Definition & Meaning

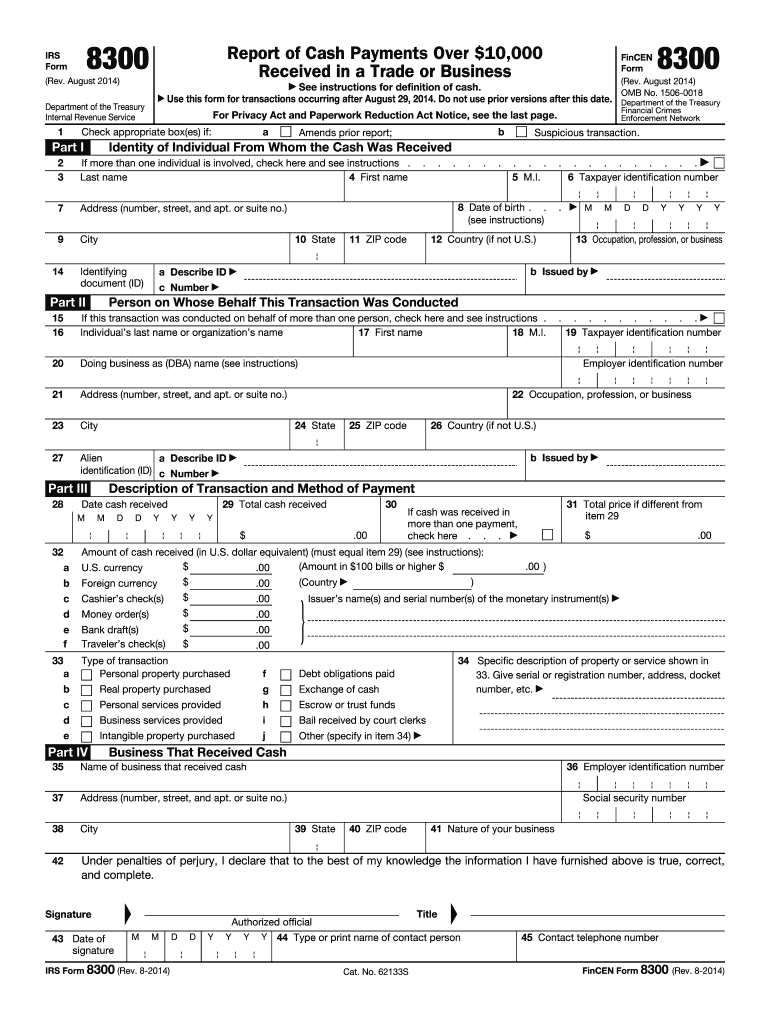

Form 8300 is an official IRS form used to report cash payments exceeding $10,000 received in a trade or business. Filing this form is a legal requirement aimed at monitoring significant cash transactions to prevent money laundering and tax evasion. Businesses must report details about both the transaction and the parties involved, providing critical data for the IRS and FinCEN to identify potential financial abuses. This not only helps the authorities track large sums of cash in the economy but also reinforces businesses' commitment to legal and ethical financial reporting.

How to Use the Form 8300

Businesses use Form 8300 to document and report any large cash payments. This includes payments received in single transactions or in related transactions over a 12-month period. When a business receives over $10,000 in cash—whether in one payment or a series of related payments—it must accurately complete and file Form 8300. The form requires detailed information about the payer, recipient, and the nature of the transaction. It's essential for businesses to understand that this form is not only a compliance tool but also a measure of transparency and integrity in financial operations.

Steps to Complete the Form 8300

-

Gather Required Information: Before filling out the form, collect pertinent details about the transaction and involved parties. This includes the payer's name, address, and taxpayer identification number (TIN).

-

Fill Out Identification Sections: Accurately provide information about both the business and the person making the payment. Ensure all identifiers such as TINs are correct to avoid penalties.

-

Describe the Transaction: Clearly outline the nature, purpose, and amount of the transaction. This section is critical for IRS reviews.

-

Submit the Form Promptly: The form must be filed within 15 days of receiving the payment. Late filing can lead to penalties.

-

Retain a Copy: Keep a copy of the filed form for at least five years as it may be necessary for future audits or regulatory checks.

Key Elements of the Form 8300

- Payer Information: Includes full name, address, and TIN.

- Transaction Details: Amount, date(s), and description of the transaction.

- Business Information: Reporting company's name, address, and EIN.

- Purpose of Payment: Detailed explanation of why the payment was made, which helps differentiate between legitimate and suspicious activities.

Each element must be correctly filled to ensure compliance and avoid penalties. Businesses should also ensure that all information is consistent with what has been reported in other financial documents submitted to the IRS.

Legal Use of the Form 8300

Legally, Form 8300 serves as a tool against illegal financial activities. When a business files this form, it aligns with federal regulations designed to detect and deter criminal enterprises, money laundering activities, and tax evasion. Failure to comply with the reporting requirements of Form 8300 can result in hefty fines and legal challenges. It's critical for businesses to understand the legal implications of non-compliance, which can also tarnish their reputation.

Who Typically Uses the Form 8300

Form 8300 is commonly used by businesses that frequently handle large cash transactions. This includes but is not limited to car dealerships, real estate agencies, jewelry stores, and other retail businesses that may receive significant cash payments. It is particularly relevant for companies in industries prone to large cash dealings, helping them maintain legitimacy and prevent legal issues tied to unreported transactions.

Filing Deadlines / Important Dates

The IRS mandates that Form 8300 must be filed within 15 days of the cash transaction. If additional related transactions with the same party accumulate to over $10,000 within a one-year span, a new 15-day period begins from the date the total goes over $10,000. This tight deadline underscores the importance of timely and accurate reporting.

Penalties for Non-Compliance

Non-compliance with Form 8300 requirements results in several potential penalties, including:

- Failure to File: Civil penalties for not filing or for filing late can be up to $100,000.

- Intentional Disregard: If the failure to file is deemed intentional, fines increase substantially.

- Criminal Penalties: Severe cases can lead to criminal charges, with the potential for fines or imprisonment.

Businesses must prioritize timely and correct filings to avoid these significant consequences. Keeping accurate records and setting up reminders can help ensure compliance with IRS mandates.

IRS Guidelines

The IRS provides comprehensive guidelines on correctly completing and filing Form 8300. These guidelines include detailed instructions on necessary fields, acceptable methods of submission, and maintaining confidentiality. The IRS also outlines protective measures to ensure that shared information does not become public, emphasizing the importance of safeguarding sensitive financial data. Businesses should familiarize themselves with these guidelines to ensure compliance and avoid complications.