Definition and Meaning

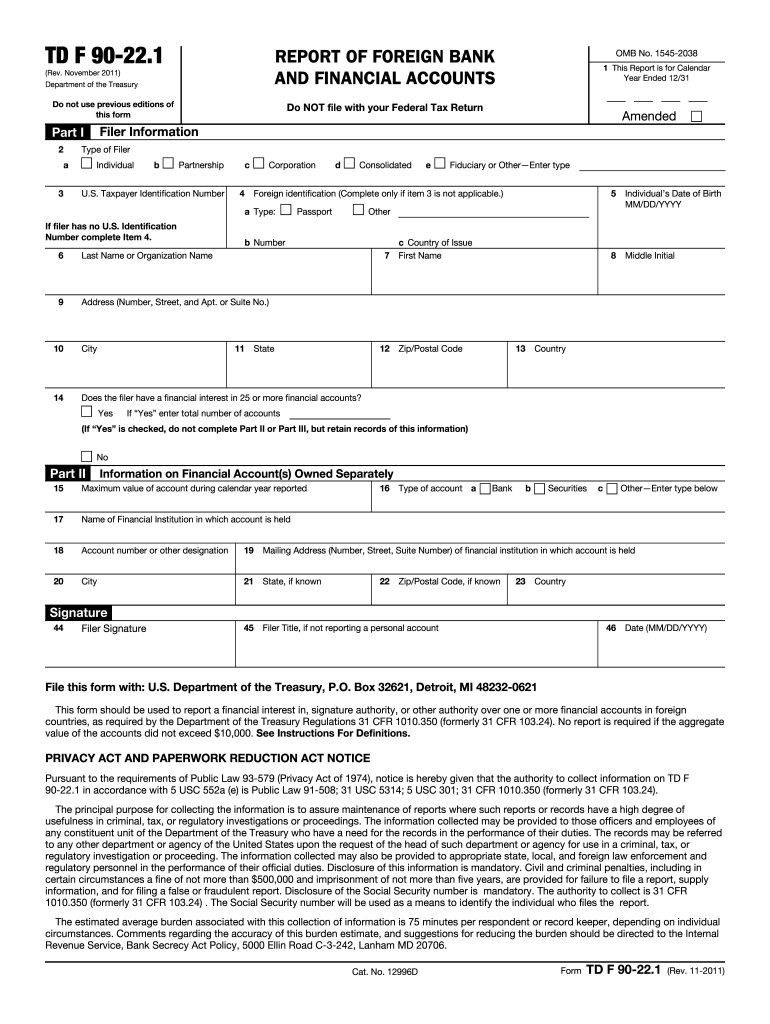

The 2011 TD F 90-22.1 form, also known as the Report of Foreign Bank and Financial Accounts (FBAR), is a crucial document for U.S. persons who hold financial interests or signature authority over foreign financial accounts exceeding $10,000 during the calendar year. This form allows individuals and entities to report their foreign accounts, thereby complying with U.S. tax regulations. Filing this form is essential to help the Department of the Treasury prevent tax evasion and ensure transparency in financial dealings.

How to Use the 2011 TD F 90-22.1 Form

To effectively use the 2011 TD F 90-22.1 form, you must accurately report each foreign account. Prepare to provide details such as the account number, the name and address of the foreign institution, and the maximum account value during the year. It is vital to double-check all entries for accuracy. Recheck the prerequisites, like meeting the financial threshold and identifying all foreign accounts applicable. This ensures compliance and minimizes issues during filing.

Steps to Complete the 2011 TD F 90-22.1 Form

-

Gather Required Information: Collect your account numbers, the maximum yearly account balances, and details of the foreign financial institutions.

-

Access the Form: Obtain the form through the Financial Crimes Enforcement Network (FinCEN) website or tax software platforms that support FBAR filings.

-

Fill in Personal Details: Complete sections requiring your personal identification, including name, address, and Social Security Number.

-

Report Account Details: Enter details for each foreign account, including its type, institution name, account number, and highest annual value.

-

Confirm and Submit: Review the completed form for accuracy, make any necessary corrections, and electronically submit it via the FinCEN's BSA E-Filing System.

Filing Deadlines and Important Dates

The deadline for submitting the FBAR was traditionally June 30 of the following year, without options for extensions. However, current regulations align the FBAR due date with the federal tax return deadline, which is April 15, with an automatic extension available until October 15. Ensuring timely submission of the 2011 TD F 90-22.1 form is vital to avoid any penalties, which are severe for late submissions.

IRS Guidelines

The IRS provides comprehensive guidelines governing the completion and filing of the FBAR. These guidelines include determining your filing requirement based on account type and balance, understanding the threshold limit, and the methods for reporting joint accounts or signature authority. It’s important to remain current with any updates, especially changes impacting compliance requirements.

Penalties for Non-Compliance

Failing to file the 2011 TD F 90-22.1 form, or filing inaccurately, can result in substantial penalties. Non-willful violations may incur penalties up to $10,000 per violation, whereas willful violations can attract harsher penalties, potentially involving the greater of $100,000 or 50% of the account balances. Understanding and adhering to these rules prevents long-term legal and financial repercussions.

Who Typically Uses the 2011 TD F 90-22.1 Form

The form is generally used by individual U.S. taxpayers and entities, such as corporations, partnerships, and trusts, who hold foreign bank accounts. This includes expatriates, dual citizens, and anyone with fiscal interests in overseas accounts. Notably, financial professionals managing client accounts may have signature authority and thus need to comply with FBAR requirements.

Key Elements of the 2011 TD F 90-22.1 Form

- Account Information: Includes the type of account, identifying number, and institution's name and address.

- Financial Limitations: Only accounts surpassing $10,000 at any point require reporting.

- Joint Accounts Reporting: Additional complexities arise when accounts have multiple owners; both holders might need to file.

Understanding these elements assists in correctly filling out and submitting the FBAR, ensuring U.S. legal compliance.