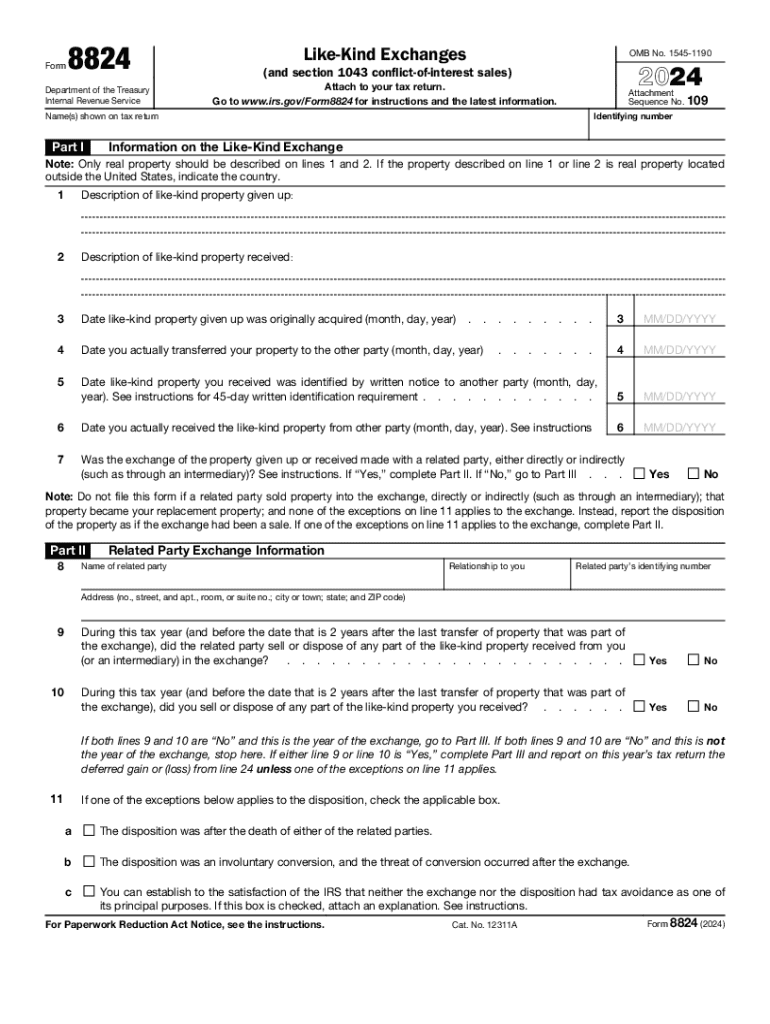

Definition and Purpose of Form 8824

Form 8824, commonly known as the Like-Kind Exchange form, is utilized by taxpayers to report exchanges of real estate that qualify for tax deferral under Internal Revenue Code Section 1031. It is particularly relevant for real estate investors looking to defer capital gains taxes when they exchange one property for another similar property. The form also covers section 1043 conflict-of-interest sales, which help certain government employees defer gains on sales of property to avoid conflicts of interest. Essential for understanding when reporting exchanges, this form ensures compliance with IRS regulations.

Steps to Complete Form 8824

-

Part I: Information on the Like-Kind Exchange

- Enter detailed descriptions of the relinquished and acquired properties.

- Provide dates of acquisition and transfer, ensuring accuracy to avoid penalties.

-

Part II: Related Party Exchange Information, If Applicable

- Disclose any related-party transactions to ensure transparency and compliance.

-

Part III: Realized Gain or Loss and Its Deferral

- Calculate the realized gain or loss from the exchange process.

- Determine the deferred gain based on the properties exchanged.

-

Part IV: Section 1043 Transactions

- Complete specific details if the transaction is intended to resolve a conflict-of-interest scenario under Section 1043.

Eligibility Criteria for Like-Kind Exchanges

To qualify for reporting on Form 8824, the exchange must adhere to these criteria:

- Properties involved must be of a similar nature—real property for real property—as per IRS guidelines.

- Both properties should be held for investment or productive use in a business.

- The transaction must meet specific IRS timelines, generally involving a 45-day identification period and a 180-day exchange completion period.

Important IRS Guidelines and Deadlines

Understanding IRS guidelines and adhering to critical deadlines is vital:

- Identification Period: Within 45 days of selling the relinquished property, identify potential replacement properties.

- Exchange Period: Complete the property exchange within 180 days of the initial sale.

Failure to comply with these timelines could result in a full taxable event, negating any potential tax benefits.

Legal Implications and Use

Legal compliance in completing and submitting Form 8824 is crucial:

- Disclosure Requirements: Ensure all relevant transaction details and related parties are accurately reported.

- Penalties: Incorrect or fraudulent reporting may invite IRS audits and significant financial penalties.

Who Typically Uses Form 8824

Primary users include:

- Real estate investors seeking to maximize tax benefits from property exchanges.

- Government employees participating in conflict-of-interest sales under Section 1043.

- Various business entities, such as corporations and partnerships, involved in property exchanges for business purposes.

Software Compatibility and Digital Considerations

For taxpayers preferring digital submissions, Form 8824 is compatible with many tax software programs, such as TurboTax and QuickBooks, which facilitate efficient filing and ensure adherence to IRS guidelines. Utilizing software can streamline the process and reduce the likelihood of errors.

Examples and Scenarios of Using Form 8824

Consider a real estate investor who exchanges a commercial property for another within the same market. By using Form 8824, the investor defers immediate capital gains taxes, allowing for reinvestment capital growth. Alternatively, a government employee selling shares in a conflict-of-interest scenario would also rely on this form to manage tax implications effectively.

Key Elements and Required Documents

When preparing to complete Form 8824, ensure availability of:

- Sale and purchase agreements for both properties.

- Property descriptions, acquisition, and transfer documents.

- Documentation supporting the fair market value assessments of exchanged properties.

Form 8824 serves as a pivotal document in the tax management strategy for like-kind exchanges and conflict-of-interest sales, offering significant benefits while requiring diligent compliance and understanding of IRS constraints.