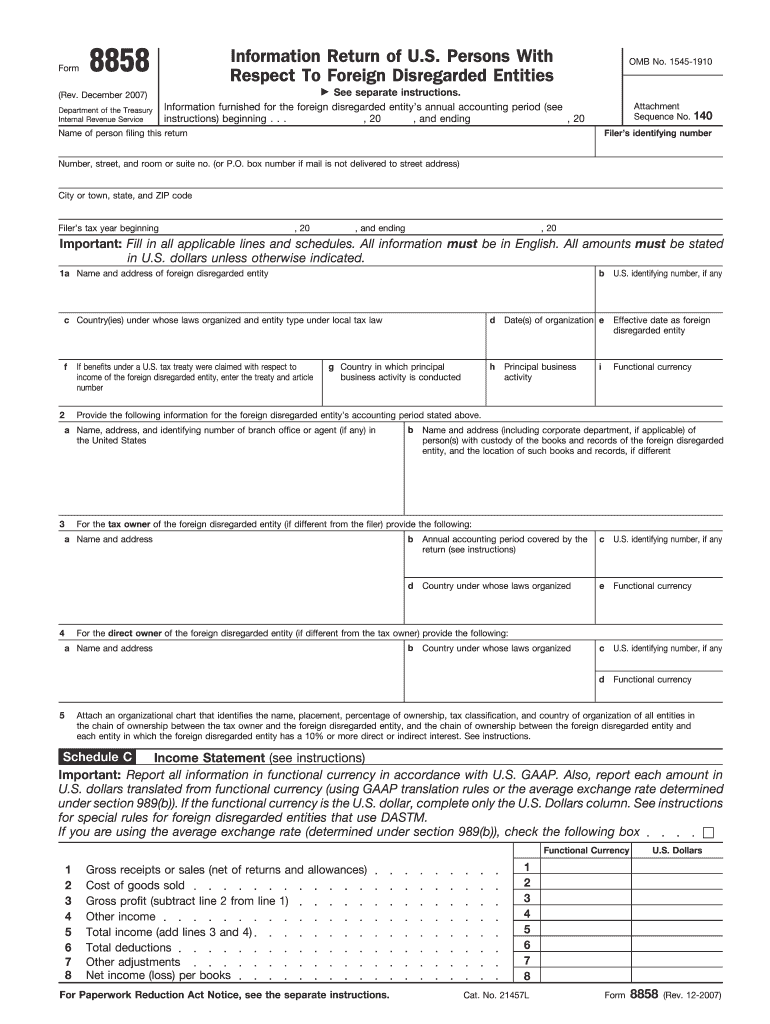

Definition and Purpose of Form 8858

Form 8858 is an information return used by U.S. persons to report details about foreign disregarded entities and foreign branches. Required by the Internal Revenue Service (IRS), its main objective is to ensure compliance with U.S. tax laws concerning foreign entities. This form includes multiple sections detailing ownership structures, financial activities, and income statements of such entities in accordance with U.S. Generally Accepted Accounting Principles (GAAP).

Key Components and Their Importance

- Foreign Disregarded Entities Details: The form captures critical data about foreign disregarded entities, including ownership and operational specifics.

- Financial Activity Reporting: Ensures transparent accounting of foreign income and financial transactions.

- U.S. GAAP Compliance: Aligns financial statement presentation with U.S. standards to maintain consistency and accuracy.

Steps to Complete Form 8858 for 2007

When filling out Form 8858 for the year 2007, it is essential to follow a structured process to ensure accuracy and completeness.

- Gather Necessary Documentation: Collect financial statements, transactional details, and ownership records pertaining to the foreign entity.

- Complete Identification Section: Fill out information about both the U.S. person filing the form and the foreign entity being reported.

- Ownership Information: Provide detailed ownership percentages and entity structures.

- Financial Information: Accurately report income, expenses, and other financial metrics according to U.S. GAAP.

- Review and Verification: Thoroughly check entries against source documents for accuracy before submission.

Practical Example

Suppose you are a U.S. citizen with a business interest in a Canadian startup treated as a disregarded entity for U.S. tax purposes. Form 8858 would require you to report this interest, along with any income generated, to comply with IRS requirements.

How to Obtain Form 8858

Acquiring Form 8858 involves multiple channels to cater to different preferences and technological access.

- Download from IRS Website: Forms and instructional guides are available as PDFs for download.

- Software Compatibility: Tax preparation platforms like TurboTax and QuickBooks can help automate data entry and e-filing, simplifying the submission process.

- Direct Request via Mail: Physical copies can be ordered from the IRS if online access is a limitation.

Considerations for Different Filing Methods

Choosing between digital or paper submissions depends on one's comfort with technology and access to the Internet. Digital submissions generally offer quicker processing times and an easier way to ensure accuracy.

Penalties for Non-Compliance

Failure to file Form 8858 can lead to significant penalties enforced by the IRS, ranging from monetary fines to implications on one's tax status.

- Monetary Fines: Not submitting the form or delay in submission often results in financial penalties.

- Audit Risks: Non-compliance can trigger audits, leading to more detailed scrutiny of one's financial activities.

- Increased Legal Exposure: Ensures legal ramifications and future compliance hurdles.

Preventative Measures

- Timely Compliance: Regularly review filing deadlines and IRS notices to maintain compliance.

- Use of Tax Professionals: Engage a tax consultant to navigate complex filings.

Filing Deadlines and IRS Guidelines

Compliance with filing deadlines is crucial to avoid penalties and ensure smooth processing.

- Annual Filing Requirement: Form is typically due with the U.S. person's applicable income tax return, including extensions.

- IRS Published Deadlines: Referencing IRS timelines is essential for aligning submissions appropriately.

Important Dates for 2007

For the 2007 tax year, ensure filing aligns with the tax return due date, incorporating extensions as needed.

Eligibility Criteria for Filing

Determining who must file Form 8858 involves assessing several eligibility factors.

- U.S. Persons with Foreign Interests: Includes individuals, partnerships, and corporations with qualifying foreign disregarded entities.

- Ownership Thresholds: A significant criterion is having a substantial control or ownership stake in the foreign entity.

Special Cases and Exceptions

Certain entities, such as tax-exempt organizations, may have different filing obligations and thresholds.

Important Terms Related to Form 8858

Understanding terminology related to Form 8858 is crucial for effective completion and compliance.

- Foreign Disregarded Entity (FDE): An entity ignored for U.S. tax purposes while still considered for foreign tax obligations.

- Financial Activities Schedule: Section of the form dedicated to detailing various income and expense items.

- Branch Reporting: Specific reporting requirements for foreign branch operations different from disregarded entities.

Glossary of Common Terms

- GAAP Compliance: Aligning financial reporting with U.S. accounting principles.

- U.S. Person: Includes citizens or residents required to report foreign income.

Practical Examples of Using Form 8858

Real-world scenarios help illustrate the application of Form 8858.

- Example 1: A U.S. corporation with a foreign R&D subsidiary reports consolidated financials to ensure tax compliance.

- Example 2: An individual investor with a controlling interest in an overseas startup uses the form to report international income.

Case Studies and Common Pitfalls

- Pitfall 1: Inaccurate financial reporting can lead to compliance challenges.

- Case Study: A company corrected its tax posture by retrospectively aligning its submissions with GAAP.

Key Elements of the Form 8858

The form's structural components are laid out to capture a comprehensive picture of the foreign entity's operational scope.

- Entity Information: Basic details including name, country, and U.S. owner details.

- Financial Statements: Essential data including balance sheets and income statements.

- Specific Instructions: Guidelines for particular complex scenarios often encountered by multinational entities.

In-Depth Analysis of Sections

Each section's role is outlined in detail, providing insights into how they contribute to the overall goal of transparent international financial reporting.

The content provided offers in-depth guidance and context to help understand, complete, and submit Form 8858 for 2007. By following detailed instructions, understanding penalties, and meeting eligibility requirements, individuals and businesses can ensure compliance with IRS regulations regarding foreign disregarded entities.