Definition and Meaning

Form 8832 is critical for eligible entities to establish their classification for federal tax purposes as a corporation, partnership, or disregarded entity. This form is essential for businesses to inform the Internal Revenue Service (IRS) of their chosen tax status. The form provides a structured way to communicate these tax elections and ensures that businesses meet compliance requirements set out by the IRS. Understanding its purpose is crucial for entities aiming to optimize their tax obligations and structure.

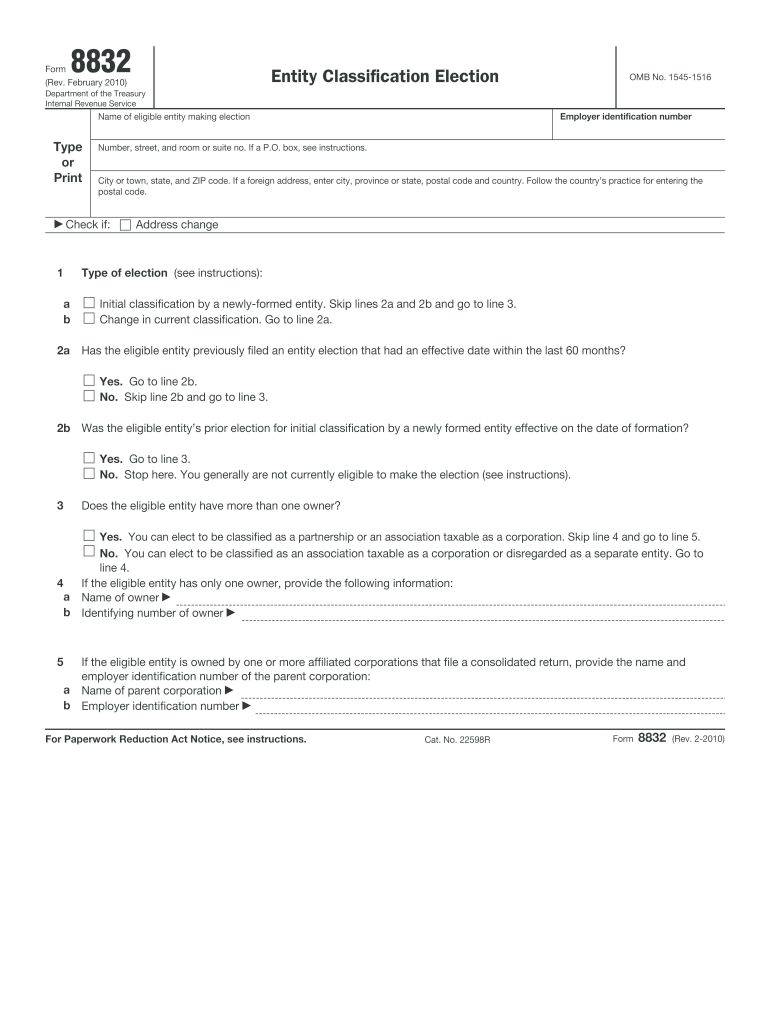

How to Use the 2010 Form 8832

Entities use Form 8832 to make their desired tax classification election. To use the form appropriately, the responsible party must provide the entity's name, address, and employer identification number (EIN). Once completed, the form should detail the type of election being made, including specifying whether the entity is making a new election or correcting a prior classification. Documentation supporting the choice and any previous choices should also be included to maintain a clear record of selections made over time.

Steps to Complete the 2010 Form 8832

-

Obtain Necessary Information: Gather details such as the entity's name, EIN, and the address to correctly fill out the form. Ensure all data is up-to-date to avoid processing delays.

-

Select Tax Classification: Decide whether the entity will be classified as a corporation, partnership, or disregarded entity. Consider consulting a tax advisor to make an informed decision.

-

Complete the Form: Fill out the sections specifying whether this is a new election or a change from a prior selection. Ensure accuracy in all entries.

-

Submit Supporting Documents: Attach any required documents that substantiate the election choice, showing consistency with prior filings if applicable.

-

Mail the Form: Send the completed form to the applicable IRS mailing address as indicated in the instructions. Note that, as of 2010, electronic filing was not an option for Form 8832.

-

Confirm Submission: Retain a copy of the completed form and all attachments for your records. Check for confirmation from the IRS, or correspondence addressing any issues with the submission.

Eligibility Criteria

To use Form 8832, the entity must be eligible under IRS guidelines. Typically, these are domestic or foreign entities like limited liability companies (LLCs), partnerships, and certain corporate structures. Entities must adhere to default classification guidelines unless they opt to elect differently. Specific entities, such as those needing special status for tax purposes, should ensure they meet all eligibility requirements before filing to avoid inadvertent tax implications.

Filing Deadlines and Important Dates

The filing deadline for Form 8832 varies based on entity operations and election timing. Generally, the election should be filed within 75 days from the effective date if choosing a new classification. Businesses need to be mindful of this timeline to ensure the election is valid for the intended tax period. Late elections may result in penalties if approval is not sought and granted by the IRS.

Legal Use and Compliance

Form 8832 must be used in compliance with U.S. tax laws. This means that entities must adhere to the guidelines governing federal tax classifications and submit the form accurately and timely to avoid legal issues such as penalties or misrepresentation of tax status. Legal compliance necessitates that all fields on the form be filled out truthfully and that the entity complies with any IRS requests or follow-up actions.

IRS Guidelines

The IRS stipulates detailed guidelines about how to fill out and submit Form 8832. Entities need to follow the official instructions carefully, providing accurate and truthful information to avoid processing delays or penalties. Consulting IRS resources or a tax professional can help in understanding the expectations and ensuring compliance, particularly in complex tax situations where guidance becomes indispensable.

Examples of Using the 2010 Form 8832

Consider a scenario where a domestic LLC wants to be classified as a corporation for IRS purposes. By filling out Form 8832, the business can notify the IRS of its preferred tax status. Similarly, a foreign entity operating in the U.S. can use the form to gain a more favorable tax classification. These examples illustrate the flexibility that Form 8832 provides, allowing businesses to tailor their tax obligations in a manner that aligns with their financial strategies.

Key Elements of the 2010 Form 8832

- Basic Information: Name, address, and EIN of the entity.

- Election Date: The effective date of the tax classification election.

- Current Classification: Designation of the entity's status before filing.

- New Classification Choice: The desired classification after the election.

- Consent Signature: Required signatures from all owners or members agreeing to the election.

Understanding these elements and their significance ensures that entities accurately communicate their tax structure preferences to the IRS, thus enhancing tax planning and compliance strategies.

Software Compatibility and Taxpayer Scenarios

Although electronic submission wasn't available in 2010, modern entities can use tax software like TurboTax or QuickBooks to organize and understand their tax statuses, even though the initial submission must be by mail. Various taxpayer scenarios apply, such as small business owners or foreign investors seeking clarity on how to impact their tax burden through correct classification. Each scenario demonstrates the need for precise adherence to IRS instructions to achieve the intended outcomes.