Definition & Meaning

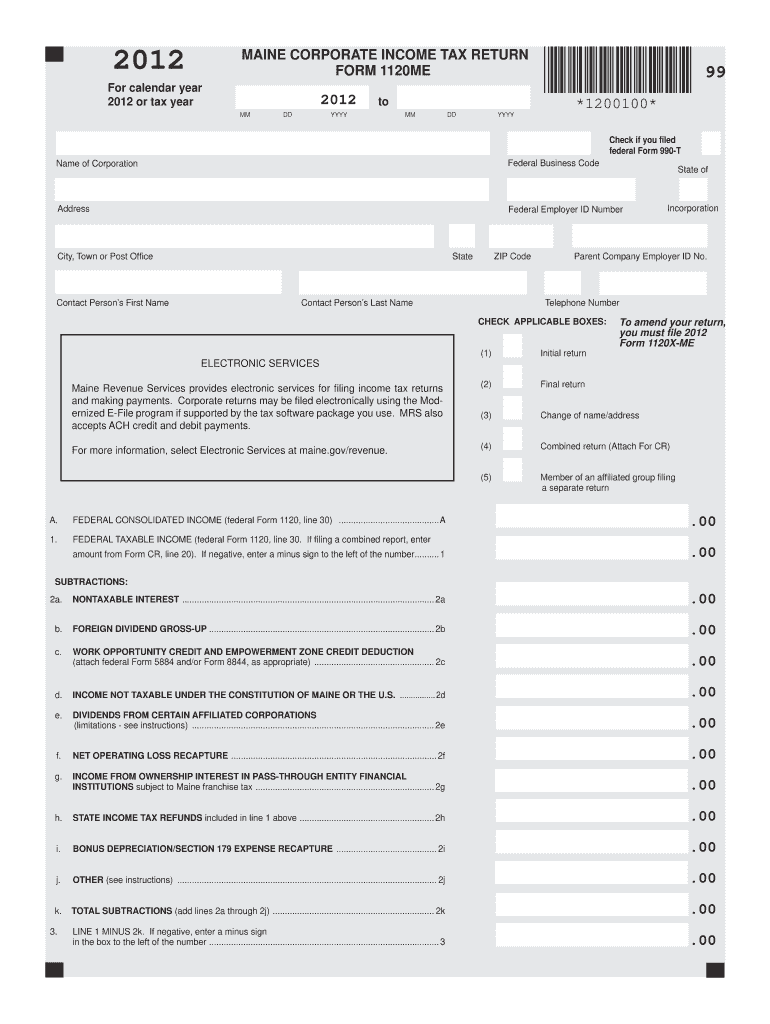

The Maine Form 1120ME for 2012 is a corporate income tax return form used by corporations conducting business in Maine. This form is required to report income, calculate state taxes, and ensure compliance with Maine's taxation requirements. It includes categories like federal taxable income, adjustments to income, and specific schedules for calculating tax liabilities.

Key Purposes of the Form

- Tax Reporting: Corporations utilize this form to declare their income for state tax determination.

- Income Adjustments: The form adjusts federal taxable income to comply with Maine tax laws.

- Tax Credit Claims: Corporations can claim state-specific tax credits and deductions using this form.

Steps to Complete the Maine Form 1120ME 2012

Filing the Maine Form 1120ME involves several steps to ensure accurate reporting and compliance with state tax regulations.

- Gather Documentation: Collect federal tax return information, financial statements, and details on income adjustments.

- Report Federal Taxable Income: Enter the corporation's federal taxable income as the starting point.

- Make Adjustments: Calculate necessary adjustments to income, including any state-specific deductions or additions.

- Calculate Maine Taxable Income: Apply Maine-specific tax rates and credits to determine the taxable income.

- Complete Schedules: Fill out any required schedules for apportionment, alternative minimum tax, or other tax factors.

- Review and Submit: Double-check all calculations, complete any additional state forms, and submit the return by the deadline.

Who Typically Uses the Maine Form 1120ME 2012

Eligible Entities

- C Corporations: The primary users, as they're required to report their income and calculate tax liabilities.

- S Corporations: While they often pass income through to shareholders, certain state-specific filing requirements may necessitate this form.

- Subsidiaries of Multinational Corporations: These entities use the form for state tax obligations resulting from Maine operations.

Usage Scenarios

- Corporations headquartered in Maine: Must file to report in-state income and calculate state taxes.

- Out-of-state corporations with Maine business activities: Required to file if their business activities within Maine meet certain thresholds.

Important Terms Related to Maine Form 1120ME 2012

Relevant Financial Concepts

- Federal Taxable Income: The initial reference point for calculating state tax obligations.

- Apportionment: A method used by multistate businesses to determine the portion of income subject to Maine tax.

- Alternative Minimum Tax (AMT): Ensures that corporations pay a minimum amount of tax, regardless of deductions and credits.

Filing Components

- Schedules: Detailed forms attached to the main return to itemize various tax components.

- Non-business Income: Income not directly related to business operations, requiring special treatment.

- Carrybacks and Carryforwards: Techniques that allow losses to offset taxable income in past or future years.

Filing Deadlines / Important Dates

Annual Due Dates

- April 15: Typical due date for calendar year filers.

- Fiscal Year Filers: Due by the 15th day of the fourth month following the end of the fiscal year.

Extension Details

- Automatic Extensions: Corporations may request a six-month extension; however, any tax due must still be paid by the original deadline to avoid penalties.

Form Submission Methods (Online / Mail / In-Person)

Available Submission Options

- Online Filing: Encouraged for speed and convenience, often resulting in quicker processing times.

- Mail: Corporations can mail completed forms to the Maine Revenue Services, though this method may involve longer processing times.

- In-Person: Limited options may be available for direct submission at designated state tax offices.

Selecting the Best Method

- Online Benefits: Offers quicker feedback and error checking.

- Mail and In-Person: May be necessary for businesses preferring traditional or need to submit additional paper documentation.

Penalties for Non-Compliance

Potential Consequences

- Late Filing Penalties: Fines imposed for failure to file by the due date without an extension.

- Underpayment Penalties: Additional charges for failing to pay the full tax liability owed by the deadline.

- Incorrect Reporting: Consequences for intentionally or inadvertently submitting inaccurate information, leading to tax underpayment.

Avoiding Penalties

- Timely Filing and Payment: Ensuring all forms and payments are submitted by the deadline.

- Accurate Documentation: Double-checking entries to avoid misreporting taxable income or other critical figures.

State-Specific Rules for the Maine Form 1120ME 2012

Unique Maine Tax Codes

- Business Property Tax Programs: Incentives that may alter a corporation's taxable income.

- State Aerospace & Maritime Credits: Specific credits available for qualified corporations operating in these industries.

- Mandatory PTET Election: A pass-through entity tax affecting how income is reported and taxed.

Compliance with Maine Laws

- Understand Local Legislation: Corporations must align their filings with both federal guidelines and state-specific regulations.

- Seek Local Expertise: Utilize Maine-based tax professionals to navigate complex state statutes, ensuring adherence to local legal standards.

Software Compatibility (TurboTax, QuickBooks, etc.)

Supported Platforms

- TurboTax: Offers specialized modules for corporate tax filings, including state-specific forms like the 1120ME.

- QuickBooks: Assists with data aggregation and preparation, easing the process of transferring figures to the state return.

- DocHub Integration: Incorporate document workflow tools for secure management and submission of digital forms.

Benefits of Using Tax Software

- Error Reduction: Automated calculations and checks minimize mistakes.

- Convenience: Ease of data transfer and the ability to e-file directly through compatible platforms.

- Efficiency: Streamlined processes significantly cut preparation and filing time, ensuring compliance and avoiding penalties.