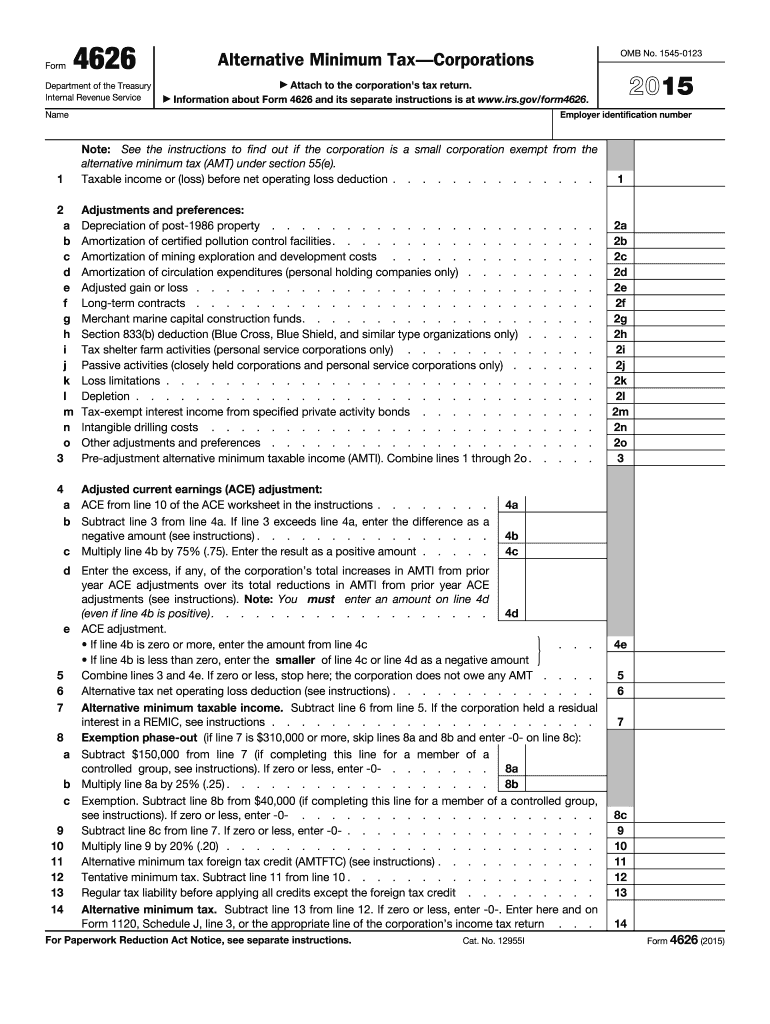

Definition and Purpose of the 2015 Form 4626

Form 4626, officially known as the Alternative Minimum Tax — Corporations, is used by corporations to compute their Alternative Minimum Tax (AMT). This form is essential because it ensures that corporations with significant income do not escape tax liabilities by using exclusions, deductions, and credits available under the regular tax system. The AMT serves as a parallel tax calculation that overrides traditional income tax calculations if the AMT amount is greater, thus requiring corporations to pay the higher of the two.

How to Use the 2015 Form 4626

Corporations use the 2015 Form 4626 to report taxable income adjustments and preferences. This includes changes necessary for AMT due to limitations and exclusions. Corporations begin by calculating their regular taxable income, and then make adjustments for AMT purposes, reporting these changes on various lines within Form 4626. The form ultimately computes the corporation's AMT liability, determining the additional tax owed beyond regular tax obligations, if applicable.

Steps to Complete the 2015 Form 4626

-

Calculate Regular Taxable Income:

- Start with the corporation's taxable income as determined under regular taxation rules.

-

Compute Adjustments and Preferences:

- Adjust based on differences such as depreciation methods, depletion deductions, and percentages in completion method gain calculations.

-

Determine Alternative Minimum Taxable Income (AMTI):

- AMTI is calculated by adding back any preference items and adjustments to regular taxable income.

-

Compute Tentative Minimum Tax:

- Apply the AMT rates to the AMTI.

-

Determine AMT Liability:

- Subtract any available AMT credits from the Tentative Minimum Tax to find the final AMT liability.

-

Compare with Regular Tax:

- If AMT liability exceeds regular tax, the corporation must pay the difference.

Important Terms Related to 2015 Form 4626

- Alternative Minimum Tax (AMT): A parallel tax system designed to ensure that corporations pay at least a minimum level of tax.

- Preference Items: Certain income, deduction, or credit items that are subject to adjustment under AMT rules.

- AMTI (Alternative Minimum Taxable Income): Regular taxable income adjusted for AMT adjustments and preferences.

Filing Deadlines and Important Dates for the 2015 Form 4626

-

Regular Filing Deadline for Corporations:

- Generally due by the 15th day of the third month after the end of the corporation's tax year.

-

Extensions:

- Corporations can file for a six-month extension to postpone the submission.

-

Payment Due Date:

- Taxes calculated using Form 4626 must be paid by the original filing deadline to avoid penalties and interest on unpaid amounts.

Required Documents for the 2015 Form 4626

- Income Statements: To determine primary taxable income.

- Adjustments and Preferences Worksheets: For specific AMT adjustments.

- Depreciation Schedules: Necessary for recalculating income for AMT adjustments.

Form Submission Methods

-

Online Submission:

- Can be electronically filed using tax preparation software that supports IRS form submissions.

-

Mail Submission:

- Paper forms can be printed, filled, and sent to the IRS mailing address provided in the instructions.

-

In-Person Filing:

- Although less common, submissions can be made in-person at IRS offices.

Who Issues the 2015 Form 4626

The Internal Revenue Service (IRS) is the issuing body for the 2015 Form 4626. It controls the guidelines and instructions for proper completion of the form, ensuring that corporations meet federal tax obligations appropriately.

Penalties for Non-Compliance with Form 4626

Corporations failing to comply with AMT regulations face penalties and interest charges. Non-compliance includes underpayment due to incorrect calculations, failure to file by the deadline, or neglecting to pay taxes owed. Penalties are calculated based on the amount of tax underpaid and the length of the delay.

Examples of Using the 2015 Form 4626 in Practice

-

Example 1: Tech Corporation

- A large tech firm with significant R&D deductions might find that, after adjustments for AMT purposes, they owe additional AMT even when regular tax appears adequately covered.

-

Example 2: Mining Company

- A mining company benefits from depletion deductions but discovers through Form 4626 calculations that AMT adjustments increase taxable income, creating an additional AMT liability.

Understanding these practical applications helps corporations prepare and submit more accurate filings to the IRS, ensuring compliance and avoiding costly penalties.