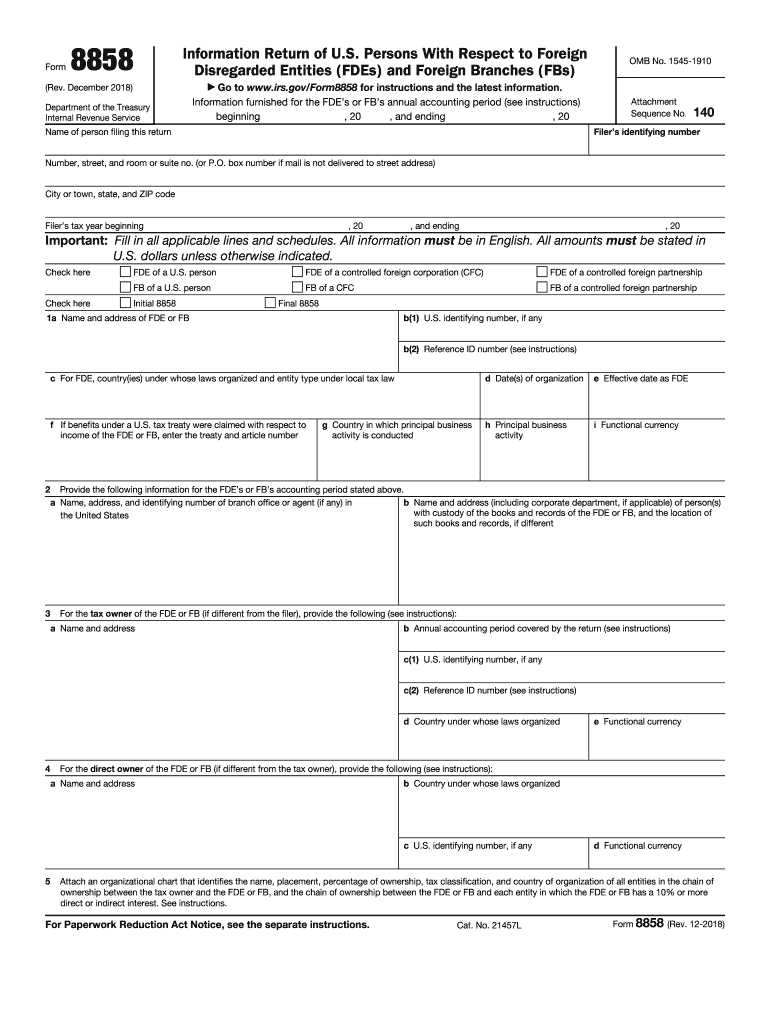

Definition and Purpose of IRS Form 8858

IRS Form 8858, officially titled the "Information Return of U.S. Persons With Respect to Foreign Disregarded Entities," serves as an essential document for U.S. individuals and businesses engaged with foreign disregarded entities (FDEs) and foreign branches (FBs). This form helps the IRS monitor international financial activities and ensure compliance with U.S. tax regulations by capturing critical information about foreign entitlements and business interests. FDEs are foreign entities that are disregarded for U.S. tax purposes, meaning their activities are directly reported by the owner on their U.S. tax return. Similarly, FBs refer to operable divisions of U.S. corporations located overseas. The consistent use of Form 8858 allows the IRS to collect integrative details, such as financial data, ownership structures, and regulatory compliance, aiding in the evaluation of cross-border income and expense flows.

Eligible Users of IRS Form 8858

Typically, IRS Form 8858 is used by U.S. persons who own foreign disregarded entities or operate foreign branches. This includes individuals, partnerships, corporations, and limited liability companies (LLCs) that engage directly or indirectly with foreign business operations. The key requirement is that the reporting person must have a sufficient level of control, commonly meaning over 50% ownership, or must be one of the owners responsible for filing consolidated tax returns. This form is crucial for entities involved in managing international business transactional structures, ensuring their income is accurately reflected and reported in accordance with U.S. tax guidelines.

Key Elements of IRS Form 8858

Form 8858 comprises several parts that comprehensively document international business engagements:

- Section I: General information about the filer, including their identification number and the tax year.

- Section II: Information about the foreign disregarded entity or branch, detailing its operations, address, and primary business activity.

- Section III: Financial data that captures income statements and balance sheet figures typical of such entities.

- Section IV: Documentation of transactions between the U.S. person and the FDE or FB.

- Section V: Additional statements and disclosures that align with related party transactions and other pertinent international activities.

Each section mandates precise entries to ensure thorough and lawful tax reporting, and inaccuracies or omissions may lead to further inquiry or penalties.

Filing Deadlines and Important Dates

The submission deadline for IRS Form 8858 often aligns with the filing of the taxpayer's main income tax return, including extensions. For most calendar-year filers, this date is usually April 15th of the following year, unless that date falls on a weekend or holiday in which the deadline might be extended. Taxpayers eligible for an automatic extension must ensure the accompanying Form 8858 is included to avoid issues associated with untimely filings. Notably, maintaining awareness of potential legislative changes affecting these dates is essential as they can vary from year to year.

Step-by-Step Guide to Completing IRS Form 8858

-

Gather Required Documentation: Before you start, compile necessary documents such as financial statements, details of ownership interests, and any prior foreign income tax returns relevant to the FDE or FB.

-

Complete General Information Sections: Enter your identifying information, including your name, Taxpayer Identification Number (TIN), and principal country of residence.

-

Detail Foreign Entity Information: Fill in pertinent details about the FDE/FB, including names, addresses, and primary business operations.

-

Financial Information Entry: Provide accurate figures for the foreign entity's balance sheets and income statements, reflecting all financial activities.

-

Transaction Reporting: List all transactions that occurred between the U.S. person and the foreign entities, ensuring compliance with related party disclosure requirements.

-

Review and Verify Entries: Carefully double-check each section for accuracy to prevent filing mishaps or potential IRS audits.

-

File with Main Tax Return: Attach Form 8858 to your federal tax return and submit by the due date.

Penalties for Non-Compliance

Failure to file a timely and accurate Form 8858 can result in significant penalties. The IRS imposes fines starting at $10,000 per missed form, with the potential for additional penalties if the delay extends after the initial notification. If an entity continues non-compliance, a daily penalty of $10 can be added up to a maximum of $50,000. Beyond financial consequences, non-compliance may flag an account for audit, increasing scrutiny on other tax matters.

Impact of IRS Guidelines and Amendments

IRS policies and guidelines regularly undergo revision to align with evolving financial and international standards. Recent amendments typically address clarity and compliance topics, ensuring they align with international tax agreements and treaties. Monitoring these updates is crucial as they directly impact reporting methods and the potential tax implications for U.S. persons involved in global economic activities.

Technological Solutions and Software Compatibility

Platforms like DocHub facilitate the preparation and electronic submission of IRS Form 8858 for users embracing tech solutions for tax compliance. Additionally, tax preparation software such as TurboTax and QuickBooks may offer integrated features to assist with Form 8858 completion. Ensuring compatibility and functional integration between your document management system and these tax platforms is pivotal in optimizing compliance efforts and minimizing errors.

Examples and Diverse Use Cases for IRS Form 8858

Consider a U.S. LLC owning a manufacturing subsidiary in Germany. Utilizing Form 8858, the LLC accurately reports its financial interactions, profits derived, and expenses incurred related to this foreign branch. In another scenario, a U.S. individual owning a consulting service in Singapore uses the form to report its financials to ensure U.S. taxes are applied correctly despite international operations. Such real-world examples showcase the necessity of Form 8858 in varied global business contexts, helping maintain transparency and compliance with U.S. tax laws while addressing diverse operational footprints of U.S. entities abroad.