Definition and Purpose of Form 8824

Form 8824 is an Internal Revenue Service (IRS) document used primarily to report like-kind exchanges of business or investment property. This form is essential for taxpayers who engage in exchanges that qualify under section 1031 of the Internal Revenue Code, allowing the deferral of capital gains taxes. The essence of Form 8824 is to detail the transactional elements of property exchanges, including descriptions, involved parties, and relevant dates, ensuring compliance and simplifying the legal tax deferral process.

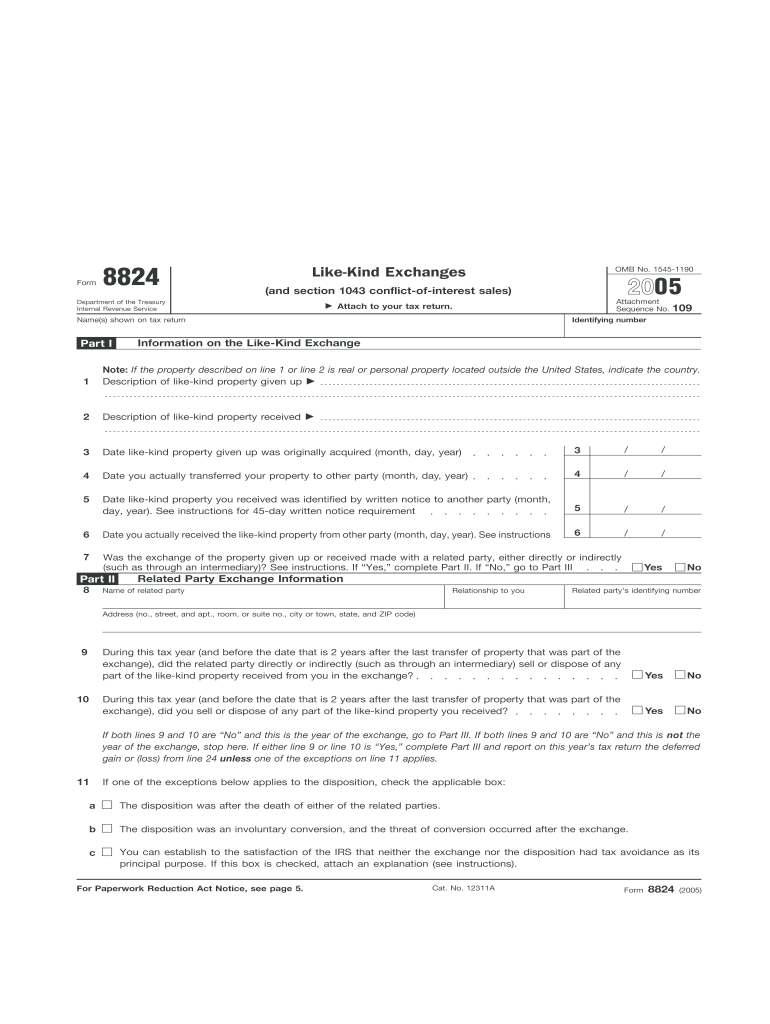

Related Party Exchanges

In the context of Form 8824, related party exchanges require special attention to ensure compliance with IRS rules. Transactions involving related parties must adhere to the strict guidelines to prevent tax avoidance tactics. Exchanges between related parties are scrutinized for their intent and timing, as these transactions must maintain the deferral status for a minimum of two years post-exchange. Understanding and documenting these details accurately on Form 8824 is crucial for compliance and claiming benefits properly.

Steps to Complete Form 8824

Completing Form 8824 involves several critical steps:

-

Transaction Details: Provide thorough descriptions of both the relinquished and received properties. This includes the dates of exchange and fair market values.

-

Gain or Loss Realization: Calculate and document the realized gain or loss on the exchange. The form includes sections to guide the taxpayer through these calculations, ensuring accuracy.

-

Deferral Calculation: Apply the deferral rules under section 1031 for legitimate like-kind exchanges. Document any boot received, which affects the deferral status by recognizing partial gains.

-

Certification: Sign and date the form, certifying the truthfulness and accuracy of the provided information.

Essential Tips for Completion

- Use specific, clear descriptions for properties involved.

- Double-check calculations for realized gains and losses.

- Ensure exchange qualifies as like-kind under IRS regulations.

Who Uses Form 8824?

Form 8824 is utilized by taxpayers who engage in the exchange of properties held for business or investment purposes. These individuals or entities include:

- Real estate investors seeking to defer capital gains taxes.

- Business owners handling the replacement of significant capital assets.

- Farmers exchanging farm equipment or land.

Special Cases

Government employees involved in conflict-of-interest sales may also utilize Form 8824 to defer capital gains. Understanding the specific exceptions and conditions applicable to these unique exchanges is vital for compliance.

Filing Deadlines and Important Dates

The timely submission of Form 8824 is crucial for tax compliance. Typically, the form should be filed simultaneously with the taxpayer's federal income tax return for the year in which the exchange commenced. Keeping track of important dates, such as the 45-day identification window and the 180-day completion period for replacement property, ensures adherence to legal requirements.

Consequences of Late Submission

Failure to submit Form 8824 in a timely manner could lead to the IRS disallowing the like-kind exchange deferral, resulting in immediate tax liability on the transaction. Late submission could potentially trigger penalties and interest on unpaid taxes.

Key Elements of Form 8824

The form comprises several integral sections that taxpayers must complete accurately:

- Identification Section: Includes taxpayer information and a brief summary of the exchange.

- Calculation Section: Guides through the computation of realized and recognized gain, detailing conditions for legitimate deferral.

- Related Party Information: Requires detailed disclosures if the exchange involves related parties to avoid tax avoidance scrutiny.

Important Fields

Specific fields within the form demand particular attention, such as property descriptions and confirmations of compliance with Section 1031 requirements. Accurate completion of these fields ensures proper processing by the IRS.

IRS Guidelines for Form 8824

The IRS provides comprehensive guidelines to aid taxpayers in correctly completing Form 8824. These guidelines explain the statutory requirements and provide examples of applicable like-kind exchanges. IRS publications and official instructions accompany the form, outlining nuanced rules for complex scenarios involving boot, third-party intermediaries, and deferred exchanges.

Official Instructions

Taxpayers can refer to IRS Publication 544 and the official instructions for Form 8824 for further clarification on completing the form. Familiarity with these documents can aid in avoiding common errors and ensuring compliance.

State-Specific Rules for Form 8824

While Form 8824 is used for federal tax purposes, state-level adaptations may exist, particularly in states with conforming tax regulations. Some states may require additional documentation or specific forms to report like-kind exchanges for state tax purposes.

Notable State Considerations

Taxpayers should be aware of states that have decoupled from federal regulations regarding like-kind exchanges. In such cases, adherence to state-specific rules is necessary to maintain compliance and avoid discrepancies in tax reporting.

Penalties for Non-Compliance

Failure to comply with the requirements of Form 8824 can result in penalties, including disqualification of the exchange, immediate recognition of taxable gains, and associated interest on unpaid taxes. The IRS may impose penalties for inaccuracies or omissions if deemed negligent or fraudulent.

Preventive Measures

- Ensure thorough review before submission.

- Consult with tax professionals knowledgeable in like-kind exchanges.

- Maintain detailed documentation to support the eligibility of the exchange.