Definition and Purpose of IRS Form 5471 Instructions

IRS Form 5471 instructions provide detailed guidelines for U.S. taxpayers who must report information about their controlled foreign corporations (CFCs) to the IRS. The instructions accompany Form 5471, which is used to disclose ownership interests, income, earnings, profits, and other significant financial details of a CFC. The purpose of these instructions is to help taxpayers accurately complete the form, ensuring compliance with legal requirements and preventing potential penalties associated with incomplete or incorrect submissions.

Steps to Complete the IRS Form 5471

Completing IRS Form 5471 involves several critical steps to ensure accurate reporting.

-

Identify the Category of Filer: The instructions help determine the filer's specific reporting category based on ownership interests and control over the foreign corporation.

-

Gather Necessary Information: Collect all relevant financial statements and records, including incomes, earnings, and transfers within the foreign corporation.

-

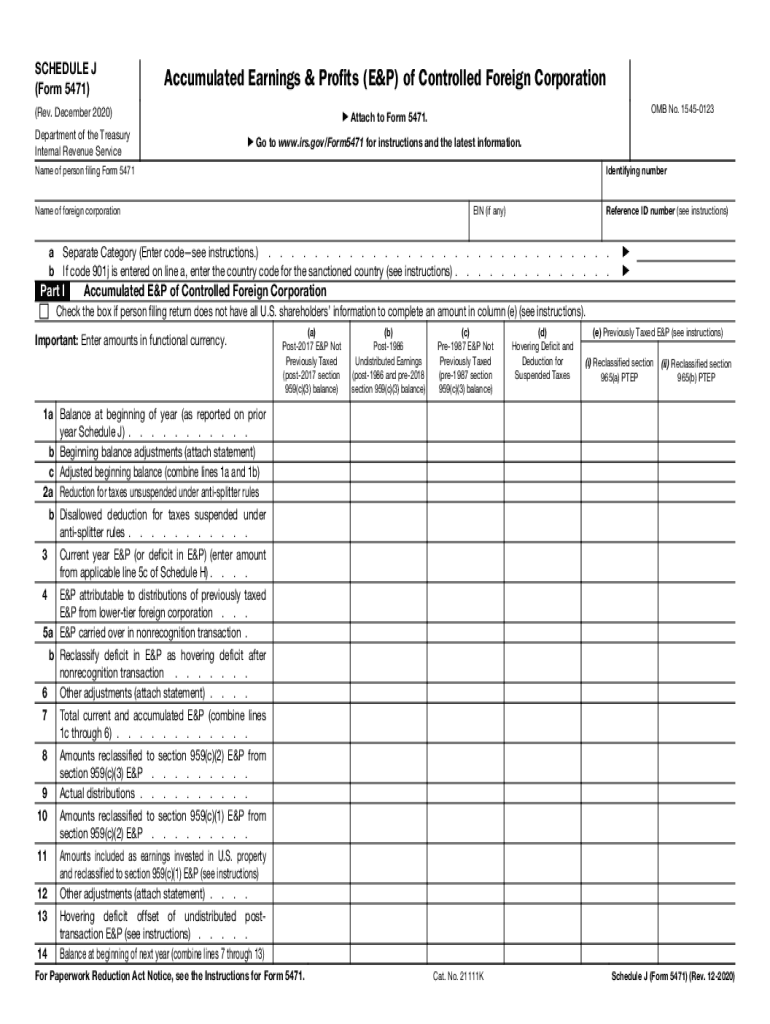

Complete the Required Schedules: Different categories of filers require various schedules, such as Schedule E for Income, Schedule J for Accumulated Earnings and Profits, and Schedule M for Transactions.

-

Verify Calculations: Ensure that all calculations and reported figures adhere to IRS guidelines to prevent discrepancies.

-

Review and Submit: Double-check completed forms against the IRS Form 5471 instructions before submission.

Who Typically Uses IRS Form 5471 Instructions

The IRS Form 5471 instructions are essential for U.S. citizens, resident aliens, and certain U.S. entities with ownership stakes in a CFC. They are often used by individuals and corporations that own at least ten percent of a foreign corporation. Tax practitioners, accountants, and tax attorneys also frequently consult these instructions to assist clients with compliance and to prepare accurate reports.

Important Terms Related to IRS Form 5471 Instructions

Understanding specific terms is crucial when engaging with IRS Form 5471 instructions:

- Controlled Foreign Corporation (CFC): A foreign corporation in which U.S. shareholders hold more than 50% of the stock by vote or value.

- Subpart F Income: Certain income of a CFC that is taxable to U.S. shareholders regardless of whether it is distributed.

- Foreign Tax Credit: A non-refundable credit for income taxes paid to a foreign government.

Filing Deadlines and Important Dates

IRS Form 5471 is typically due alongside the annual tax return, including extensions. For calendar year taxpayers, this would generally be April 15th. Extensions may allow filing until October 15th, but it's vital to confirm deadlines each tax year. Staying informed on these key dates can prevent penalties for late filing.

Penalties for Non-Compliance

Failing to file IRS Form 5471 correctly and timely can lead to severe penalties. Generally, the penalty starts at $10,000 per form for each year not filed. Additional penalties can accrue if underreporting or discrepancies are identified, emphasizing the critical need for accurate form completion and timely submission.

Legal Use of IRS Form 5471 Instructions

The instructions are a legal guideline for ensuring taxpayer compliance with U.S. international tax laws. They outline the responsibilities and obligations of U.S. persons with interests in CFCs, and adherence to these instructions helps prevent potential legal issues related to tax evasion or misreporting.

Key Elements of the IRS Form 5471 Instructions

Several components make the IRS Form 5471 instructions comprehensive:

- Eligibility Criteria: Clarifications on who must file based on foreign ownership and control.

- Detailed Schedule Descriptions: In-depth explanations for completing applicable schedules.

- Reporting Requirements: Specifics regarding income, deductions, and foreign corporation financial activities.

IRS Guidelines and Updates

The IRS frequently updates Form 5471 instructions to reflect changes in tax law or policy. Taxpayers must review the most recent version of the instructions annually to comply with any amendments. Staying current with these updates is fundamental to meeting U.S. reporting obligations accurately.

Examples of Using IRS Form 5471 Instructions

Consider a U.S. shareholder owning 15% of a CFC that generates significant profits abroad. By following Form 5471 instructions, the shareholder ensures accurate reporting of their share of Subpart F income and adjusts their U.S. tax return to reflect foreign earnings, illustrating the practical application in real-world scenarios.

Digital vs. Paper Version Availability

While IRS Form 5471 and its instructions are available in paper format, many taxpayers use digital versions for ease of completion and electronic submission. Online tax software often integrates these digital forms, allowing for direct data entry and, in some cases, e-filing options, enhancing efficiency and accuracy.