Definition & Meaning

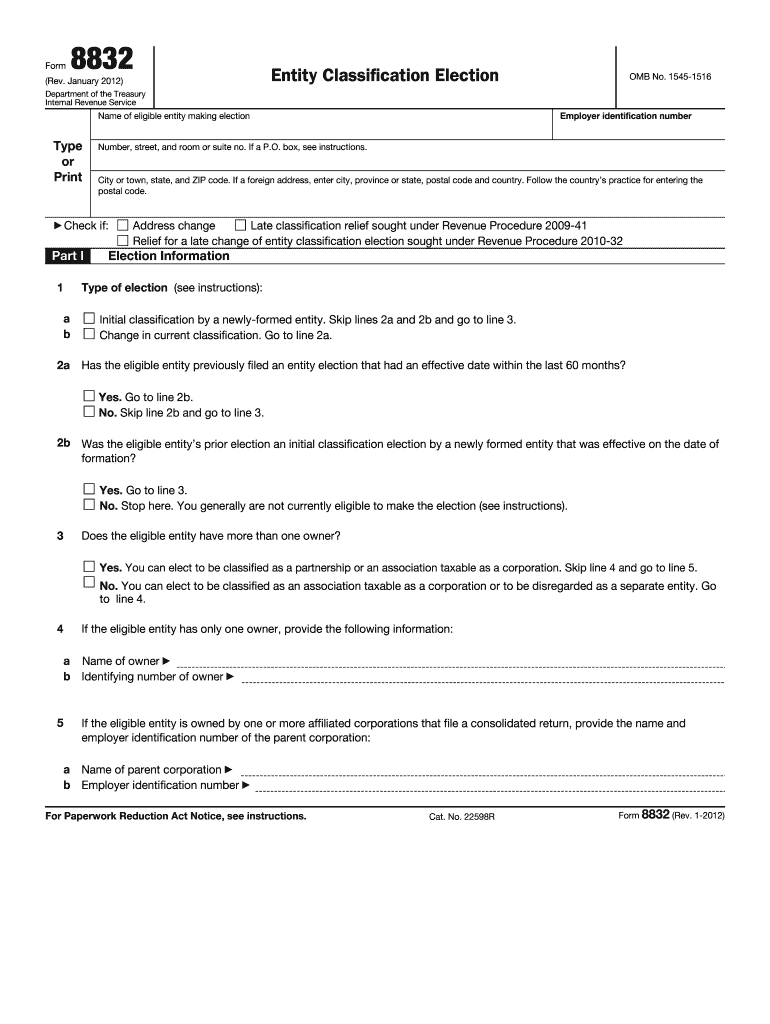

Form 8832, also known as the Entity Classification Election form, allows eligible entities to choose how they will be classified for federal tax purposes. In the context of the 2012 form 8832, this document is crucial for entities such as limited liability companies (LLCs) to determine whether they will be taxed as a corporation, partnership, or sole proprietorship (disregarded entity). Understanding the implications of each classification is essential, as it directly impacts an entity’s tax obligations and compliance with U.S. tax laws.

Key Considerations

- Corporation Election: Entities electing to be taxed as a corporation may face double taxation, once at the corporate level and again on dividends.

- Partnership Election: This classification suits entities with multiple owners, where income is passed through to individual tax returns.

- Disregarded Entity Election: Typically for single-member LLCs, where the entity is not considered separate from its owner for tax purposes.

How to Use the 2012 Form 8832

The 2012 form 8832 is used by eligible businesses to elect their preferred tax classification. This requires careful consideration and an understanding of the business's financial structure. By default, domestic entities like LLCs are treated as partnerships unless Form 8832 is filed to change this classification.

Key Steps

- Determine Eligibility: Ensure the entity is eligible to file Form 8832. Most domestic entities can file, but certain restrictions may apply.

- Select Classification: Choose between corporation, partnership, or disregarded entity based on your business needs and tax strategy.

- Complete the Form: Follow the IRS instructions carefully, filling out the information accurately to avoid processing delays.

Steps to Complete the 2012 Form 8832

Filling out Form 8832 involves several steps that require precision and a clear understanding of the entity’s current and desired classification.

Detailed Process

-

Section I: Basic Information

- Provide entity's name, address, and employer identification number (EIN).

- Indicate current and desired entity classification.

-

Section II: Election Information

- Specify the type of election and the requested date of change.

- Attach any required statements or explanations.

-

Section III: Signatures

- The form must be signed by an authorized person, typically an officer or member of the entity.

-

Submitting the Form

- Ensure the form is filed with the correct IRS service center based on your location.

Important Terms Related to 2012 Form 8832

Understanding the terminology related to Form 8832 is essential for accurate completion and compliance.

Key Terms

- Entity Classification: The tax treatment elected by a business whether as a corporation, partnership, or disregarded entity.

- Disregarded Entity: A business entity that is ignored for federal income tax purposes but may still require state filings.

- Election Date: The date when the new classification takes effect, which can be up to 75 days before or 12 months after filing.

Filing Deadlines / Important Dates

Timely filing of Form 8832 is crucial to implement the elected classification for the desired period.

Important Considerations

- Default Classifications: If no election is made, entities default to partnership or disregarded entity status.

- Retroactive Elections: The form allows for retrospective elections of up to 75 days before filing.

Required Documents

Completing Form 8832 successfully requires providing detailed documentation and statements as evidence of eligibility and classification choice.

Essential Documentation

- Prior Tax Returns: If changing classifications, past returns may be relevant to ensure compliance.

- Operating Agreement: For LLCs, the operating agreement may outline member agreements that impact classification.

IRS Guidelines for 2012 Form 8832

Adhering to IRS guidelines ensures the successful processing and approval of Form 8832.

Compliance Requirements

- Accuracy: Complete all relevant sections with precise information.

- Completeness: Include any necessary attachments and explanations for your classification choice.

Penalties for Non-Compliance

Failing to file Form 8832 correctly or on time can result in significant penalties and unintended tax implications.

Potential Consequences

- Default Classifications: Entities may default to a less favorable tax status.

- Fines and Interest: Potential fines for incorrect filing or late submissions.

- Delayed Processing: Errors or omissions can delay IRS processing and affect tax obligations.

Business Entity Types Beneficial from 2012 Form 8832

Determining the optimal tax classification can significantly impact different types of business entities.

Benefitting Entities

- LLCs: Can choose from multiple classifications to align with their business strategies.

- Multi-Member Partnerships: May elect corporate status to limit liability or strategic tax planning.

- Sole Proprietorships: Often benefit from disregarded entity status for simplicity.