Definition & Meaning

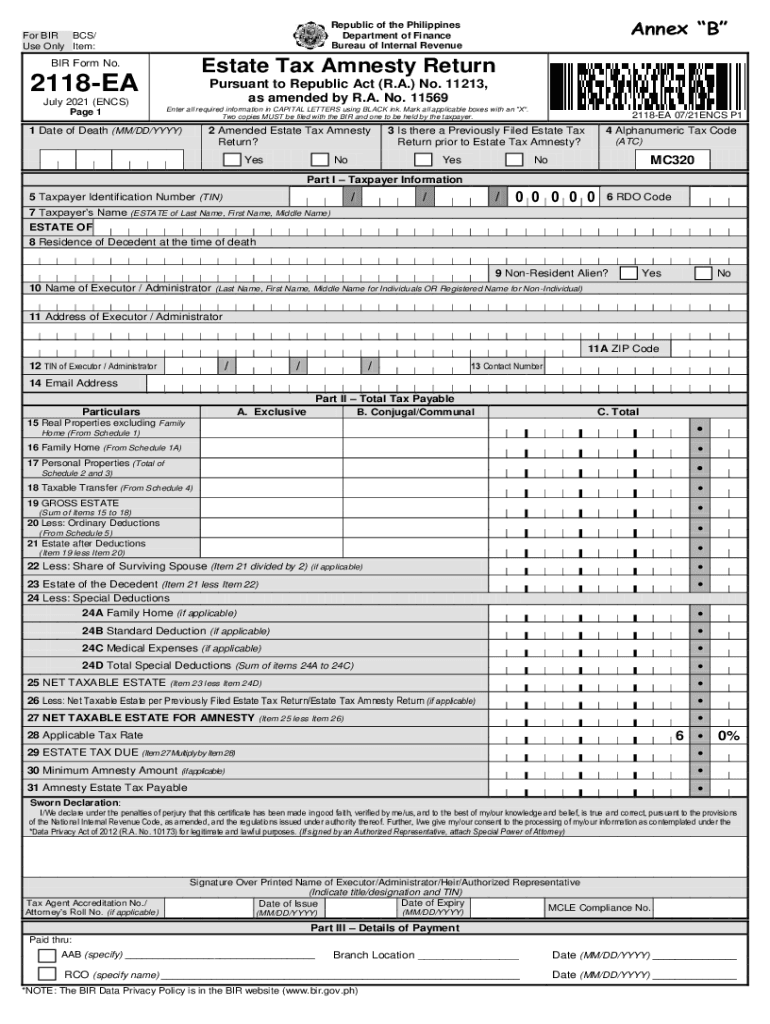

The "assets kpmgcontentdamRepublic of the Philippines For BIR BCS Use Only Estate Tax" refers to a specific form utilized by individuals or entities in the Philippines to report and settle estate taxes. This process is part of the compliance requirements set by the Bureau of Internal Revenue (BIR) under Republic Act No. 11213, which has been amended by Republic Act No. 11569. The form facilitates the declaration and computation of the estate tax due to the Philippine government following the transfer of assets from a deceased individual to their heirs or beneficiaries.

Steps to Complete the Estate Tax Form

-

Collect Necessary Information: Gather all relevant documents, including the decedent’s death certificate, testamentary documents, and a comprehensive list of assets.

-

Identify Taxable Assets: Determine all assets that are subject to estate tax, including real estate, cash, stocks, and any business interests.

-

Calculate the Gross Estate: Sum the value of all taxable assets to arrive at the gross estate.

-

Assess Applicable Deductions: Deduct authorized deductions such as funeral expenses, debts, and medical expenses from the gross estate.

-

Compute the Net Estate: Subtract the total deductions from the gross estate to determine the net estate value.

-

Determine the Estate Tax Due: Apply the appropriate estate tax rate to the net estate to calculate the tax due.

-

Complete the Form: Fill in the details on the form, including the computed estate tax, and ensure all sections are accurately completed.

-

Submission: Submit the completed form to the BIR with any required attachments and payment of the calculated tax.

Required Documents

Filing the estate tax form requires the following documentation:

- Death Certificate: An official document confirming the death of the individual whose estate is being settled.

- Testate or Intestate Documents: Documents such as a will or court order proving how the estate is to be divided.

- Asset Inventory: A detailed list of assets owned by the deceased, including valuations.

- Liabilities and Deductions: Proof of debts, funeral costs, and other relevant deductions.

- Identification Documents: IDs of the executor, heirs, or beneficiaries involved in the estate.

Filing Deadlines / Important Dates

The estate tax form must be filed within six months from the decedent’s date of death. Extensions may be requested, but they are subject to the approval of the BIR and could incur additional interest.

- Six-Month Window: Initial deadline for filing.

- Extension Requests: Must be justified and are not automatically granted.

- Penalties: Late filings may result in interest and surcharges.

Form Submission Methods

- Online Submission: The form can be processed through the BIR’s online portal, which facilitates electronic submission of documents and payment.

- In-Person Filing: Submit the completed form and required documents directly at BIR offices.

- Mail Submission: Documents may be mailed, but tracking and confirmation are advised to ensure they are received on time.

Legal Use of the Estate Tax Form

This form is legally required for the payment and settlement of estate taxes in the Philippines. It ensures the lawful transfer of estate assets and prevents legal issues from arising in the future. Failure to properly file and settle these taxes can result in penalties, interest, and potential legal action.

- Compliance: Legal obligation under Philippine tax law.

- Transparency: Clear declaration of assets and compliance with tax responsibilities.

- Legal Protection: Protects against challenges to the estate distribution.

Penalties for Non-Compliance

Non-compliance with filing requirements can result in significant penalties:

- Surcharges: An additional charge based on the unpaid tax amount.

- Interest: Compounded daily interest on overdue taxes.

- Legal Action: Possible court proceedings initiated by the BIR for continued non-compliance.

Key Elements of the Estate Tax Form

- Taxpayer Information: Details of the decedent, including name, address, and taxpayer identification number.

- Property Details: Specifics of all properties, both immovable and movable, comprising the estate.

- Payment Schedules: Defined timelines and methods for tax payment, allowing for installment setups where applicable.

- Declaration and Signature: Confirmation of the accuracy of information provided, signed by the executor or administrator of the estate.

Each section of the form requires careful attention to ensure accurate reporting and compliance with Philippine tax laws.