Definition & Purpose

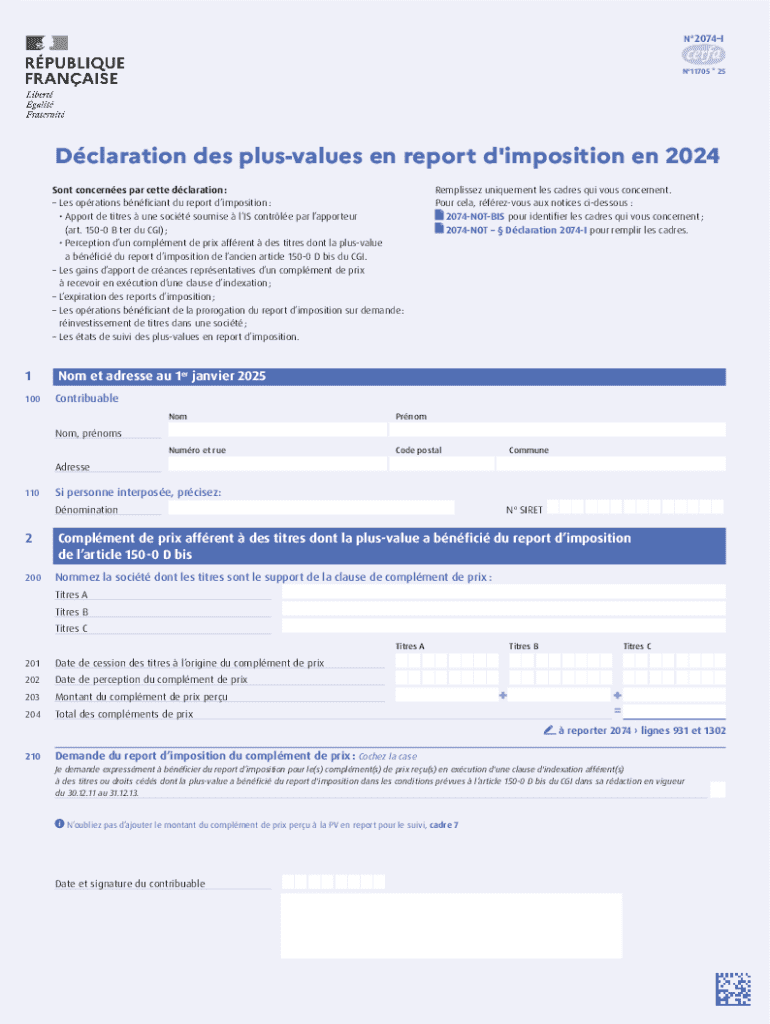

The French Tax Form 2074-I, also known by the shorthand "2074-I," is specifically designed for reporting capital gains that are deferred in taxation. This form is crucial for taxpayers involved in transactions that benefit from deferred tax reporting, such as the transfer of securities to a company subject to corporate tax. It allows for transparent declaration of deferred capital gains, ensuring compliance with French tax regulations.

- Deferred Taxation Transactions: These include operations like the transfer of securities to a company when the taxation of the capital gains can be postponed.

- Importance for Compliance: Using this form is essential to comply with French tax laws regarding capital gains, which facilitates tax deferment opportunities legally.

Steps to Complete the French Tax Form 2074-I

Filling out the French Tax Form 2074-I requires attention to detail and a step-by-step approach to ensure accuracy and compliance.

- Gather Necessary Information: Begin by compiling details regarding the securities transferred, including acquisition dates, original purchase prices, and market values at the time of transfer.

- Enter Personal Information: Input your personal details, such as name, address, and tax identification number.

- Provide Transaction Details: For each deferred gain, specify the relevant security's description, the involved parties in the transaction, and the date of transfer.

- Calculate Deferred Gains: Ensure precise calculations of deferred capital gains by subtracting the acquisition costs from the market value at the time of transfer.

- Complete Signature Section: After verifying all entries, sign and date the form to confirm the accuracy of the information provided.

Essential Calculations

- Cost Basis Determination: Calculate the cost basis of each security involved to ensure accurate reporting of gains.

- Gain or Loss Assessment: Determine the deferred gain or loss using market valuations.

Important Terms Related to French Tax Form 2074-I

Understanding key terms is critical for accurately completing the French Tax Form 2074-I.

- Deferred Capital Gains: These are gains on securities that are not taxed immediately upon realization but deferred to a future date.

- Security Transfer: Refers to the act of transferring ownership of financial instruments like stocks or bonds to another entity.

- Corporate Tax: A tax imposed on the net income of a company, integral when securities are transferred to companies.

Steps to Obtain the French Tax Form 2074-I

Acquiring the French Tax Form 2074-I can be done through various channels.

- France’s Official Tax Website: The form can be downloaded directly from the French Ministry of Finance’s website, ensuring you have the most updated version.

- Tax Professionals: Accountants and tax advisors can provide the form and usually help with its completion.

- Local Tax Offices: Physical copies may be available at local tax offices in France.

Digital Access

With technological advancements, this form can be accessed online, which improves convenience for taxpayers who prefer electronic submissions.

Filing Deadlines and Important Dates

Adhering to deadlines is crucial when handling deferred gains.

- Standard Filing Date: Generally aligns with the annual income tax return due date in France.

- Amendment Period: Corrections to filed forms should be made within specified periods following the initial submission.

Tax Year Considerations

Understanding when and for which fiscal year the tax applies is critical in maintaining compliance.

Legal Use of the French Tax Form 2074-I

The legal framework surrounding the 2074-I dictates its proper use and filing requirements.

- Compliance with French Tax Law: Utilizing the form ensures taxpayers are following national regulations on deferred taxation.

- Eligibility for Deferred Gains: Only transactions meeting specific criteria set by French law are eligible for deferment.

Legal Consequences

Failing to adhere to the legal uses of this form can result in penalties or additional taxes, emphasizing the importance of compliant use.

Who Typically Uses the French Tax Form 2074-I

The French Tax Form 2074-I is commonly used by individuals and entities involved in specific financial transactions.

- Foreign Investors: Non-residents involved in significant transactions in France may need to report using this form.

- Corporate Entities: Companies benefiting from deferred capital gains through specific securities transactions are frequent users.

Individual vs. Corporate Use

While both may use the form, the details and sections applicable can vary based on the nature of the taxpayer.

Required Documents

Documentation is crucial to substantiate claims and figures reported on the 2074-I.

- Transaction Receipts: Proof of original transactions and any subsequent sales are necessary.

- Securities Evidence: Records detailing the nature and value of the securities at the time of transfer or sale.

- Professional Valuations: Certified appraisals that ensure accurate market valuations at necessary reporting dates.

Having all required documents ready before filling out the form ensures a smoother and more efficient filing process.

Examples of Using the French Tax Form 2074-I

Exploring scenarios in which the French Tax Form 2074-I is used can clarify its application.

Common Scenarios

- Cross-Border Securities Transfer: Investors or corporations involved in transferring securities across borders for corporate restructuring, requiring deferred gains calculation.

- Realization of Stock Options: Executives or employees who transfer stock options into equity positions that benefit from deferred taxation.

Each scenario underscores the form's role in accurately reporting deferred capital gains and ensuring alignment with tax regulations.