Definition and Meaning of MN Surplus Lines

The term "MN Surplus Lines" refers to specific types of insurance policies that cover risks not adequately served by insurers licensed within Minnesota. These insurance contracts are procured from nonadmitted insurers, meaning the companies are not licensed by the state's insurance department but are permitted to cover risks under the laws governing surplus lines. This concept enables individuals and businesses to obtain coverage for unique or high-risk circumstances that traditional insurers might refuse. Surplus lines play a crucial role in the insurance market by offering solutions where conventional insurance avenues do not suffice.

How to Use MN Surplus Lines Insurance

Using MN surplus lines insurance involves a few critical steps. First, the individual or business requiring coverage must identify the risks not covered by admitted insurers in Minnesota. It is essential to work with a licensed surplus lines broker who can access nonadmitted insurers. This broker will assist in finding the best policy match, ensuring compliance with state regulations. Once a suitable policy is identified, the broker facilitates the purchase and ensures that the correct taxes, required under Minnesota law, are calculated and paid to the state.

Steps to Obtain MN Surplus Lines Insurance

- Identify Coverage Needs: Determine the specific risks not covered by licensed insurers in Minnesota.

- Engage a Licensed Broker: Consult with a broker licensed to handle surplus lines, as only specialists can transact these policies.

- Research and Select Policies: The broker provides options from nonadmitted insurers.

- Purchasing the Policy: Finalize the policy purchase through the broker, who will manage all logistical and legal requirements.

- Filing and Payment of Taxes: Brokers must report the policy purchase to the state and facilitate the payment of any applicable taxes or fees.

Key Elements of MN Surplus Lines Policies

- Nonadmitted Insurers: Policies originate from insurers not licensed in Minnesota but approved for surplus lines.

- Broker Involvement: An essential intermediary licensed specifically for surplus lines.

- Regulatory Compliance: Adherence to reporting and tax payment regulations as outlined by the state.

- Policy Specificity: Tailored to cover unique or high-risk circumstances that are not typically insurable through admitted insurers.

Important Terms Related to MN Surplus Lines

- Nonadmitted Insurers: Insurers not licensed in a particular state but allowed to provide surplus lines insurance.

- Surplus Lines Broker: A specialist licensed to negotiate surplus lines insurance.

- Admitted vs. Nonadmitted: Admitted insurers are licensed by the state, while nonadmitted insurers are not.

- Premium Tax: A tax on the premiums of surplus lines insurance, usually collected by brokers and paid to the state.

Legal Use of MN Surplus Lines Insurance

The Minnesota state government allows surplus lines insurance as a legal means to procure coverage where admitted insurers fall short. It is governed by specific regulations requiring brokers to handle the policy purchasing and compliance aspects. This includes adhering strictly to reporting standards and ensuring all taxes owed are paid punctually, avoiding penalties.

Filing Deadlines and Important Dates

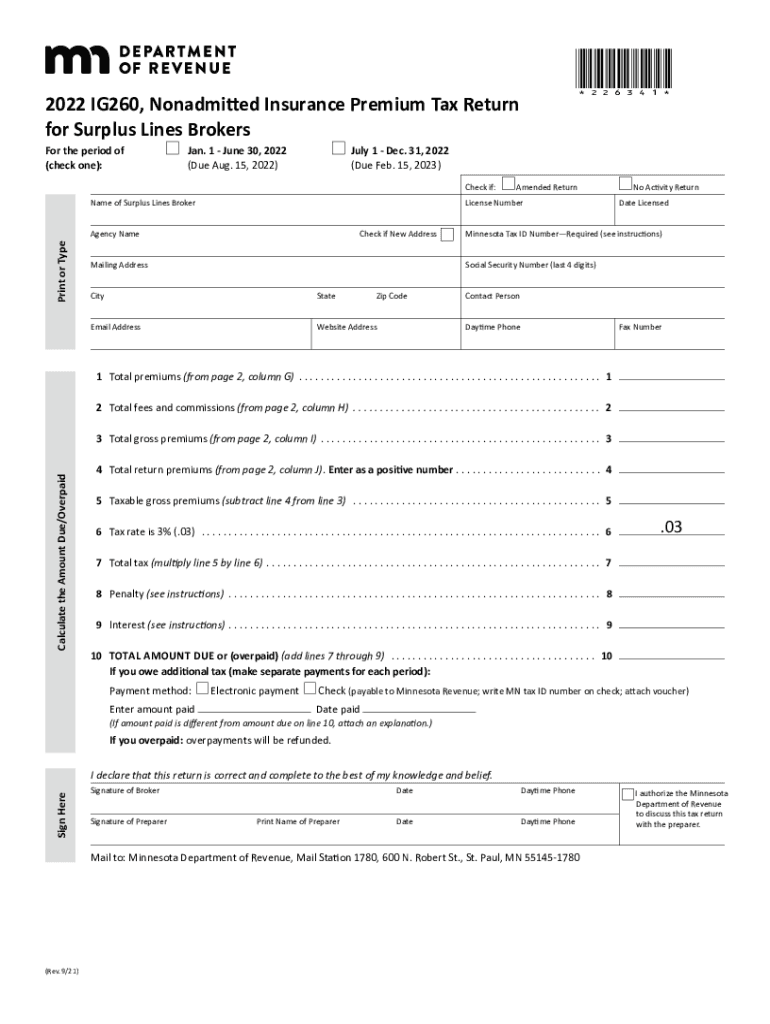

For surplus lines insurance brokers in Minnesota, the key deadlines relate to the semiannual tax return submissions. These include filing the IG260 form twice yearly, with precise due dates outlined by the Minnesota Department of Revenue. Even if no tax is due, brokers must submit this form timely to demonstrate compliance with state insurance laws.

Required Documents for MN Surplus Lines

To ensure compliance and proper documentation of MN surplus lines insurance, several documents are typically required:

- IG260 Form: To report and pay the premium tax.

- Broker License: Certification allowing the broker to transact surplus lines.

- Proof of Coverage: Documentation from the nonadmitted insurer confirming policy details.

State-Specific Rules for MN Surplus Lines

Minnesota imposes specific rules governing the use and purchase of surplus lines insurance. This includes the necessity for brokers to have a surplus lines license and for all transactions to be fully documented and reported. Additionally, all surplus lines policies must be clearly identified as such, ensuring transparency and compliance with state regulations.