Definition and Meaning

The Tax Form 1041-T, formally known as "Allocation of Estimated Tax Payments to Beneficiaries," is instrumental for fiduciaries managing trusts or decedent's estates. Its primary purpose is to allocate a portion of estimated tax payments to beneficiaries under section 643(g) of the Internal Revenue Code. It provides an avenue for fiduciaries to elect that a part of the tax payments be considered as payments made by the beneficiaries themselves. Understanding this form is crucial for fiduciaries who wish to manage tax implications effectively for both the estate and its beneficiaries.

Purpose and Usage

This form is used primarily by fiduciaries to ensure that beneficiaries receive credit for estimated tax payments applied towards their individual tax returns. Filing the 1041-T allows fiduciaries to manage the tax burdens more strategically, helping beneficiaries align with tax liabilities. By assigning estimated payments to beneficiaries, the fiduciary can better represent the estate's financial activities for tax reporting purposes. Such strategic allocations can optimize tax responsibilities and potentially benefit both the fiduciary and the beneficiaries.

Obtaining the Tax Form 1041-T

Acquiring the Tax Form 1041-T is straightforward. It can be downloaded directly from the IRS website. Alternatively, it may be available through tax software such as TurboTax or QuickBooks, which often includes the forms necessary for comprehensive tax preparation. Financial institutions or legal professionals specializing in estate planning might also provide this form to their clients. Ensuring the correct version is obtained can prevent misunderstandings during the submission phase.

Steps to Complete the Tax Form 1041-T

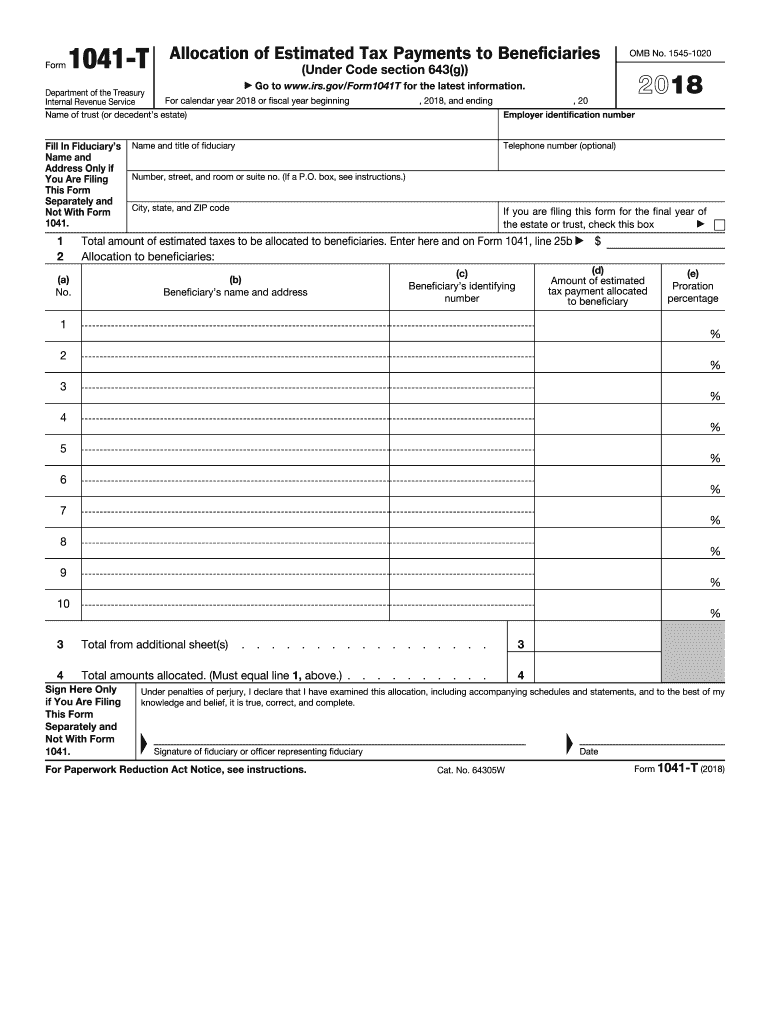

- Identify the Fiduciary: Include the estate or trust details along with the fiduciary's information.

- List Beneficiaries: Clearly list all beneficiaries, including their names and taxpayer identification numbers.

- Allocate Payments: Specify the amounts of estimated tax payments to be allocated to each beneficiary.

- Sign and Date the Form: The fiduciary must provide a signature and date to validate the allocations.

- Submit: Ensure submission by the 65th day following the close of the tax year. This filing deadline is critical as the election made is irrevocable.

Filing Deadlines and Important Dates

The crucial filing deadline for the Tax Form 1041-T is the 65th day after the end of the estate or trust’s tax year. This timeline is vital as missing this deadline can lead to complications, including a potential inability to allocate estimated payments to beneficiaries, which could result in higher tax liabilities. Compliance with this deadline ensures that elections made via the form are considered valid for the related tax year, preventing any disruption in beneficiary tax credit allocations.

Key Elements of the Tax Form 1041-T

- Fiduciary and Entity Information: Clear identification of the trust or estate and the responsible fiduciary.

- Beneficiary Details: Comprehensive list including beneficiaries’ identification numbers.

- Allocated Amounts: Specific amounts of allocated estimated tax payments must be precise and reflect the fiduciary's records.

- Irrevocability Clause: Once elected, the allocations on this form cannot be revised, emphasizing the importance of accuracy when completing the form.

Legal Use and Compliance

The form facilitates the legal transfer of tax payment credits from an estate to its beneficiaries and establishes a fiduciary responsibility to report accurately. The legal framework supporting this form under IRS guidelines demands that any allocation of estimated payments be executed with strict adherence to current tax laws. Fiduciaries must act within their legal capacity when utilizing Tax Form 1041-T, ensuring compliance to avoid penalties or legal ramifications.

Examples of Using the Tax Form 1041-T

A typical scenario might involve an estate with multiple beneficiaries, where the fiduciary opts to allocate estimated tax payments directly to those beneficiaries. For instance, in a trust distributing approximately $30,000 in estimated taxes among five beneficiaries, each receiving an equal share, this would translate to $6,000 in estimated payments per beneficiary. This strategic allocation aids beneficiaries in managing their personal tax liabilities efficiently.

By understanding these aspects of Tax Form 1041-T, fiduciaries can strategically allocate estimated tax payments, ensuring compliance and optimizing the tax benefits for the estate and its beneficiaries.