Definition and Meaning of a Foreign Account Bank

A foreign account bank generally refers to accounts held in banks located outside the account holder’s country of residence. In the context of U.S. residents, these accounts are typically located in financial institutions abroad. Foreign bank accounts are often used for various purposes, such as business transactions, investments in foreign currency, and personal savings in a jurisdiction outside the United States. Understanding the nature of these accounts is crucial for compliance with U.S. regulations, especially concerning taxation and reporting requirements.

Key Characteristics

- Location: A foreign account is held in a bank situated outside the borders of the United States.

- Purpose: These accounts serve various functions including business transactions, investment portfolios, and secure savings.

- Regulation: Managed under U.S. laws that require reporting of financial interests for transparency and compliance.

Examples

- An American businessman might maintain a foreign account in Switzerland for international business transactions.

- An expatriate living abroad could have a personal savings account in a local financial institution.

How to Use a Foreign Account Bank

Utilizing a foreign account bank involves understanding both the utility of such accounts and the obligations that come with them. Users typically leverage these accounts for managing international transactions, securing assets in diverse currencies, or even as tax-efficient investment tools.

Practical Uses

- International Business: Facilitating cross-border financial activity for companies with global operations.

- Investment: Access to foreign investment opportunities not available domestically.

- Currency Management: Holding funds in foreign currencies to hedge against exchange rate fluctuations.

Compliance Considerations

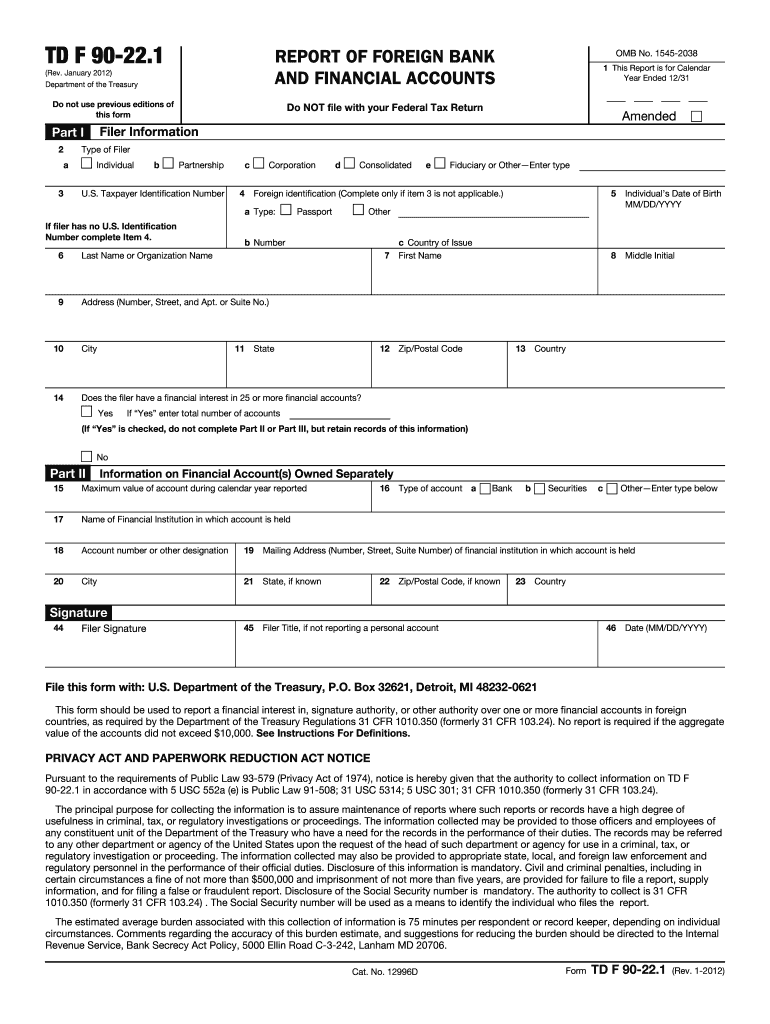

- Regular filing of the Report of Foreign Bank and Financial Accounts (FBAR) to report account balances.

- Acknowledging tax implications on foreign income and adhering to IRS regulations.

Steps to Complete the Foreign Account Bank Reporting

Completing foreign account bank reporting requires a methodical approach to ensure compliance with all legal stipulations. The key document in this reporting process is the FBAR.

- Identify Accounts: Determine which of your foreign accounts meet the reporting thresholds.

- Gather Information: Collect all necessary details such as account numbers, names on the account, and maximum balance during the year.

- File FBAR: Use FinCEN’s online system to file the FBAR by April 15th, with an automatic extension to October 15th if not filed sooner.

- Confirm Submission: Retain a copy of the submitted form for at least five years to substantiate compliance in case of audits.

Who Typically Uses Foreign Account Banks

Various individuals and entities may find foreign account banks beneficial. Those who engage in international business operations or hold assets overseas often utilize these accounts.

User Profiles

- Business Entities: Corporations with subsidiary operations abroad.

- Expatriates: U.S. citizens living abroad who need a local bank account.

- Investors: Those seeking to diversify through foreign investments.

Case Scenarios

- A multinational corporation uses a foreign bank account to manage its subsidiary's payroll and operational expenditures.

- An American retiree living in France holds a foreign account for daily expenses and local financial dealings.

Important Terms Related to Foreign Account Bank

Understanding the terminology associated with foreign account banks is essential for anyone involved in maintaining such accounts.

Glossary of Terms

- FBAR: A mandatory filing for U.S. persons with financial interests or signature authority over foreign accounts exceeding $10,000.

- FinCEN: The Financial Crimes Enforcement Network, responsible for collecting FBAR filings.

- Thresholds: Specific minimum account balances that trigger reporting obligations.

Legal Use of Foreign Account Banks

Legal use of foreign accounts involves a thorough understanding of the U.S. and foreign regulations governing such accounts to ensure compliance.

Compliance Requirements

- Reporting: Timely reporting of foreign accounts via the FBAR is mandatory for qualifying accounts.

- Taxation: Declaring all earned income from foreign accounts on U.S. tax returns.

- Legal Jurisdiction: Complying with both local laws of the foreign jurisdiction and U.S. laws.

IRS Guidelines for Foreign Account Bank Reporting

The IRS provides detailed guidelines to ensure transparent reporting of foreign accounts, aiming to prevent tax evasion and ensure proper taxation.

Key Guidelines

- File Annually: Account holders must file FBAR every year if accounts exceed the aggregate threshold.

- Penalties: Non-compliance can lead to hefty fines, ranging from $10,000 for non-willful violations to more substantial penalties for willful non-compliance.

- Record Keeping: Maintain detailed records of account information and filed FBARs for at least five years.

Penalties for Non-Compliance

The U.S. government imposes strict penalties for failure to report foreign bank accounts according to compliance regulations.

Financial Consequences

- Non-Willful Penalty: Up to $10,000 per violation for unreported accounts.

- Willful Violations: Can result in fines amounting to $100,000 or 50% of the account balance at the time of the violation, whichever is higher.

Additional Penalties

- Potential criminal charges could be pursued for consistent non-compliance or perceived intentional deception.

- Possible tax evasion investigations leading to further prosecution and penalties.

By following the structured approach detailed in each block, individuals and businesses can efficiently manage foreign accounts while ensuring compliance with U.S. treasury and tax laws.