Definition & Meaning

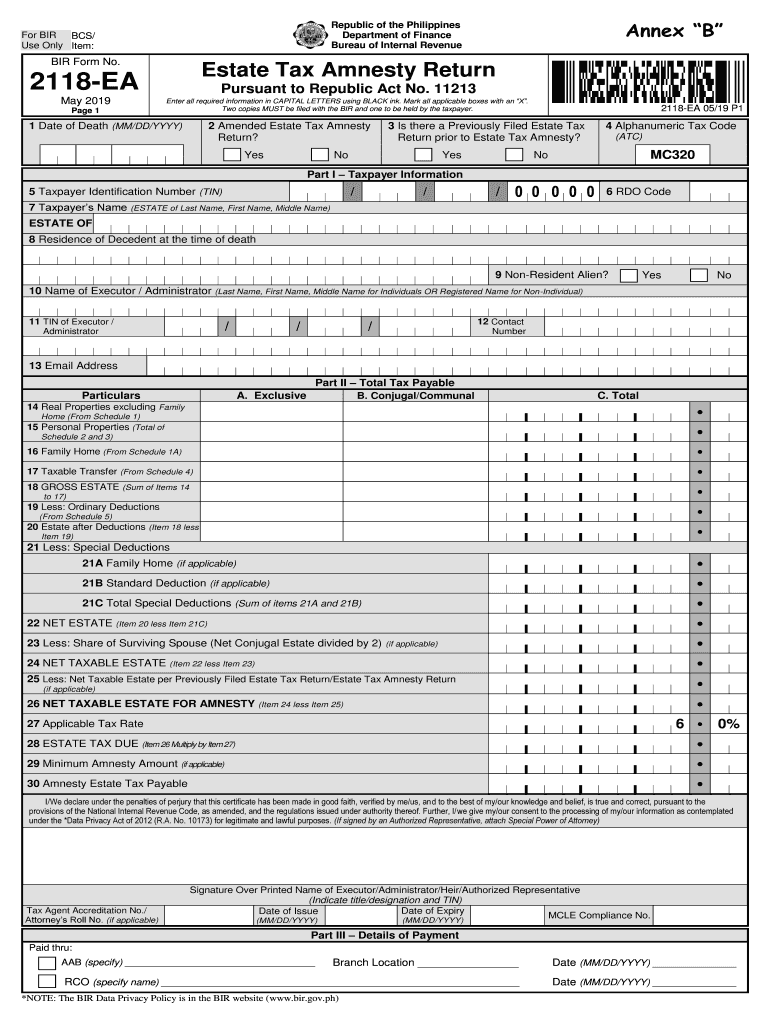

The BIR Form No. 2118-EA, often referred to simply as "BIR Form 2118 EA," is the Estate Tax Amnesty Return designed for use in the Republic of the Philippines. This form facilitates the declaration and settlement of estate taxes under the provisions of Republic Act No. 11213. It enables taxpayers to report the details of the deceased's estate, including all pertinent real and personal properties. Proper completion of this form is crucial for the accurate calculation and payment of estate-related taxes.

How to Use the BIR Form 2118 EA

Using the BIR Form 2118 EA involves several precise steps to ensure compliance with legal requirements:

- Gather Necessary Information: Collect all relevant documents relating to the estate, including property titles, bank statements, and other financial records.

- Complete Taxpayer Information: Enter the required personal and estate details about the deceased individual, including their legal representatives.

- Outline Property Details: List all real and personal properties belonging to the estate, ensuring accurate description and valuation.

- Calculate Deductions: Identify any permissible deductions applicable to the estate, which can reduce the total taxable amount.

- Determine Total Tax Payable: Use the provided schedules for detailed tax calculations, encapsulating total liabilities.

- Review and Finalize: Verify all entries for accuracy before final submission to avoid errors that could lead to complications or penalties.

Steps to Complete the BIR Form 2118 EA

Completing the BIR Form 2118 EA requires careful attention to detail:

-

Start with Taxpayer Information:

- Fill out personal details of the deceased.

- Include the names and contact details of the estate's legal representatives.

-

Property Schedules:

- List each piece of real estate with accompanying documentation.

- Detail all personal properties, such as vehicles, jewelry, and other assets.

-

Deductions and Liabilities:

- Identify deductions such as funeral expenses and outstanding debts.

- Record these deductions accurately to ensure compliance.

-

Tax Calculation:

- Use specific tables within the form to calculate the exact tax amount.

- Adjustments must be made according to the prevailing tax laws.

-

Filing:

- File the form in duplicate with the Bureau of Internal Revenue (BIR).

- Ensure both copies are signed and include all necessary attachments.

Required Documents for BIR Form 2118 EA

Preparation of the BIR Form 2118 EA necessitates specific documentation:

- Death Certificate: Verification of the deceased's date of death.

- Property Titles: Legal documents validating estate ownership.

- Financial Records: Bank statements and investment account reports.

- Payment Receipts: Documentation of expenses related to estate management.

- Identification Documents: ID of executors or administrators managing the estate.

Each document serves to substantiate the claims made within the form, ensuring legal and fiscal accuracy.

Legal Use of the BIR Form 2118 EA

The BIR Form 2118 EA is used within a legal framework to:

- Settle Estate Taxes: Formalize the payment of taxes owed on a deceased's estate.

- Facilitate Tax Amnesty: Allow taxpayers to clear liabilities under the amnesty program.

- Ensure Compliance: Adhere strictly to national tax regulations to avoid penalties.

This form is critical for executors responsible for closing an estate, serving as an official record of their tax obligations.

Key Elements of the BIR Form 2118 EA

Key components within the BIR Form 2118 EA include:

- Taxpayer Information: Details about the deceased and the legal representatives.

- Property Listings: Comprehensive lists categorized into real and personal assets.

- Schedules and Deductions: Sections dedicated to tax computations and allowable deductions.

- Authorization and Declaration: Signature fields acknowledging the accuracy and truthfulness of the information provided.

Understanding each section is vital for the precise completion of the form.

Filing Deadlines / Important Dates

Timely submission of the BIR Form 2118 EA is crucial:

- Filing Period: Typically within a specified timeframe after the individual's death.

- Deadline for Payment: The constituted deadline for tax settlements to avoid late fees or penalties.

- Extensions: Conditions or precedents for granting extensions must be understood and adhered to.

Observing deadlines ensures compliance and avoids unnecessary financial penalties.

Penalties for Non-Compliance

Failure to properly file or settle dues via the BIR Form 2118 EA can result in:

- Late Fees: Imposed for missing the application filing deadline.

- Interest Charges: Additional costs accumulated on unpaid taxes.

- Legal Repercussions: Possible legal actions, including fines or levies, for continuous non-compliance.

The severity of these penalties underscores the importance of timely and accurate submission.