Definition & Meaning

The "2013 Connecticut form" often refers to a type of tax document such as the Form CT-W4, which is used by employees in Connecticut to specify their state tax withholding preferences. This form ensures that the correct amount of state income tax is withheld from their paycheck based on their individual circumstances, such as filing status and expected annual income. It's a critical component for individuals working in Connecticut to comply with state tax laws and avoid unexpected tax liabilities at the end of the tax year.

How to Obtain the 2013 Connecticut Form

Accessing the 2013 Connecticut form is straightforward and can be done through multiple channels. The form can be downloaded directly from the Connecticut Department of Revenue Services website, ensuring access to the most accurate and official version. Alternatively, employers often provide this form to new employees during onboarding processes. For those seeking physical copies, local tax offices or public libraries may also have this document available. If you prefer digital convenience, platforms like DocHub facilitate this by allowing imports directly from cloud services such as Google Drive or Dropbox.

Steps to Complete the 2013 Connecticut Form

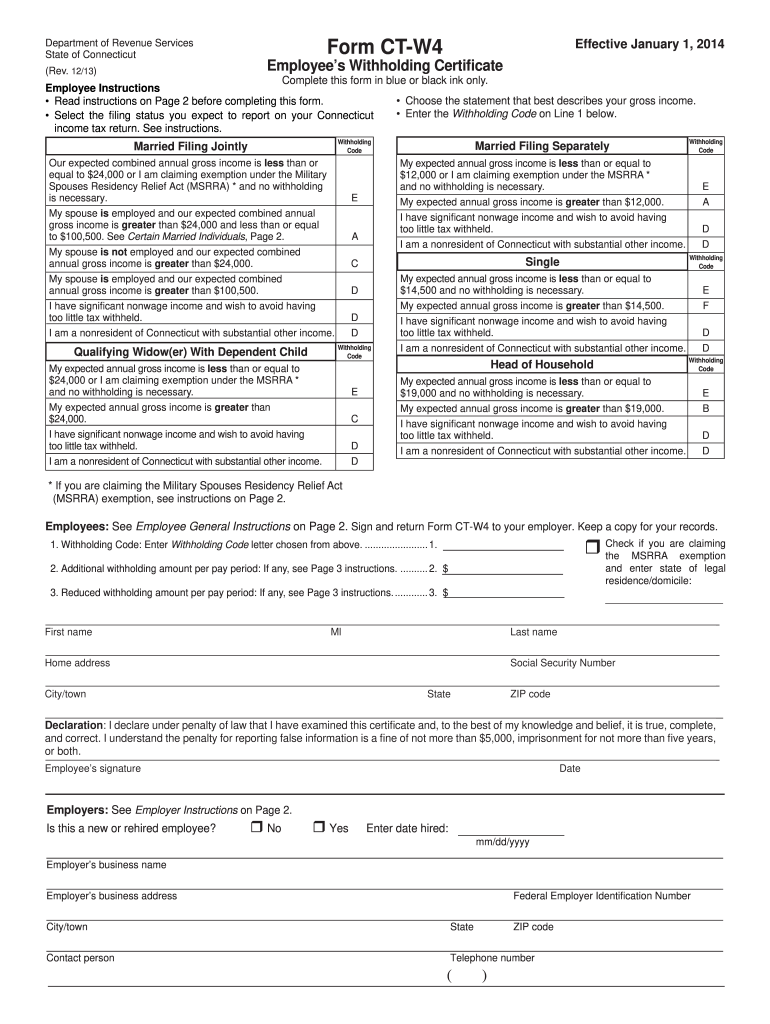

- Personal Information: Begin by entering your full name, address, and Social Security number at the top of the form.

- Withholding Code: Use the instructions provided in the form to determine your withholding code based on your expected gross income and filing status. This code dictates how much tax should be withheld from your paycheck.

- Military Exemptions: If applicable, detail any military status information that affects withholding exemptions.

- Sign and Date: After filling in the necessary sections, don’t forget to sign and date the form to authenticate your responses.

- Submit to Employer: Once completed, submit the form to your employer, not to the state; this facilitates proper tax withholding.

Important Terms Related to the 2013 Connecticut Form

- Withholding Code: This code determines the amount of income tax withheld from your paycheck.

- Filing Status: Refers to your tax filing classification, such as single, married, or head of household.

- Exemption: A provision that reduces taxable income and, in this context, may alter your withholding requirements.

- Gross Income: Total income received before taxes and other deductions.

Legal Use of the 2013 Connecticut Form

The 2013 Connecticut form must be used in compliance with state-specific tax laws. Employees use it to authorize their employers to withhold a certain amount from their wages for state income tax, which helps prevent underpayment or overpayment of taxes. Employers, on the other hand, are legally obligated to process and maintain accurate records of these forms for every employee, ensuring all deductions align with the represented data. Non-compliance can lead to penalties or legal action.

State-Specific Rules for the 2013 Connecticut Form

Connecticut-specific tax rules are integral to completing the form accurately. The state has its specific guidelines for withholding rates and exemptions, which differ from federal requirements. It's vital to review these rules annually as they can change with new legislation. Connecticut residents must also understand credits and deductions unique to the state, ensuring their withholding is neither more nor less than necessary.

Penalties for Non-Compliance

Failure to accurately complete or submit the Connecticut form can lead to several penalties. For employees, underpayment due to incorrect withholding can result in tax underpayment penalties at the end of the fiscal year. Employers who do not collect or process these forms correctly could face audits and fines for improper withholding. Maintaining compliance requires timely updates to the form if personal or financial circumstances change.

Form Submission Methods

Forms can be submitted in a few different ways, offering flexibility to accommodate various preferences. Most commonly, employees submit the form directly to their employer’s HR department. While traditional paper submission is still widely used, electronic submission through email or internal HR systems is gaining popularity for its convenience. Regardless of the method, ensure submission before any payroll cycles to enforce proper withholding without delay.