key Differences from Sales Tax:

Use tax is self-assessed and applies to the use, storage, or consumption of goods within the state, whereas sales tax is collected by the retailer at the point of sale.

How to Use the Use Tax and Casual Sales Forms

Utilizing the Use Tax and Casual Sales Forms correctly is essential for compliance and accurate tax reporting. Follow these steps to effectively use the form:

Step-by-Step Instructions

-

Identify Eligible Transactions:

Determine which purchases are subject to use tax. Typically, these are out-of-state or online transactions where no sales tax was collected. -

Document Transaction Details:

Record the date, nature, and amount of each taxable purchase. Provide vendor information and describe the items purchased. -

Calculate Use Tax Due:

Apply your state's use tax rate to the total purchase amount to compute the tax owed. -

Complete the Form:

Fill out the required information on the form, ensuring all fields are accurately completed to avoid errors. -

Submit the Form:

Follow state-specific guidelines to file the form—options may include online submission, mailing, or in-person delivery to the Department of Taxation and Finance.

Steps to Complete the Use Tax and Casual Sales Forms

Accurate completion of the Use Tax and Casual Sales Forms is critical. Here is a detailed guide to assist in the process:

Detailed Process

-

Gather Necessary Documents:

Collect invoices, receipts, and records of any purchases that may be subject to use tax. -

Access the Form:

Obtain the form from the Department of Taxation and Finance’s official website or from their local office. -

Provide Personal or Business Information:

Enter your name, address, and taxpayer identification number. Businesses need to provide their business tax ID. -

Enter Purchase Details:

List all purchases, their costs, and whether sales tax was paid upfront. Include vendor names and item descriptions. -

Calculate and Enter the Tax Amount:

Use the state-specific tax rate; enter the use tax amount calculated from your purchase totals. -

Review and Submit:

Double-check all information for accuracy. Submit the form along with any payments due.

Important Terms Related to Use Tax and Casual Sales Forms

Understanding terminology associated with the Use Tax and Casual Sales Forms aids in proper form completion and compliance.

Terms to Know

-

Casual Sale:

A sale made by someone not in the regular business of selling goods, possibly triggering use tax obligations if no sales tax was collected. -

Taxable Item:

Any item subject to either sales or use tax under state laws. -

Retail Sale:

Sale of goods or services to consumers, contrasted with wholesale sales exempt from use tax.

Penalties for Non-Compliance

Failing to comply with use tax obligations can result in significant consequences. Here are potential penalties:

Consequences

-

Fines and Penalties:

Late or non-payment can lead to financial penalties, including fines proportional to the overdue amount. -

Interest Charges:

States typically assess interest on any unpaid taxes, increasing the amount owed over time. -

Legal Repercussions:

Persistent non-compliance may result in legal actions, potentially impacting credit or business operations.

IRS Guidelines

While primarily a state-level requirement, IRS guidelines provide best practice standards for record keeping and tax compliance:

IRS Recommendations

-

Record Keeping:

Maintain detailed records of all purchases potentially subject to use tax, including invoices and receipts. -

Regular Reviews:

Conduct periodic checks to ensure all eligible transactions have been reported and paid accurately.

Form Submission Methods

Multiple submission methods ensure flexibility and convenience for taxpayers:

Submission Options

-

Online Filing:

Use state-provided online portals to submit the form digitally for faster processing. -

Mail-In Submission:

Fill out the form manually and mail it to the designated state department address. -

In-Person Filing:

Visit a local tax office to submit the form and any payments directly.

Business Entity Types

Different business structures may impact use tax responsibilities:

Implications for Different Entities

-

LLCs and Corporations:

These entities may have more extensive reporting obligations due to the volume of transactions. -

Sole Proprietors:

May encounter use tax mainly for business-related out-of-state purchases. -

Partnerships:

Must coordinate tax responsibilities among partners to ensure comprehensive compliance.

By adhering to these guidelines and utilizing the Use Tax and Casual Sales Forms effectively, taxpayers can maintain compliance with state tax regulations and avoid potential penalties.