Definition and Meaning of FORM 720 VI

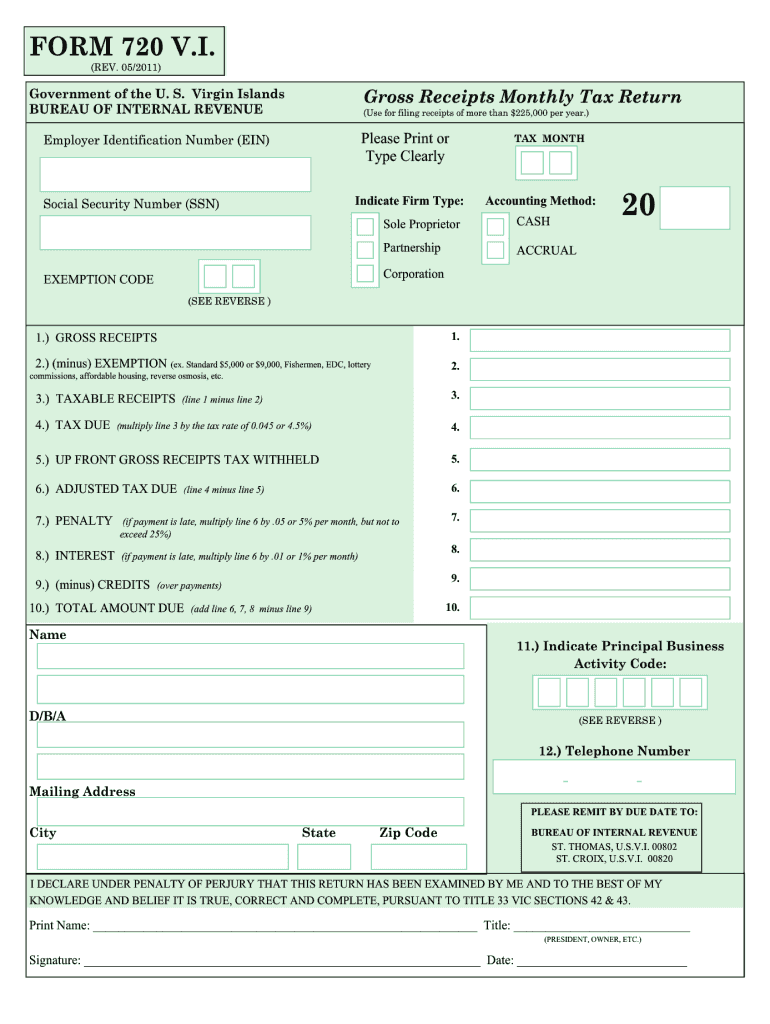

FORM 720 VI, officially titled the Virgin Islands Gross Receipts Monthly Tax Return, is a tax form used to report and pay gross receipts tax for businesses operating in the U.S. Virgin Islands. This form is mandatory for entities whose annual gross receipts exceed $225,000, aiming to document all taxable and exempt receipts while calculating monthly owed taxes. The completion of FORM 720 VI is essential for compliance with the Virgin Islands Bureau of Internal Revenue, ensuring accurate tax reporting and payment.

Steps to Complete FORM 720 VI

-

Gather Required Information: Before filling out FORM 720 VI, collect all necessary financial data, including total gross receipts, detailed exemptions, and any penalties for prior late payments.

-

Fill Out Taxable Sections: Enter gross receipts for the month. Subtract allowable exemptions to determine taxable receipts, then calculate the gross receipts tax based on current rates.

-

Verify Entries: Double-check all entries for accuracy. Ensuring precise figures is crucial to avoid additional liabilities or audits.

-

Complete Additional Sections: If applicable, address penalties for late submission. Present the total amount due, combining the regular tax and any penalties.

-

Final Review and Signature: Carefully review the entire form for mistakes or omissions. Sign the document to validate the information provided.

-

Submission: Submit the form to the Virgin Islands Bureau of Internal Revenue by the specified deadline, using the appropriate method of delivery, such as mail or electronic submission.

Submission Methods for FORM 720 VI

-

Mail: Traditional mail remains a viable option. Ensure the form is postmarked by the deadline to avoid penalties.

-

Electronic Submission: Many taxpayers prefer electronic filing due to its convenience and speed. Verify compatibility with the Bureau's digital submission system before proceeding.

-

In-Person: Delivering forms in-person to the local Bureau office ensures immediate receipt and verification but might not be practical for all filers.

Filing Deadlines and Key Dates

-

Monthly Filing Requirement: FORM 720 VI is due on the fifteenth day of the month following the reporting period. Timely submission is crucial to avoid penalties.

-

Extension Requests: Under specific conditions, extensions may be granted. However, these do not extend the time for payment of taxes due.

-

Penalty Dates: Late filings incur penalties, emphasizing the importance of meeting or requesting an extension before deadlines.

Required Documents for FORM 720 VI

-

Financial Statements: Provide comprehensive documentation of all income streams and exemptions.

-

Previous Tax Forms: Past submissions for comparison and accuracy in reporting ongoing data.

-

Proof of Exemptions: Maintain records supporting any exemptions claimed on the form.

Penalties for Non-Compliance

-

Monetary Fines: Failing to file or pay on time can lead to fines proportional to the overdue amount. These fines incrementally increase depending on the duration of non-compliance.

-

Interest on Unpaid Taxes: Interest may accrue on unpaid taxes, compounding monthly until the outstanding balance is resolved.

Who Typically Uses FORM 720 VI

Primarily utilized by business entities within the U.S. Virgin Islands, FORM 720 VI is typically required for corporations, partnerships, and sole proprietors. These entities report gross receipts to comply with local tax laws, ensuring accurate financial accountability to the Virgin Islands Bureau of Internal Revenue.

IRS Guidelines and Compliance

While FORM 720 VI is specific to the Virgin Islands Bureau of Internal Revenue, IRS guidelines for general tax compliance still apply. Taxpayers must remain aware of both federal and territorial regulations to fully comply with all governing bodies. This dual awareness can prevent overlapping legal issues and ensure overall congruity in tax reporting.