Definition and Meaning of the 2 Form

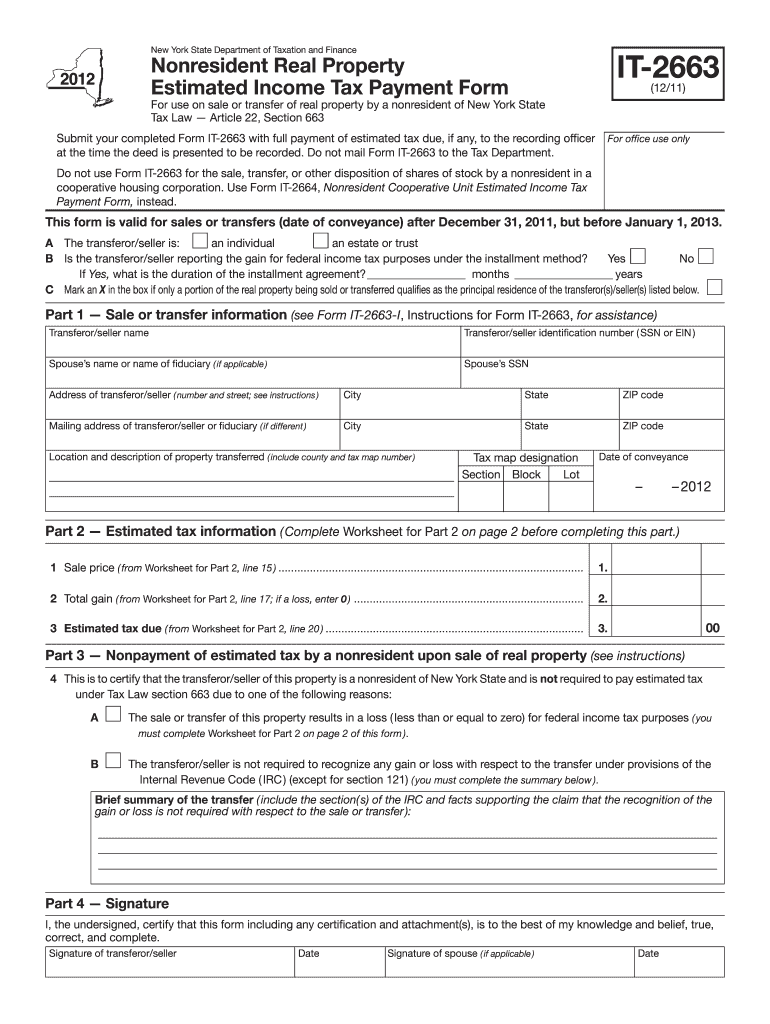

The 2 form is officially known as Form IT-2663, utilized by the New York State Department of Taxation and Finance. It is primarily used by nonresidents engaged in the sale or transfer of real property located in New York State. This form is essential for reporting estimated income tax payments associated with such transactions. The form facilitates the computation and documentation of estimated taxes owed to the state by nonresidents, ensuring compliance with New York State tax statutes.

Understanding the core purpose of Form IT-2663 is essential for anyone involved in real estate transactions where nonresidents are the sellers. The need for this form arises from New York State's regulations, which require nonresident sellers to account for income tax resulting from capital gains on properties located within the state.

How to Use the 2 Form

Utilizing Form IT-2663 involves several critical steps to ensure accurate submission and compliance with state laws. Here's a step-by-step guide for its correct usage:

-

Determine Applicability: Confirm that the transaction involves the sale or transfer of New York State real property by a nonresident.

-

Gather Necessary Information: Collect details related to the property being transferred, including address, sale price, and closing date.

-

Calculate Estimated Tax: Use the form's instructions to compute the estimated tax owed on the transaction. This involves calculating the gain from the sale and applying the state tax rate.

-

Complete the Form: Enter all required information accurately, including personal details of the seller, property specifics, and calculated tax.

-

Submit with Payment: The form and the payment for estimated taxes must be submitted simultaneously when recording the deed for the transaction.

Correct usage of the 2 form is vital for compliance, ensuring that estimated taxes are paid before or during property recording.

Steps to Complete the 2 Form

Completing Form IT-2663 can be broken down into detailed steps:

-

Fill Personal Information: Begin by entering the seller's personal information, including full name, address, and Social Security Number or ITIN.

-

Provide Property Details: Enter complete details about the property, such as the physical address and description of the property type.

-

Calculate Gain or Loss: Utilize section instructions on the form to compute the gain or potential loss from the property sale.

-

Enter Estimated Tax: Based on the taxable gain, calculate and record the amount of estimated tax owed.

-

Sign and Date: Ensure that the seller or authorized person signs and dates the form before submission.

Following these steps methodically will help avoid errors and ensure that the form is filled accurately.

Important Terms Related to 2 Form

Understanding specific terms related to the IT-2663 form is crucial:

- Transferor/Seller: The entity or individual selling or transferring the property.

- Estimated Tax Payment: The calculated tax owed on the gain from the property sale by a nonresident.

- Nonresident: An individual or entity that does not reside in New York State but owns real property within the state.

- Gain from Sale: The profit made from selling or transferring the property, calculated as the difference between the sale price and the property's cost basis.

Knowledge of these terms aids in accurately interpreting and completing the form.

Filing Deadlines and Important Dates

Timeliness is essential for the 2 form:

- At the time of deed recording: The form, along with the payment, must be submitted on or before the deed is recorded to avoid penalties.

- Incomplete Submission Deadline: If additional information is needed, ensure completion by specified dates to prevent fines.

Understanding the importance of these deadlines ensures compliance and helps in avoiding unnecessary penalties.

Legal Use of the 2 Form

The legal purpose of the form is to ensure that New York State receives due taxes on real property sales by nonresidents. This form is legally mandated, reflecting the state's requirement for tax collection based on gains from in-state property transactions by those who do not reside within the state. Comprehension of the legal implications is important for nonresident sellers to fulfill their tax obligations lawfully.

Penalties for Non-Compliance

Failure to accurately submit Form IT-2663 can lead to severe consequences:

- Fines and Interest: Unpaid taxes can accrue interest, and late filing can result in financial penalties.

- Legal Action: Persistent non-compliance might lead to legal actions, increasing costs and complexities for the seller.

Non-compliance is a critical issue, and awareness of the penalties can incentivize timely and correct submissions.

Examples of Using the 2 Form

Real-world scenarios emphasize its practical application:

- Example 1: A California resident selling a vacation home in the Catskills would need to complete Form IT-2663 to report and pay New York State taxes on the gain from this sale.

- Example 2: A corporation based in Florida decides to sell its commercial property in Manhattan. Completion of the 2 form would facilitate the proper reporting and payment of estimated taxes on the transaction.

Understanding these examples helps visualize the form's application in various transaction scenarios across different contexts.