Definition & Meaning

Indiana estimated income refers to the projection of quarterly income tax payments required from businesses operating in Indiana. This process aids corporations, particularly those subject to state taxes, in anticipating their quarterly tax liabilities to avoid any underpayment penalties. Estimation methods and requirements are often based on the previous year's tax obligations and current performance indicators, enabling businesses to manage cash flow and align budgetary plans efficiently.

Relevant Terms and Considerations

- Quarterly Payments: Businesses must make four payments throughout the fiscal year.

- INTIME: Indiana Taxpayer Information Management Engine, the primary platform for payment processing and form submission.

- Underpayment Penalties: Charges incurred for failing to meet estimated tax requirements.

How to Use the Indiana Estimated Income

Businesses should integrate the Indiana estimated income framework into their financial operations by assessing fiscal performance regularly and projecting future income based on historical and real-time data. It involves calculating expected income and aligning it with tax rates for a precise quarterly payment strategy. The primary goal is to minimize tax liabilities by being well-prepared and informed about state-specific tax mandates.

Strategic Approaches

- Review Historical Data: Use previous financial statements and tax documents to estimate future obligations accurately.

- Monitor Financial Trends: Keep up-to-date with economic fluctuations affecting business income.

- Conform to Regulations: Adhere to state-specific tax laws to ensure compliance and avoid penalties.

How to Obtain the Indiana Estimated Income

Obtaining the necessary forms for calculating estimated income involves accessing the appropriate resources via the Indiana Department of Revenue or the INTIME platform. Businesses can register online to pay taxes, view account details, and manage payment activities. Resources and guides for filling out required forms are also available to aid in completing submissions accurately.

Key Resources

- INTIME Portal: Offers a comprehensive guide for managing and submitting estimated income tax forms.

- Department of Revenue: Provides printed forms and information booklets.

- Tax Advisors: Professional advice ensures accuracy and compliance with state tax expectations.

Steps to Complete the Indiana Estimated Income

Completing the Indiana estimated income process involves a series of detailed steps. Businesses must calculate potential earnings, apply the correct tax rate, and submit estimated payments by set deadlines.

- Calculate Potential Income: Evaluate profit forecasts and historical performance.

- Determine Tax Rate: Apply the current state tax percentages to projected income.

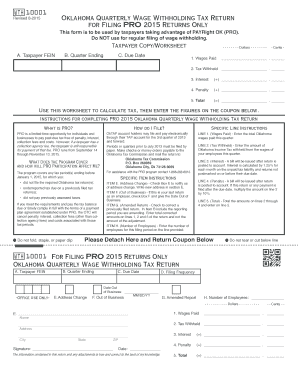

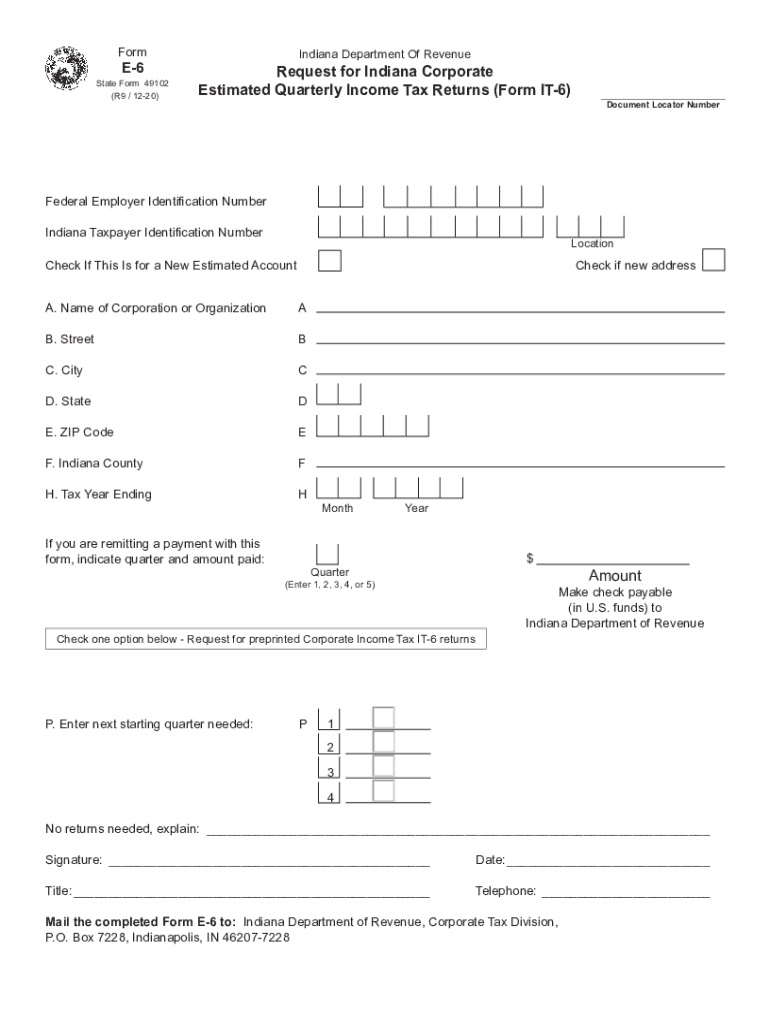

- Form Completion: Fill out the E-6 form or equivalent documents with computed figures.

- Submission and Payment: Use online, mailed, or in-person methods to submit forms and make payments.

Filing Tips

- Use accounting software to maintain organization and record accuracy.

- Stay informed on changes to state tax rates and filing procedures.

Filing Deadlines / Important Dates

Adhering to strict filing deadlines is crucial. Indiana requires estimated income forms to be submitted quarterly, usually on the 15th day of the fourth, sixth, ninth, and twelfth months of the tax year. Timely submission ensures that businesses avoid penalties.

Critical Dates

- April 15: First quarter deadline.

- June 15: Second quarter deadline.

- September 15: Third quarter deadline.

- December 15: Final quarter deadline.

Required Documents

To accurately complete the Indiana estimated income process, certain documents must be ready and available. These include previous tax returns, financial statements, and the Indiana Form E-6 for corporations.

Essential Documentation

- Tax Returns: Prior year federal and state returns to determine past obligations.

- Financial Statements: Current balance sheets, income statements, and cash flow analyses.

- E-6 Form: Specific to Indiana corporate estimated income tax reporting.

State-Specific Rules for the Indiana Estimated Income

Indiana has specific rules governing estimated income tax payments. Understanding these nuances is essential for compliance and optimizing tax strategies.

Compliance Guidelines

- Thresholds: Businesses that expect to owe less than a certain amount may not be required to make estimated payments.

- Exemptions and Deductions: Be aware of specific state deductions that may affect tax liabilities.

Penalties for Non-Compliance

Failing to comply with Indiana's estimated income tax requirements can result in significant penalties. Underpayments, late payments, or incorrect filings can all incur fines.

Potential Consequences

- Interest Charges: Accumulate on outstanding tax liabilities until payment is made.

- Fine Amounts: Calculated based on the amount and duration of underpayment.