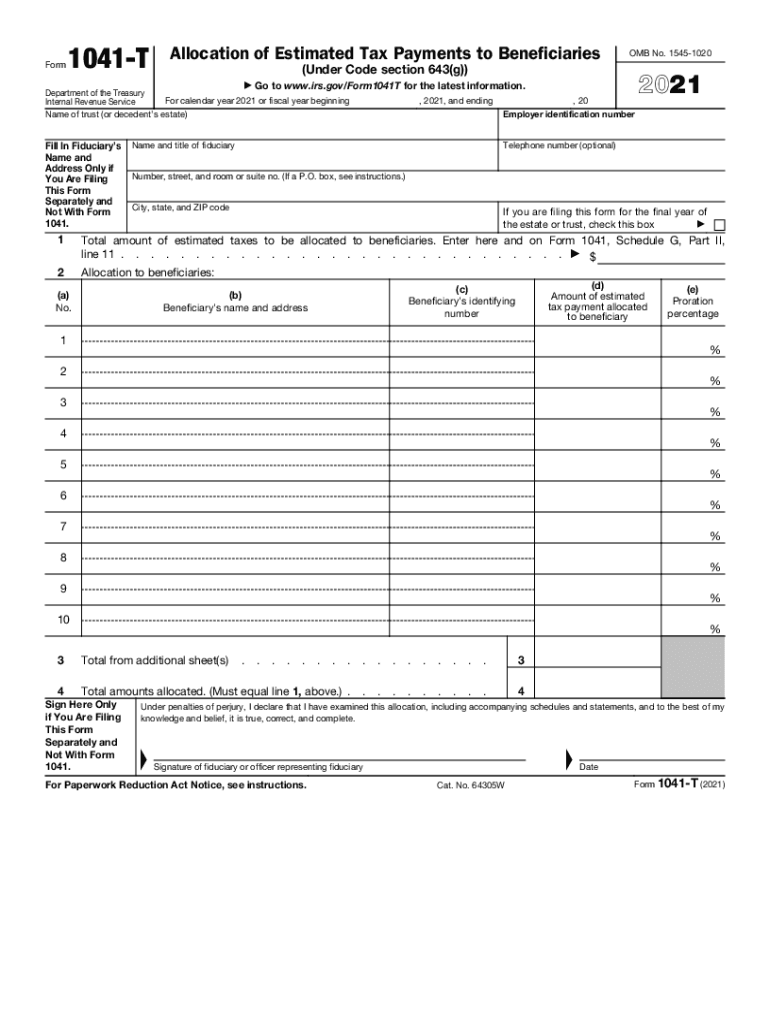

Definition and Purpose of the 1041-T Tax Form

Form 1041-T, titled "Allocation of Estimated Tax Payments to Beneficiaries," is used by trusts and decedent's estates to allocate estimated tax payments to beneficiaries according to section 643(g) of the Internal Revenue Code. This election is irrevocable and allows a fiduciary to treat a portion of the estimated tax paid by the estate or trust as if it were paid by the beneficiaries themselves. This can be crucial for accurate tax reporting and ensuring that beneficiaries receive the appropriate tax credits or refunds. The form facilitates the division of tax liabilities in a manner that reflects their respective shares as defined under trust or estate agreements.

How to Use the 1041-T Tax Form

Using Form 1041-T involves several specific steps to ensure accurate allocation of estimated tax payments. First, fiduciaries must determine the total amount of estimated taxes available for allocation. They then divide this amount among the beneficiaries based on the terms of the trust or estate or as required by law. It's essential to calculate each beneficiary’s share accurately, considering the legal or agreed-upon division of the asset’s income. After completing the form, ensure it is signed and dated by the fiduciary or authorized representative before submission. Beneficiaries can use their share of the allocated estimated taxes when filing their personal income tax returns.

Steps to Complete the 1041-T Tax Form

-

Gather Required Information: Collect the total estimated tax payments made by the trust or estate and detailed information for each beneficiary, including names, addresses, and taxpayer identification numbers.

-

Calculate Allocations: Determine how much of the estimated tax payments will be allocated to each beneficiary. This should be based on their respective share outlined in the trust or estate instrument.

-

Complete the Form: Fill out the top section with identifying information about the estate or trust. Then, enter the calculated allocations for each beneficiary under the relevant sections for their identification and allocation amounts.

-

Sign and Date the Form: Ensure that the fiduciary or authorized representative signs and dates the document to validate its authenticity.

-

Submit the Form: Prepare to submit the form according to IRS guidelines, typically with the estate or trust’s annual tax return by the prescribed deadline.

Filing Deadlines and Important Dates

The 1041-T should be filed by the 65th day following the close of the estate or trust’s tax year. Timely submission is critical, as late filing can result in penalties or cause issues with beneficiaries claiming their allocated portion of estimated taxes. Keep a record of this deadline to avoid any compliance issues. It is important for fiduciaries to be aware of and adhere to these filing requirements to maintain accuracy in tax reporting for both the estate or trust and its beneficiaries.

Obtaining the 1041-T Tax Form

Form 1041-T can be acquired directly from the IRS website as a downloadable PDF. Fiduciaries may also find the form through tax software solutions or by requesting a physical copy via mail from IRS services. Always ensure you're using the most up-to-date version of the form to avoid compliance issues and take advantage of any changes in tax law or form instructions that could affect allocations.

Important Terms Related to the 1041-T Tax Form

- Fiduciary: The appointed individual or institution responsible for managing the estate or trust as per the legal agreements.

- Beneficiary: Individuals or entities entitled to receive a portion of the trust’s or estate’s income or assets.

- Irrevocable Election: Once the fiduciary elects to allocate estimated taxes using the 1041-T, this choice cannot be undone.

Understanding these terms ensures proper handling and knowledge for preparing and filing the form.

Legal Use and Compliance for the 1041-T Tax Form

IRS regulations dictate that the use of Form 1041-T must be strictly for its intended purpose of allocating estimated tax payments to beneficiaries. The election made using this form must reflect the agreements under the trust or estate plan and is irreversible once filed. Fiduciaries must ensure compliance with IRS rules and maintain transparency in allocations to prevent any legal issues or disputes from arising. Legal counsel may be sought when needed to ensure appropriate handling of the form’s requirements.

Example Scenarios of Using the 1041-T Tax Form

Consider a trust that received $10,000 in estimated tax payments during the tax year. The trust agreement specifies that three beneficiaries—Beneficiary A, Beneficiary B, and Beneficiary C—are to receive 40%, 35%, and 25% of income, respectively. When using Form 1041-T, the fiduciary would allocate $4,000 to Beneficiary A, $3,500 to Beneficiary B, and $2,500 to Beneficiary C. Each beneficiary would then report these amounts on their personal tax returns, possibly reducing their individual tax liabilities through this allocation.

IRS Guidelines and Instructions for the 1041-T Tax Form

The IRS provides comprehensive instructions for completing Form 1041-T, covering areas such as accuracy in figures, it being mandatory to report taxpayer identification numbers (TINs) for all beneficiaries, and adhering to filing deadlines. Any discrepancies or omissions could lead to delays or compliance issues. Fiduciaries must familiarize themselves with the instructions to ensure complete and accurate filings.

Penalties for Non-Compliance with the 1041-T Tax Form

Failure to file Form 1041-T on time or incorrect allocation of tax payments can result in penalties imposed by the IRS. Non-compliance might result in the inability of beneficiaries to claim their portion of estimated taxes, inaccurately filed personal returns, or potential legal disputes. Thus, fiduciaries are advised to maintain accurate records, consult tax professionals if necessary, and adhere strictly to IRS guidelines to avoid these potential penalties.