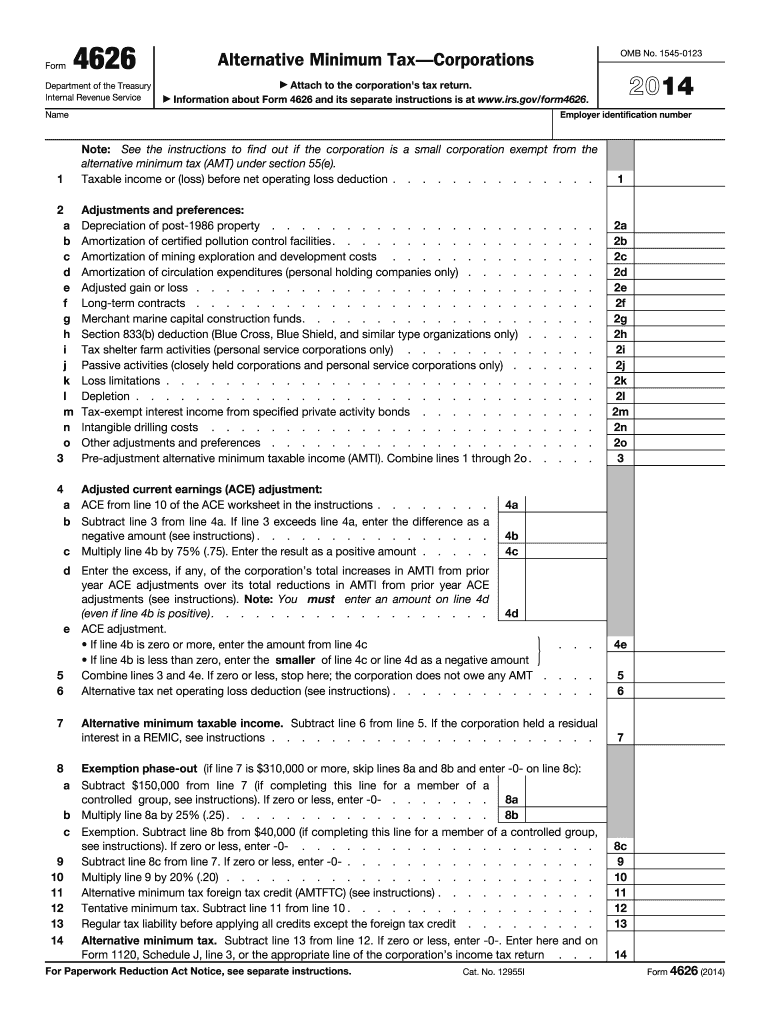

Understanding the 2014 Form 4626

The 2014 Form 4626 is a critical document used by corporations to compute the Alternative Minimum Tax (AMT) for the 2014 tax year. The form helps businesses determine their alternative minimum taxable income (AMTI) and identifies applicable exemptions and credits. This process ensures that corporations meet their tax obligations while considering relevant adjustments and preferences.

Definitions and Important Terms

Understanding key terminology is essential when working with Form 4626. Some fundamental terms include:

- Alternative Minimum Tax (AMT): A parallel tax system designed to ensure that companies pay at least a minimum level of tax, even if they have a substantial amount of deductions in the regular tax system.

- Alternative Minimum Taxable Income (AMTI): The taxable income calculated under the AMT system, which includes adjustments and preferences.

- Adjustments and Preferences: These are items that the IRS requires to be recalculated for AMT purposes, potentially leading to a higher taxable income.

How to Obtain the 2014 Form 4626

Corporations can obtain the 2014 Form 4626 through several methods:

- Download from the IRS Website: The form is available for download as a PDF from the official IRS website.

- Tax Software: Tax preparation software, such as TurboTax or QuickBooks, often includes relevant tax forms, including Form 4626.

- Request by Mail: Businesses can request a physical copy by contacting the IRS directly, although this might take additional time.

Steps to Complete the 2014 Form 4626

Filing the 2014 Form 4626 involves several steps. Here is a comprehensive breakdown:

- Report Taxable Income: Begin by entering the corporation's regular taxable income.

- Calculate Adjustments: Make necessary calculations for adjustments that impact AMTI. This includes depreciation differences and foreign tax credits.

- Identify Preferences: List preferences that need reevaluation, such as tax-exempt interest and income categories requiring adjustments.

- Compute AMTI: Use the adjustments and preferences to compute the AMTI.

- Calculate AMT Exemptions and Credits: Apply any available exemptions or credits that reduce the AMT liability.

- Determine Tax Liability: Compare the determined AMT against regular tax liability to assess if the AMT applies.

Who Typically Uses the 2014 Form 4626

Primarily corporations, particularly those with higher income that may fall into AMT brackets, utilize Form 4626. These companies customarily possess:

- A substantial number of tax deductions.

- Engagement in complex financial transactions leading to large differences between regular taxable income and AMTI.

Key Elements of the 2014 Form 4626

The form consists of essential sections, each serving a unique purpose:

- Section 1: Details corporate income subject to AMT.

- Section 2: Covers key adjustments and preferences necessary for calculating AMTI.

- Section 3: Captures AMT exemptions, credits, and the ultimate tax liability.

Penalties for Non-Compliance

Failure to properly file Form 4626 may result in:

- IRS Penalties: Penalties for underpayment of taxes, which include interest and fees.

- Legal Repercussions: Potential audits and legal scrutiny of corporate financial practices.

- Financial Exposure: Increased costs due to inaccuracies or oversight in tax liability reporting.

IRS Guidelines for 2014 Form 4626

Corporations must adhere to specific IRS guidelines when completing Form 4626. Key points include:

- A detailed review of IRS instructions specifically related to AMT.

- Ensuring all calculations, preferences, and adjustments are accurately reported.

- Understanding the implications of exemptions and maintaining proper documentation as proof.

Important Filing Deadlines

Corporations must be conscious of applicable filing deadlines for the 2014 tax year. Key dates include:

- Regular Filing Deadline: Generally April 15th, unless extended.

- Extensions: Available upon request, though interest on any unpaid taxes may accrue.

By maintaining comprehensive records and ensuring adherence to IRS guidelines, corporations can effectively manage their AMT obligations using the 2014 Form 4626.