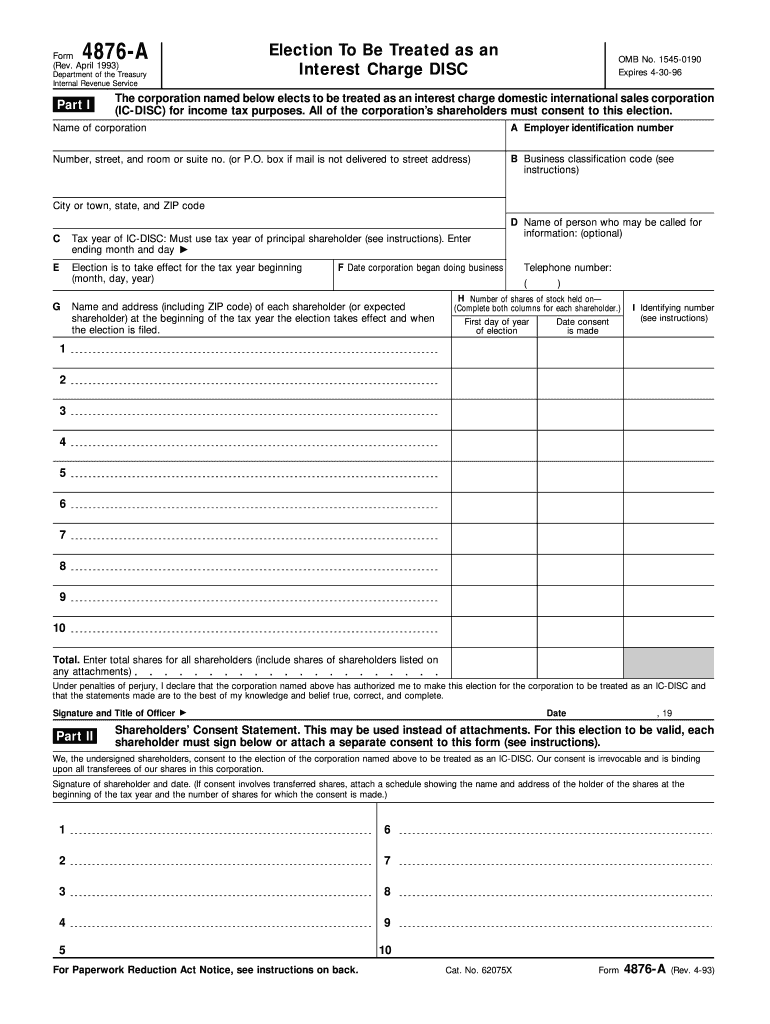

Definition & Purpose of Form 4876-A

Form 4876-A, often referenced as the Election Form for Interest Charge Domestic International Sales Corporation (IC-DISC), is a U.S. tax form that provides corporations with the opportunity to elect IC-DISC status. This classification can offer significant tax advantages by allowing certain foreign sales income to be deferred or taxed at a lower rate. The form includes sections dedicated to corporate information, shareholder consent, and eligibility criteria, all pivotal for securing this special tax treatment.

Historical Context

This form, first introduced in 1993, was part of legislative measures aimed at boosting U.S. exports by granting favorable tax treatments to domestic corporations engaging in international sales. By electing IC-DISC status, corporations could defer part of their income attribution to shareholders, thus reducing immediate tax liabilities.

Steps to Complete the 4876-A Form

Filling out Form 4876-A involves several key steps that require careful attention to detail:

-

Gather Corporate Information

- Begin by collecting the corporation's name, address, and taxpayer identification number. Ensure these details are current and accurately reflect the latest corporate registration documents.

-

Shareholder Information

- Provide a complete list of all shareholders, including their names, addresses, and percentage of ownership. Consent from each shareholder is mandatory and should be documented accordingly.

-

Consent Statement

- Each shareholder must sign a consent statement agreeing to the IC-DISC election. This statement verifies that all parties are aware of the tax implications and benefits associated with the IC-DISC status.

-

Eligibility Criteria Verification

- Confirm that the corporation meets all eligibility requirements, which include limitations on foreign sales revenue proportions and compliance with specific business activity regulations.

-

Filing

- Submit the completed form to the IRS as per the specified deadlines. Ensuring timely submission is crucial to avoid penalties and to maintain the desired tax status.

How to Obtain Form 4876-A

Form 4876-A is available through multiple channels:

-

Online Access

- The IRS website provides digital copies of the form, allowing corporations to download and print physical copies as needed for filing.

-

Tax Preparation Software

- Platforms such as TurboTax and QuickBooks support direct access to Form 4876-A, offering integration with digital tax filing solutions for streamlined processing.

-

Tax Advisors

- Consulting a tax advisor or attorney can provide access to the form and offer guidance on its completion, especially beneficial for those unfamiliar with international sales taxation laws.

Key Elements of Form 4876-A

Understanding the critical components of Form 4876-A is essential for accurate completion:

-

Corporate Information

- Detailed corporate identifiers that must align with records on file with federal and state tax authorities.

-

Shareholder Consent

- A documented agreement from all shareholders is required to validate the election process.

-

Eligibility Section

- Criteria such as the export sale percentage and revenue distribution need to be established to qualify for IC-DISC status.

IRS Guidelines on Form 4876-A

The IRS provides comprehensive guidelines to assist corporations in the accurate completion and timely submission of Form 4876-A:

-

Documentation

- Ensure all sections are fully completed and signed, and accompany the form with any supporting documentation as specified by IRS instructions.

-

Submission Deadline

- Corporations must adhere to strict submission deadlines, typically at the end of the corporation's tax year. Filing delays can nullify the election for the requested period.

Eligibility Criteria for Form 4876-A

To qualify for the IC-DISC election, corporations must meet certain criteria:

-

Domestic Incorporation

- The entity must be incorporated within the United States and maintain the majority of its financial activities domestically.

-

Export Revenue

- A significant portion of the corporation's revenue, generally at least 95%, must originate from exported goods and services.

-

Shareholder Agreement

- Consensus among all shareholders is required, dictating a unified stance on electing IC-DISC status.

Penalties for Non-Compliance

Failing to comply with the requirements and deadlines associated with Form 4876-A can result in severe ramifications:

-

Loss of IC-DISC Status

- Inadequate or incorrect submissions can negate the election, leading to immediate standard corporate tax implications.

-

Financial Penalties

- Corporations may incur fines and penalties for late submissions or filing errors.

Business Types Benefiting from Form 4876-A

Corporations most likely to benefit from electing IC-DISC status include:

-

Manufacturing Firms

- Engaging in significant export activities and distributing goods internationally.

-

Distribution Companies

- Those that re-export products after domestic purchase, maximizing the markup potential through international sales.

By understanding the nuances of Form 4876-A, corporations can strategically plan their electing process to ensure legal compliance and optimize tax benefits, leveraging the economic advantages for international trade growth.