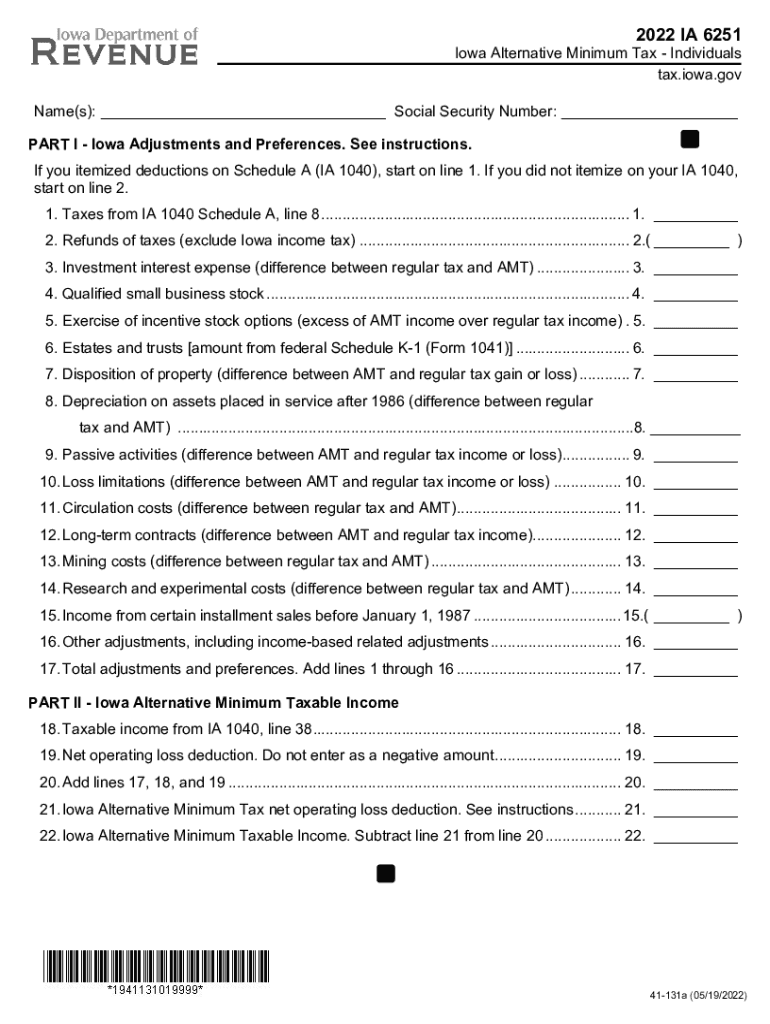

Definition & Meaning

The Iowa Alternative Minimum Tax (AMT) is a state-specific tax requirement that adjusts the amount of tax liability for certain taxpayers to ensure that they pay at least a minimum amount of taxes. This form, IA 6251, is utilized by individuals to calculate their Iowa AMT, incorporating adjustments and preferences not counted under the regular tax system. It aims to prevent high-income earners from significantly reducing tax obligations through deductions and credits.

Detailed Explanation

- Purpose: The form helps identify the minimum tax payable by recalculating taxable income after adding back deductions and exemptions allowed under the normal tax system.

- Who It Affects: Primarily targets individuals with high incomes or those with substantial deductions.

- Key Concept: Adjusts for preference items and calculates using a different taxable income base.

Steps to Complete the Iowa Alternative Minimum Tax

Completing the IA 6251 form involves several key steps to accurately determine the AMT liability.

Step-by-Step Guide

- Gather Required Documentation: Ensure all necessary tax documents, including prior tax returns, are on hand.

- Calculate Adjustments: Identify income adjustments, including interest exemptions, net operating losses, and depreciation.

- Compute Tax Preferences: Determine any preference items like depletion rates or tax-exempt interest.

- Determine AMT Income: Add adjustments and preferences to regular taxable income.

- Apply Exemptions: Use filing status to identify available exemptions.

- Finalize Calculation: Subtract exemptions from AMT income to find AMT taxable income.

Important Terms Related to Iowa Alternative Minimum Tax

Understanding terminologies used in the IA 6251 form is crucial for accuracy.

Key Terms

- Adjustments: Modifications to income like state tax refunds and certain capital gains.

- Preferences: Specific deductions not allowed in the AMT calculation, such as oil depletion.

- Exemption Amount: Variable deduction based on filing status, essential in determining final AMT.

- AMT Tax Rate: Varies from regular tax rates; specifically applied to AMT taxable income.

Who Typically Uses the Iowa Alternative Minimum Tax

Individuals who may fall under specific categories are more likely to use the IA 6251.

Typical Scenarios

- High Earners: Individuals with substantial income usually from investments or specific deduction claims.

- Itemizers: Taxpayers who itemize deductions, particularly with significant state tax payments or investment expenses.

- Business Owners: Those with depreciation-based deductions or credit claims may need to compute AMT.

State-Specific Rules for the Iowa Alternative Minimum Tax

The implementation of AMT varies by state, making it essential to understand Iowa's specific regulations.

Iowa-Specific Guidelines

- Exempt Income: Iowa considers certain municipal bond interests in calculating AMT.

- Exemption Phases-Out: High-income earners observe a phase-out in exemptions available.

- Special Deductions: Includes credits unique to Iowa for taxation computation.

IRS Guidelines

Federal IRS guidelines interact with state AMT computations, influencing adjustments.

IRS Interactions

- Federal Adjustments Impact: Certain federal allowances and income adjustments are incorporated into the Iowa AMT.

- Cross-Referencing: Iowa AMT might require referencing federal tax returns for adjusted gross income and federal preferences.

Filing Deadlines / Important Dates

Meeting deadlines is essential to avoid penalties when submitting the IA 6251 form.

Critical Dates

- Filing Deadline: Aligns with regular state tax return deadlines, typically April 15.

- Extension Procedure: Available through forms that can extend filing to October, but payment is due by April.

- Payment Timeliness: Required to avoid interest on Iowa AMT liabilities.

Penalties for Non-Compliance

Failure to comply with Iowa's AMT requirements can result in penalties and interest.

Types of Penalties

- Late Filing: Monetary penalties apply for not filing on time.

- Underpayment: Interest accrues on underpaid tax amounts from the original due date.

- Accuracy Penalty: Penalties may be imposed for substantial inaccuracies in tax calculations, particularly affecting AMT amounts.

Required Documents

Preparing necessary documentation ensures accurate completion of the IA 6251 form.

Necessary Paperwork

- Income Statements: W-2s, 1099s, and other relevant income documentation.

- Prior Year’s Tax Returns: Use these for comparative analysis and accurate adjustment calculations.

- Supporting Adjustment Documents: Receipts or statements that validate specific deductions or preferences included or eliminated in AMT calculation.

Form Submission Methods (Online / Mail / In-Person)

Submitting the IA 6251 form accurately is vital for compliance.

Submission Options

- Online Filing: Available through Iowa Department of Revenue’s platform, offering ease and speed.

- Mail Submission: Traditional paper filing is possible; keep copies of all correspondence.

- In-Person Assistance: Seek guidance or submissions at designated Department of Revenue offices if needed.