Definition and Meaning

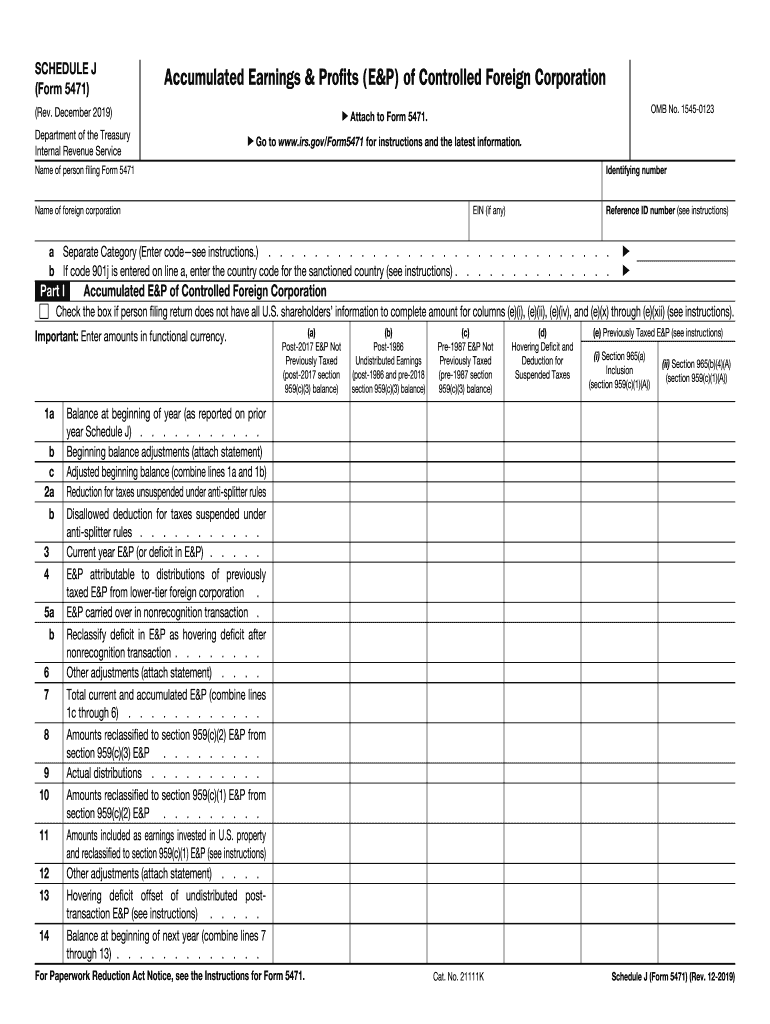

Form 5471, officially titled "Information Return of U.S. Persons With Respect to Certain Foreign Corporations," is a crucial document used by U.S. citizens and residents to report their interest in foreign corporations. This form aims to collect comprehensive data on foreign corporations in which U.S. persons hold a significant stake, thereby ensuring compliance with U.S. tax laws related to foreign income. The form helps the Internal Revenue Service (IRS) gain insight into the operations, financials, and earnings of these foreign corporations.

Who Typically Uses Form 5471

This form is generally used by U.S. citizens, resident aliens, and certain foreign individuals who are considered U.S. persons under tax law. Specifically, it is applicable to U.S. persons who are officers, directors, or shareholders in certain foreign corporations where the person owns 10% or more of the total combined voting power or market value in the foreign corporation. Business entities, such as partnerships and corporations, may also need to file this form if they meet the ownership threshold.

Key Elements of Form 5471

- Income Statement and Balance Sheet: Ensures a detailed report of the foreign corporation's financial activities.

- Shareholder Information: Identifies U.S. persons who have a certain level of ownership in the foreign entity.

- Earnings and Profits Calculation: Captures the earnings and profits of the foreign corporation for tax purposes.

- Transactions with Shareholders: Details any financial interactions between the corporation and its U.S. shareholders.

Important Terms Related to Form 5471

- Control: Refers to ownership of more than 50% of the voting power or value of the foreign corporation.

- CFC (Controlled Foreign Corporation): A U.S. person holds more than 50% of the control.

- Subpart F Income: Types of income that must be reported by U.S. shareholders even if not distributed.

- GILTI (Global Intangible Low-Taxed Income): Income component taxed under U.S. regulations to curb tax avoidance.

Steps to Complete Form 5471

- Gather Required Financial Information: Collect financial statements and shareholder details.

- Calculate Earnings and Profits: Determine the corporation’s accumulated earnings for tax purposes.

- Complete the Income and Balance Sheet Sections: Enter financial data in the designated sections.

- Report Shareholder Information: Fill in details for U.S. shareholders meeting the ownership requirements.

- Review for Accuracy: Double-check all calculations and entries to ensure compliance.

- Submit the Form: File with your U.S. federal tax return, using the same due date.

Filing Deadlines and Important Dates

Form 5471 aligns with the filing deadline for individual tax returns, typically April 15 for calendar-year filers, providing an extension to October 15 when necessary. It's crucial to adhere to these deadlines to avoid penalties. Corporations may have different deadlines depending on their fiscal year.

Penalties for Non-Compliance

Failure to file Form 5471 or incorrect filings can result in significant penalties. The IRS imposes a penalty of $10,000 for each form not filed, with additional penalties accruing for extended delinquency. Moreover, certain larger penalties may be applied based on the severity of non-compliance, particularly if the IRS deems the oversight as intentional evasion.

IRS Guidelines

The IRS provides comprehensive instructions for Form 5471, detailing each section and its requirements. Understanding these guidelines is essential as they explain the subtleties associated with various filing categories, such as categories of filers, types of ownership structures, and special reporting instances. Reading the IRS instructions thoroughly can prevent errors and omissions.

Examples of Using Form 5471

Consider a scenario where a U.S. citizen owns 15% of a Canadian company. The citizen must report their ownership stake and any income derived from this investment on Form 5471. Similarly, companies like partnerships or LLCs with foreign subsidiaries must also comply by detailing their foreign interests. Each instance tailors the form's requirements to reflect specific ownership and income scenarios.