Definition & Meaning

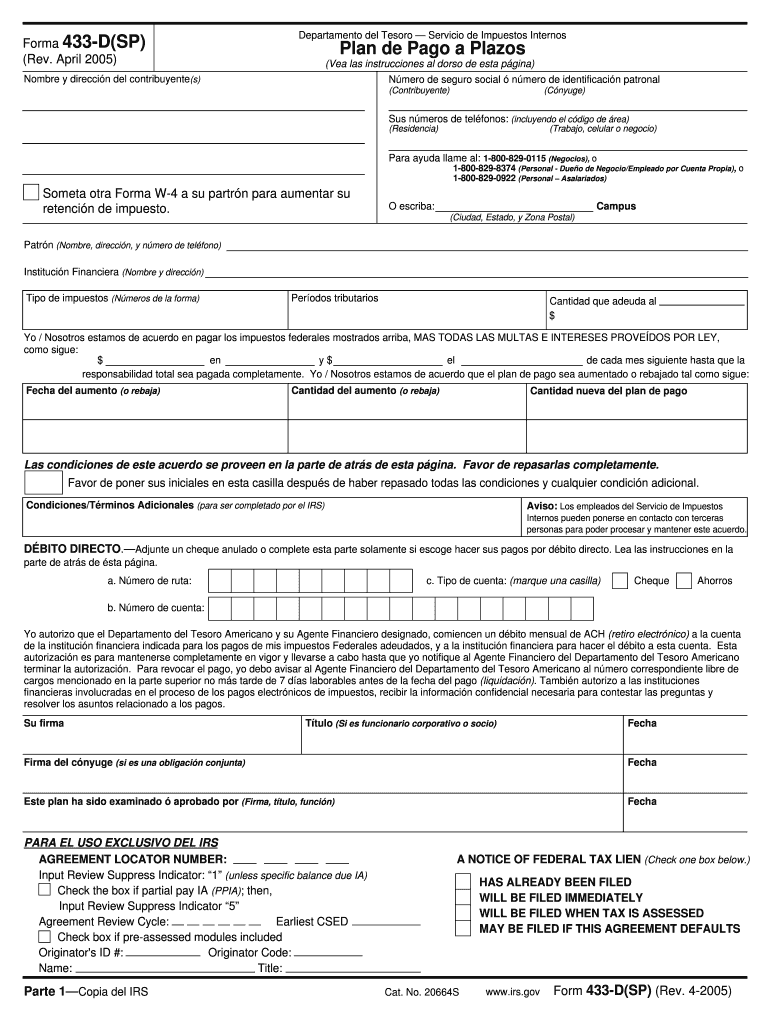

Form 433-D, known as an Installment Agreement, is a critical IRS document that facilitates taxpayers in setting up a legally binding payment plan for settling their federal tax liabilities over time. This form outlines the taxpayer's financial details, the total amount owed, and the terms under which they agree to fulfill their tax obligation via periodic installment payments. It includes specifics such as the payment amount, frequency, and method, often through direct debit from a bank account. Known more commonly as an Installment Agreement, this form allows taxpayers to meet their obligations without bearing the financial strain of paying in full immediately.

How to Use the IRS Form 433-D

To effectively use Form 433-D, taxpayers should first gather all necessary personal and financial information, including their Social Security Number, tax filing status, and the total tax debt. This form must be completed accurately to avoid delays in processing or rejection by the IRS. Taxpayers will need to outline their proposed payment schedule, ensuring it adheres to IRS guidelines and that they can reasonably meet these obligations. Once completed, the form should be returned to the IRS via the specified submission methods, which may include mailing or faxing, depending on the circumstances outlined by the IRS.

Steps to Complete Form 433-D

-

Gather Required Information:

- Social Security Number.

- Total tax liability.

- Proposed installment amount and payment frequency.

-

Fill Out Personal Information:

- Complete sections with your full name, contact information, and employer details, if applicable.

-

Outline Payment Schedule:

- Specify the monthly payment amount.

- Indicate preferred payment method, such as direct debit, and provide necessary bank details if chosen.

-

Review Terms of the Agreement:

- Read all included terms and conditions thoroughly to understand obligations and rights.

-

Submit the Form:

- Send the completed form to the IRS, using the designated mailing address or fax number, as instructed.

-

Await Confirmation:

- The IRS will review the submission and confirm whether the proposed payment plan is accepted or if modifications are needed.

Who Typically Uses Form 433-D

Form 433-D is predominantly used by individual taxpayers who require structured payment plans to meet their federal tax obligations. Common users include those who have experienced unexpected financial difficulties, such as job loss or medical expenses, which prevent them from paying their taxes in full. Additionally, small business owners facing temporary cash flow challenges may also benefit from utilizing this form to manage tax debts without disrupting their operations.

Key Elements of IRS Form 433-D

- Taxpayer Identification: Personal details, Social Security Number, and IRS-issued identifiers.

- Debt and Payment Details: Total amount of federal tax owed, proposed payment plan, and frequency.

- Payment Method Options: Direct debit, check, or money order, with a focus on direct debit for its efficiency and reliability.

- Terms and Conditions: Clear outline of the installment agreement's conditions, including responsibilities and consequences for default.

Form Submission Methods

Form 433-D can be submitted to the IRS through several channels, depending on individual preferences and IRS requirements:

- Mail: Traditional mailing to the designated IRS address provided on the form instructions.

- Fax: For expedience, taxpayers may fax the form to the number specified by the IRS.

Additionally, submitting digitally through IRS-sponsored tools where applicable ensures quicker processing and confirmation.

Legal Use and Compliance

Form 433-D serves the legal purpose of formalizing an individual's intent to repay their tax debt under specified terms and conditions. Signing this form is a legally binding acknowledgment of the debt and the agreed-upon payment arrangement, making compliance critical. Failure to comply with the terms, such as missing payments or providing inaccurate information, can result in penalties or nullification of the agreement.

IRS Guidelines and Penalties for Non-Compliance

The IRS stipulates specific guidelines for entering into an installment agreement using Form 433-D. Taxpayers must adhere to these to avoid potential repercussions, which can include:

- Interest and Penalties: Accrual on outstanding balances until fully paid.

- Default and Revocation: The IRS can revoke the agreement for non-compliance, leading to enforced collection actions.

- Credit Impact: Reports of defaults may affect the taxpayer's credit rating adversely.

Understanding and following the IRS guidelines ensures continuation of the agreement without additional stress or legal complications.