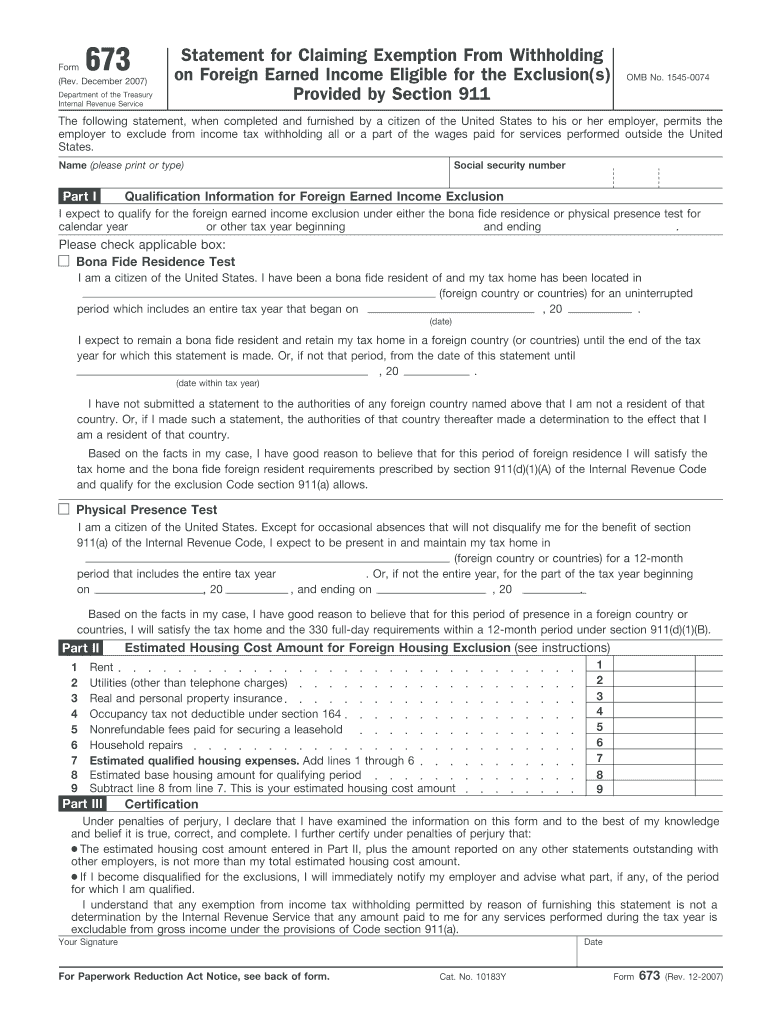

Definition and Purpose of Form 673

Form 673 is a critical document provided by the Internal Revenue Service (IRS) that allows U.S. citizens working abroad to claim an exemption from income tax withholding on foreign-earned income. This form plays an essential role for those who qualify for the foreign earned income exclusion, offering a clear avenue to manage their tax obligations effectively. Key components of Form 673 include personal information sections, qualification details, estimated housing costs, and a certification statement that the taxpayer must complete.

The primary goal of Form 673 is to ensure that U.S. citizens living overseas can leverage the tax benefits afforded under Section 911 of the IRS code. By filing this form with their employer, expatriates can have their tax withholding adjusted, aligning them more closely with their financial realities and legal entitlements.

Steps to Complete Form 673

Filling out Form 673 involves several detailed steps to ensure accuracy and compliance with IRS regulations.

-

Gather Required Information: Before starting, collect personal details such as name, address, social security number, and employment details. It's also important to have information on foreign residency and income.

-

Enter Personal Details: Begin by filling in your personal information, including your full legal name, U.S. address, and social security number.

-

Qualification for Exclusion: Declare your eligibility for the foreign earned income exclusion. This includes stating your intention to meet either the bona fide residence test or physical presence test.

-

Estimate Housing Costs: If applicable, provide an estimate of your foreign housing costs. This is particularly relevant for individuals seeking the foreign housing cost exclusion.

-

Certify Accuracy: Complete the form by certifying that the information provided is accurate to the best of your knowledge.

-

Submit to Employer: Once completed, submit the form to your employer. This action informs them of your status and facilitates appropriate adjustments to your income tax withholding.

How to Obtain Form 673

There are several methods for acquiring Form 673 to ensure easy access for all eligible U.S. citizens working abroad.

-

Online Download: The most straightforward method is to download the form directly from the IRS website. This ensures that you have the most up-to-date version available.

-

Employer Request: Many employers provide this form directly to employees working overseas, streamlining the process between expatriate employees and the HR or accounting department.

-

Tax Professional Services: Another option is to consult with a tax professional who can provide the form as part of their tax planning services.

By accessing Form 673 through these channels, you can ensure prompt and proper submission, aiding in the management of tax liabilities associated with foreign income.

Who Typically Uses Form 673

Form 673 is predominantly used by U.S. citizens who earn income abroad and wish to manage this income with respect to U.S. tax obligations.

-

Expatriate Employees: Many expatriates employed by multinational companies or international organizations benefit from filing Form 673, as it allows for adjusted withholding on foreign income.

-

Self-Employed Individuals: Although less common, self-employed U.S. citizens living overseas may also utilize this form to coordinate with any stateside entities regarding tax responsibilities.

-

Military Personnel: U.S. military members stationed abroad may also find filling out Form 673 valuable due to eligibility for certain exclusions.

Key Elements of Form 673

Understanding the core components of Form 673 is fundamental to accurately completing and filing the document.

-

Personal Identification Section: This includes full legal name, U.S. address, and social security number. Accurate entry of these details is crucial to avoid processing issues.

-

Exclusion Eligibility Declaration: This section requires the taxpayer to declare eligibility for the foreign earned income exclusion, including residency status and duration.

-

Estimated Foreign Housing Costs: For those eligible, this segment captures estimated foreign housing expenses to utilize the housing exclusion provision successfully.

-

Certification Statement: This part of the form requires a signature, indicating agreement with the provided information's truthfulness and completeness.

IRS Guidelines for Form 673

Comprehensive understanding of IRS guidelines concerning Form 673 ensures compliance and maximizes the potential benefits from the foreign earned income exclusion.

-

Exclusion eligibility under Section 911 must be clearly articulated, with taxpayers choosing between the bona fide residence test or the physical presence test.

-

Documentation Submission: It's important to follow guidelines for submitting the form to an employer for withholding adjustments rather than directly to the IRS.

-

Timing Considerations: Ensure timely submission aligned with IRS guidelines to mitigate potential impacts on withholdings for the current tax year.

Adherence to IRS guidelines ensures the proper execution of Form 673, preventing misunderstandings or potential penalties.

Penalties for Non-Compliance

Understanding the repercussions of not adhering to Form 673 protocols is essential for any U.S. citizen working abroad.

-

Increased Tax Liabilities: Failure to submit Form 673 might result in incorrect withholding, leading to larger tax liabilities at year-end.

-

Possible Penalties: Non-compliance can also attract penalties or interest charges on taxes that should have been withheld and paid.

Ensuring compliance with Form 673 requirements lowers the risk of financial penalties and supports effective tax planning.

Eligibility Criteria for Form 673

Before filling out the form, it's crucial to ascertain eligibility based on U.S. tax law.

-

U.S. Citizenship: Only U.S. citizens who meet this criterion can utilize the form.

-

Foreign Earned Income: You must have qualifying foreign earned income to be eligible for the related exclusion under Section 911.

-

Residency or Physical Presence Test: Eligibility is contingent upon meeting the conditions of either the bona fide residence test or the physical presence test.

-

Foregoing Foreign Tax Credit: Taxpayers cannot claim both the foreign earned income exclusion and the foreign tax credit on the same income.

Meeting these criteria allows U.S. citizens to leverage Form 673 effectively and manage their tax status while living abroad.