Definition and Purpose of the 2014 Form 592-F

The 2014 Form 592-F is issued by the California Franchise Tax Board and is primarily used by partnerships and limited liability companies (LLCs). This form is designated for reporting the total withholding amount for foreign partners or members within a specific taxable year. The primary objective of this form is to ensure that taxes are appropriately withheld from distributions to foreign partners or members to meet state tax obligations.

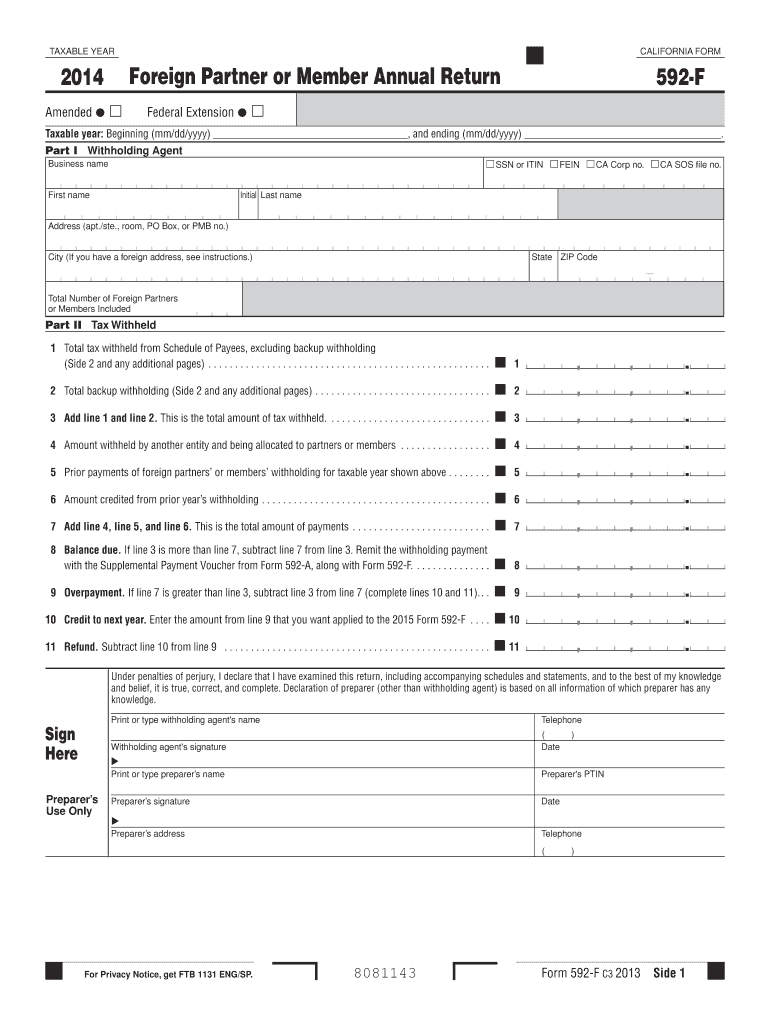

Components of the Form

- Withholding Agent Information: Includes sections where the withholding agent's details are provided, such as name, address, and identification numbers.

- Tax Withheld: Details on the total tax amount withheld for the specified period.

- Instructions for Filing: Guidelines on how to complete, amend, and submit the form are included.

How to Use the 2014 Form 592-F

Utilizing this form involves several essential steps:

- Gather Information: Collect all necessary details about the partners or members, specifically the foreign entities involved.

- Complete Withholding Details: Accurately fill out the sections related to the withheld taxes, displaying the amounts for the given year.

- Review and Submission: Before submission, ensure all information is correct, reflecting any amendments if necessary.

Importance of Accurate Completion

Accurate completion is critical to avoid penalties and ensure compliance with California state tax laws. Mistakes in reporting can lead to delays in tax processing and potential financial repercussions for the business entity.

Steps to Complete the 2014 Form 592-F

Completing the 2014 Form 592-F involves the following detailed steps:

- Identify the Withholding Agent: Enter the required identification information, making sure it's up-to-date and correct.

- List Foreign Partners or Members: Provide details on each foreign partner or member involved in the partnership or LLC.

- Calculate Withholding: Determine and record the total amount withheld during the taxable year.

- Fill in the Form: Following the prescribed format, enter all necessary information into the form.

- Double-check Entries: Verify the accuracy of all data entered to minimize errors.

- Submission: Submit the form using the methods specified by the California Franchise Tax Board.

Why Use the 2014 Form 592-F

The 2014 Form 592-F is critical for ensuring that all tax obligations are met when dealing with foreign partners or members of a business entity. By accurately withholding and reporting taxes, companies align themselves with state requirements, avoiding legal issues and potential penalties.

- Tax Compliance: Using this form keeps businesses compliant with California’s tax rules.

- Foreign Engagement Management: Helps manage tax responsibilities when engaging with foreign entities.

Key Elements of the 2014 Form 592-F

The key parts of the form provide structure and clarity to tax withholding and reporting:

Withholding Requirements

The form specifies guidelines for calculating and reporting the correct amount of tax to withhold from foreign entities.

Filing and Amending

Provides explicit instructions on how to file the form and make amendments if errors are discovered post-submission.

Important Terms Related to the Form

Understanding specific terminology is essential for accurate completion:

- Withholding Agent: The entity responsible for withholding taxes on behalf of foreign partners.

- Foreign Partner/Member: Any partner or member that resides outside the U.S. and is subject to withholding.

Legal Use and Compliance

Ensuring the form is correctly used is crucial for legal compliance:

Compliance Assurance

The form mandates accurate record-keeping and timely submission to align with California tax law, avoiding legal infractions.

Backup Withholding

Details conditions under which backup withholding must be implemented, ensuring businesses comply with broader tax obligations beyond the basics.

Filing Deadlines and Important Dates

Adherence to designated deadlines is paramount for compliance:

- Annual Submission Date: Forms should be completed and submitted by the set date for the fiscal year.

- Amendments: Any adjustments required must be addressed promptly within the provided timeline to prevent penalties.

Penalties for Non-Compliance

Failing to correctly file or comply with the 2014 Form 592-F requirements can result in significant penalties:

- Financial Penalties: Direct monetary fines for late submissions or incorrect data.

- Legal Ramifications: Potential legal challenges or audits from the state tax authority.

Understanding these elements ensures that businesses remain compliant with the tax requirements as outlined in the 2014 Form 592-F from the California Franchise Tax Board.