Definition & Meaning of NY State Tax Not Applicable for Canadian Tax Credit

The term "NY State Tax not applicable for Canadian Tax Credit" refers to the specific conditions under which New York State taxes do not impact the eligibility or amount for claiming a Canadian tax credit. This involves understanding the nuances of how taxes paid to a province in Canada might influence a resident tax credit on a New York State tax return. It’s particularly relevant for U.S. residents who have financial dealings or income sources in Canada and wish to ensure compliance with tax regulations in both jurisdictions.

Key Elements of the Credit Application

- Eligibility Criteria: Individuals eligible to claim this credit typically have cross-border income transactions. The primary requirement is proof of taxes paid to a Canadian province.

- Applicable Tax Law: Section 620 of the New York Tax Law outlines the procedures and conditions for claiming resident credits due to taxes paid to a Canadian province.

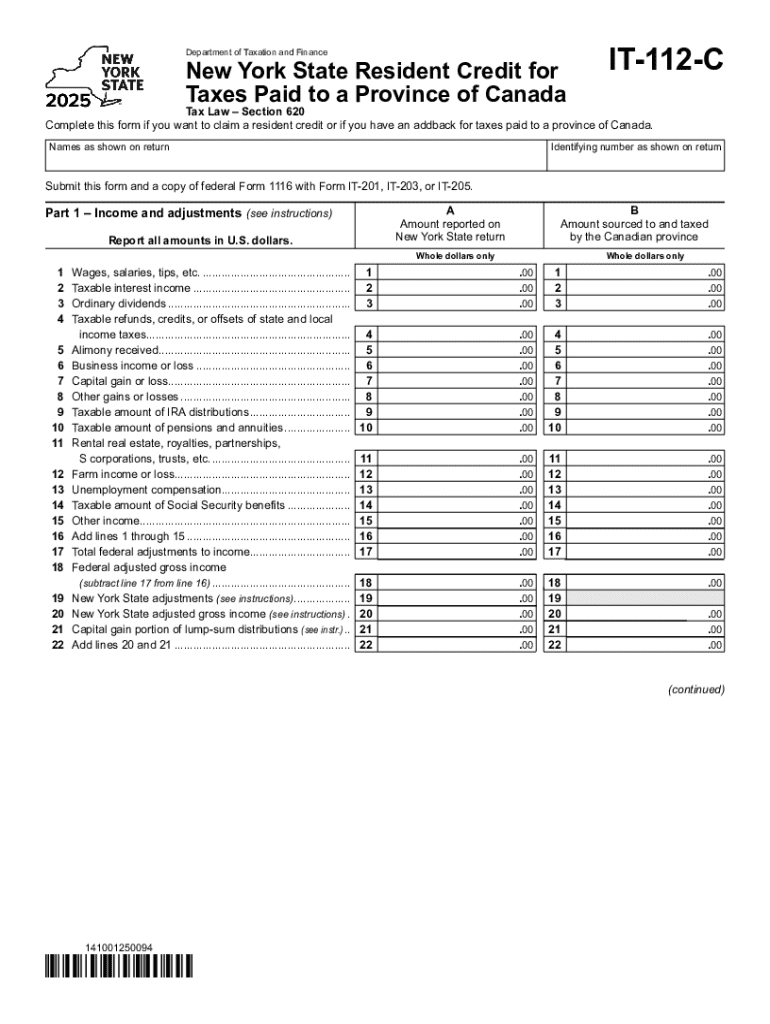

- Supported Documents: Taxpayers should prepare documents like IT-112-C to support their claim.

How to Use the NY State Tax Not Applicable for Canadian Tax Credit

To leverage the NY State Tax exemption in claiming a Canadian Tax Credit, taxpayers need to communicate their cross-border taxation details accurately. Here's how to do so:

- Assessment of Tax Paid to Canada: Determine the taxes paid to a Canadian province which you've already reported to the Canadian government.

- Filing the Correct Forms: Complete Form IT-112-C to reflect these Canadian taxes and illustrate why NY State Tax should not apply.

- Cross-Border Income Reporting: Ensure all income eligible for such claims is declared in both NY State and Canadian tax filings.

Step-by-Step Filing Instructions

- Document Collection: Gather all relevant tax documents from Canada, such as notices of assessment.

- Form Completion: Fill out Form IT-112-C, ensuring every entry aligns with your Canadian tax records.

- Review Cross-Jurisdiction Tax Treaty Benefits: Double-check any applicable tax treaties or agreements between the U.S. and Canada.

Steps to Complete the NY State Tax Not Applicable for Canadian Tax Credit

Completing the process involves several key steps that ensure full compliance and benefit optimization:

- Tax Identification: Begin by formally identifying all income sources and associated taxes paid to any Canadian jurisdiction.

- Documentation: Collect and verify each relevant document. This includes tax returns and any tax settlement documents from Canada.

- Form Submission: Submit Form IT-112-C alongside your New York State tax return.

- Verification and Audit Prep: Keep all records and documents ready for potential audits or requests for further information.

Potential Challenges and Solutions

- Misreporting Risks: Be cautious of currency conversion errors when reporting Canadian amounts in USD.

- Missing Supporting Documents: Contact Canadian tax authorities immediately if any forms are missing.

Important Terms Related to NY State Tax Not Applicable for Canadian Tax Credit

Understanding specific terminologies is crucial for accurately completing the tax credit process. Here are important terms:

- Resident Credit: A credit given to New York residents for taxes paid to other jurisdictions, including foreign countries.

- Tax Treaty: Bilateral arrangements between the U.S. and Canada to minimize dual taxation.

- IT-112-C Form: The designated form used by New York residents to claim credits against Canadian taxes paid.

IRS Guidelines

While primarily a state issue, understanding IRS perspectives on foreign tax credits is essential:

- Double Taxation Avoidance: IRS acknowledges claims for foreign taxes paid but requires proper documentation and the use of correct schedules.

- Foreign Tax Credit Forms: Utilize IRS Form 1116, though this operates differently from state credits.

State-Specific Rules for the NY State Tax Not Applicable for Canadian Tax Credit

State-specific rules dictate how and when this credit can be applied:

- New York-Specific Policies: Apply only if you're a resident of New York State with peer income taxation claims in Canada.

- Province-Specific Agreements: Be aware of any unique agreements New York might have with specific Canadian provinces.

Navigating State-by-State Differences

- Local Tax Law Understanding: For other states, investigate if similar credits or exemptions are available.

- Regional Tax Cooperation: Explore how states potentially collaborate with provinces to facilitate smoother cross-border taxation processes.

Penalties for Non-Compliance

Failure to accurately follow through with NY State Tax credit applications linked to Canadian credits can lead to:

- Fines and Penalties: Monetary penalties for filing inaccurate claims.

- Audit Risks: Increased likelihood of audits and deeper investigations by New York State tax authorities.

- Repayment Demands: State tax authorities may require repayment of improperly claimed credits, potentially with interest.

Best Practices to Avoid Penalties

- Thorough Review: Regularly audit your documentation and tax filing processes.

- Professional Consultation: Consult with a tax professional familiar with cross-jurisdictional tax regulations.

Filing Deadlines and Important Dates

Stay informed about critical deadlines to ensure timely submission:

- Annual State Tax Return Deadline: Typically aligns with federal deadlines, unless extensions are granted.

- Form IT-112-C Submission: Should coincide with your NY State Tax return to ensure credits are processed simultaneously.

Implications of Missing Deadlines

- Loss of Credits: Missing a deadline might delay the application of credits, impacting cash flow.

- Late Filing Penalties: Fines for late filings that escalate rapidly.

Form Submission Methods

There are various methods to submit the necessary forms for claiming the credit:

Online vs. Manual Submission

- Online Filing: Expedites the processing of your claims and is more efficient for keeping digital records.

- Mail Submission: Still an option but time-consuming and less reliable in terms of immediate feedback and processing times.

Digital Methods and Verification

- E-Filing Platforms: Utilize secure platforms to submit electronically and receive immediate confirmation of submission.

- Document Verification: Ensure all components of your claim are digitally verified by a professional to prevent errors during submission.