Definition & Meaning

Publication 915, particularly the 2017 version, is an IRS document that offers guidance on the taxation of social security benefits and railway retirement benefits, specifically equivalent tier 1 benefits. It helps taxpayers determine the taxability of such benefits and provides instructions on reporting them on federal income tax returns. Additionally, it offers worksheets for calculating taxable amounts and discusses deductions and repayments related to these benefits.

How to Use the Publication Form

Using Publication 915 involves understanding its purpose in calculating the taxable portion of social security benefits. Users must follow the worksheets provided within the publication to determine if any portion of their benefits is taxable. This process requires reference to IRS worksheets, ensuring accurate calculations. Familiarity with terms such as adjusted gross income (AGI) and thresholds outlined by the IRS is crucial for effective utilization.

Steps to Complete the Publication Form

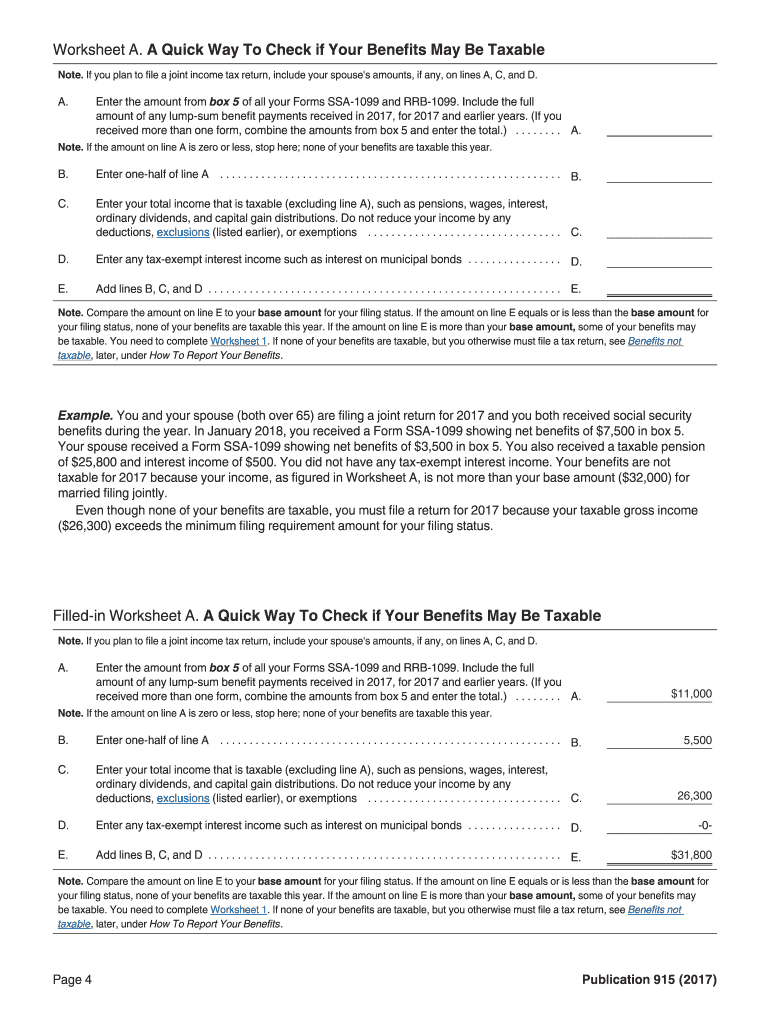

- Collect Relevant Information: Gather documents such as SSA-1099 or RRB-1099.

- Calculate Gross Income: Determine your combined income, including half of your social security benefits.

- Determine Taxable Benefits: Utilize the worksheets to identify if and what portion of your benefits is taxable.

- Input Data on Tax Return: Enter the calculated taxable portion on the relevant line of your tax return form, using Worksheet 1 and Worksheet 2 as guides.

Key Elements of the Publication Form

- Worksheets: Integral for calculating taxable social security benefits.

- Explanatory Sections: Detailed descriptions on identifying and claiming deductions.

- Tax Calculation Examples: Illustrated examples for clarity, aiding correct usage.

- FAQs and Common Scenarios: Address typical taxpayer situations.

Important Terms Related to Publication Form

- Combined Income: The total of AGI, nontaxable interest, and half of social security benefits.

- Base Amount: Predefined income levels that determine benefit taxability.

- Adjusted Gross Income (AGI): Income calculations excluding specific deductions.

- Tier 1 Railroad Retirement Benefits: Analogous to social security benefits for tax purposes.

Legal Use of the Publication Form

The use of Publication 915 is mandated by U.S. tax laws concerning the reporting of certain benefits. It ensures compliance with federal regulations by guiding taxpayers through the complex tax implications associated with social security benefits. Failing to use the publication appropriately could result in underreporting income and facing IRS penalties.

IRS Guidelines

Guidelines specify that social security benefits may be taxable depending on your filing status and income levels. It is crucial to follow the IRS instructions detailed in Publication 915 to correctly determine and report taxable benefits, especially when dealing with multiple sources of income.

Penalties for Non-Compliance

Failure to accurately report taxable social security benefits as required by Publication 915 can lead to penalties. The IRS may impose fines or demand back taxes for underreported income. Accurate adherence to the guidance outlined in Publication 915 minimizes the risk of audits and associated financial consequences.