Definition and Meaning

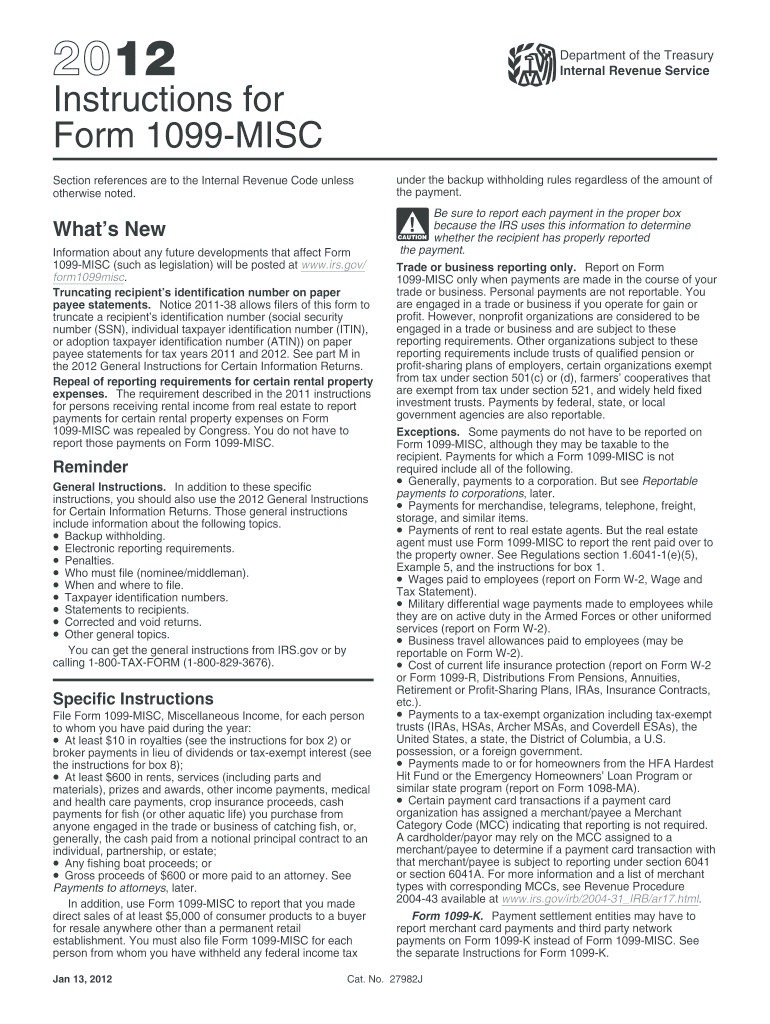

The "2012 instructions form" typically refers to guidelines issued by the Internal Revenue Service (IRS) for completing a specific tax form for the year 2012. These instructions outline the necessary steps, definitions, and details to accurately complete tax documents and are essential for ensuring compliance with federal requirements. Understanding these forms requires familiarity with the tax year's specific adjustments and requirements, reflecting any legislative changes or policy updates that impacted taxation during 2012.

How to Use the 2012 Instructions Form

Using the 2012 instructions form involves a step-by-step approach to decoding the content and applying it to the relevant tax form. First, identify the particular form or application associated with these instructions, such as the 1099-MISC for miscellaneous income. Next, read through each section to understand the specific requirements, focusing especially on sections dealing with income inclusivity, exemptions, and deductions. Make sure to cross-reference the guidelines with specific line items on the tax form to ensure all tables, charts, or examples apply directly to your circumstances.

Steps to Complete the 2012 Instructions Form

- Gather Necessary Documents: Ensure you have all the required financial documents, receipts, and previous tax returns on hand.

- Review the Instructions: Carefully read each section of the instructions form, paying attention to notes that highlight changes specific to the 2012 tax year.

- Calculate Income and Deductions: Use provided worksheets to compute any required figures, such as taxable income or qualifying deductions.

- Complete the Tax Form: Fill out the corresponding tax form, using official calculations and guidance from the instructions.

- Verify All Information: Double-check all entered data against your records and the instruction guidelines to prevent errors or omissions.

- Submit the Form: Choose your submission method, such as electronic filing or mail, ensuring compliance with the required submission protocols.

Filing Deadlines and Important Dates

Adhering to filing deadlines is crucial for avoiding penalties. For the 2012 tax year, the standard IRS deadline for most individual tax returns was April 15, 2013. Extensions might have been available, but an extension request needed to be filed by this date. It's also important to consider dates for payment obligations if you owed taxes, as failing to pay on time could result in interest and late payment penalties. Specific deadlines could vary for different business types or those with international tax obligations.

Important Terms Related to the 2012 Instructions Form

- Gross Income: Total revenue before any deductions or exemptions.

- Adjusted Gross Income (AGI): Income after adjustments and deductions, critical for determining tax liability.

- Exemptions: Specific reductions to taxable income based on taxpayer status or dependents.

- Filing Status: Classification based on marital or family situation impacting tax bracket determination.

- Tax Credit: Direct reductions to tax owed, different from deductions which reduce taxable income.

Examples of Using the 2012 Instructions Form

For instance, a self-employed contractor receiving miscellaneous income through 1099-MISC forms in 2012 would use the instructions to identify reportable amounts and allowable deductions, such as travel expenses. A retiree might consult the instructions to determine how to handle distributions from retirement accounts. Another example involves a corporation declaring dividends, turning to the instructions to navigate the appropriate reporting channels and ensure shareholder compliance.

Legal Use of the 2012 Instructions Form

Proper use of the 2012 instructions form ensures compliance with federal tax regulations, avoiding legal pitfalls like underreporting income or misstating expenses. The guidelines provided help navigate complex situations such as dealing with foreign income, adapting to legislative changes in tax code, or employing credits and deductions appropriately. Failing to adhere to these instructions could result in audits, fines, or legal consequences for fraud or negligence.

Penalties for Non-Compliance

Non-compliance with the IRS requirements outlined in the 2012 instructions form can lead to significant penalties. Potential consequences include fines for late filing or payments, interest on unpaid taxes, and additional penalties for underpayment or underreporting of income. In severe cases, legal actions may ensue, emphasizing the necessity of precise and accurate adherence to the form's guidance.

Taxpayer Scenarios

Various scenarios necessitate nuanced use of the 2012 instructions form. Individuals with multiple income sources, such as wage earners and freelancers, must consolidate their income data accurately. Businesses utilizing form instructions to report employee compensation via W-2 or contract labor via Form 1099-MISC must ensure categorizations align with IRS mandates. Retirees or individuals with investment incomes also rely on the instructions to manage taxes on social security benefits, dividends, and capital gains correctly.