Definition and Purpose of the 8300 Form

The IRS Form 8300, used in 2012 and other years, is primarily designed for reporting cash payments over $10,000 in a trade or business. This form is crucial for monitoring substantial cash transactions to prevent money laundering and tax evasion. Businesses that receive cash above this limit must file Form 8300 to provide information about the transaction and involved parties.

How to Obtain the 8300 Form

Securing the 8300 form is straightforward. It can be downloaded directly from the IRS website, ensuring you have the latest version. Businesses can also find it available through tax preparation software or by contacting the IRS directly to have a physical form mailed to them.

Steps to Complete the 8300 Form

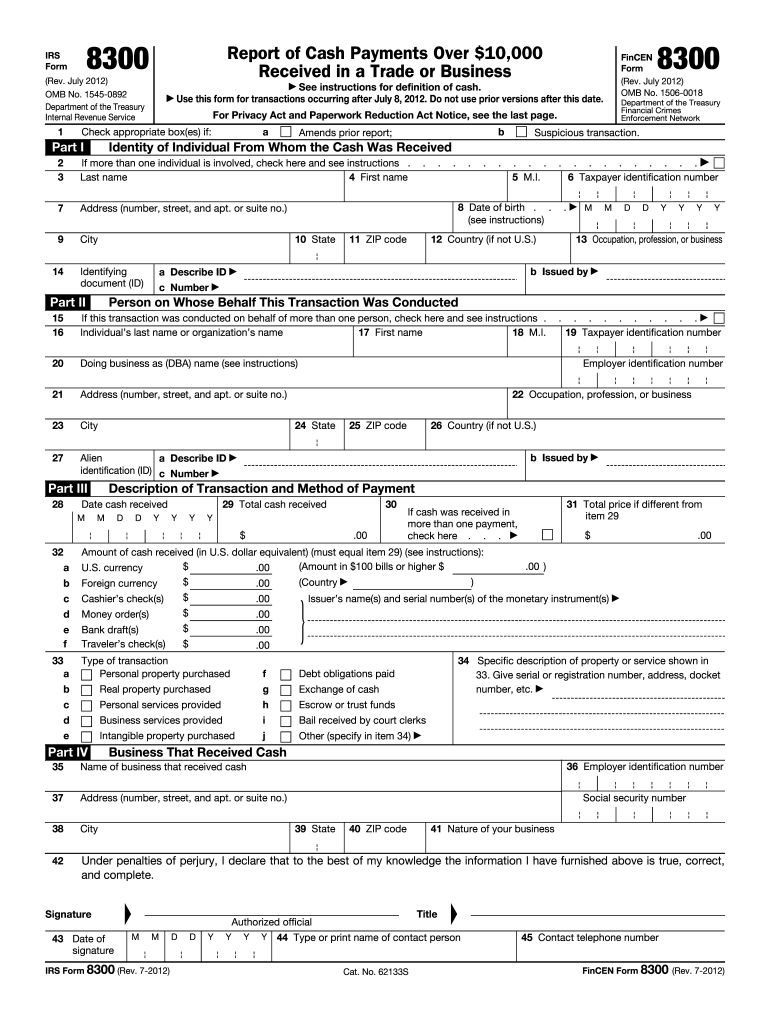

- Identify the Transaction: Ensure the payment exceeds $10,000 and falls within a single transaction or a series of related transactions.

- Provide Transaction Information: Include details such as the date of the transaction and the amount.

- List Each Party: Gather complete information about each individual or organization involved. This includes their name, address, and tax identification number.

- Submit to IRS: File the completed form with the IRS, either electronically or through the mail, as directed in the submission guidelines.

Who Typically Uses the 8300 Form

Common users of the 8300 form include businesses and professionals involved in high-value cash transactions. These range from car dealerships and real estate agents to brokerage firms. Financial institutions like banks and currency exchanges also frequently utilize this form given the nature of their daily operations.

Important Terms Related to Form 8300

- Cash: The term "cash" includes coins and currency of the United States and any foreign country. Cash does not include a check drawn on the payer’s own account.

- Transaction: Defined as a purchase, sale, loan, exchange, etc., that results in paid, received, or loaned funds exceeding $10,000.

- Recipient: The business or individual receiving the cash must report using the 8300 form within 15 days of the transaction.

Penalties for Non-Compliance

Failing to file the 8300 form promptly can result in hefty fines. Penalties range from administrative fines to more severe sanctions if intentional disregard for filing is determined. Timely submission and accurate reporting are essential to avoid these repercussions.

IRS Guidelines

The IRS provides comprehensive guides and support for completing the 8300 form. These include filing instructions and details on what constitutes a cash transaction. It’s recommended to refer to official IRS publications to ensure adherence to their guidelines.

Filing Deadlines and Important Dates

Businesses must file Form 8300 within 15 days after receiving the cash payment. If multiple related transactions occur, each should be treated as a separate event for filing purposes. Documenting and adhering to these key dates protects businesses from penalties and ensures compliance.

Digital vs. Paper Version

The 8300 form can be submitted both digitally and in paper format. Electronic filing is encouraged for faster processing and is supported by several software platforms. However, paper submissions must be printed, filled, and sent via mail to the IRS as outlined in the instructions.