Definition and Purpose of Form IT-112

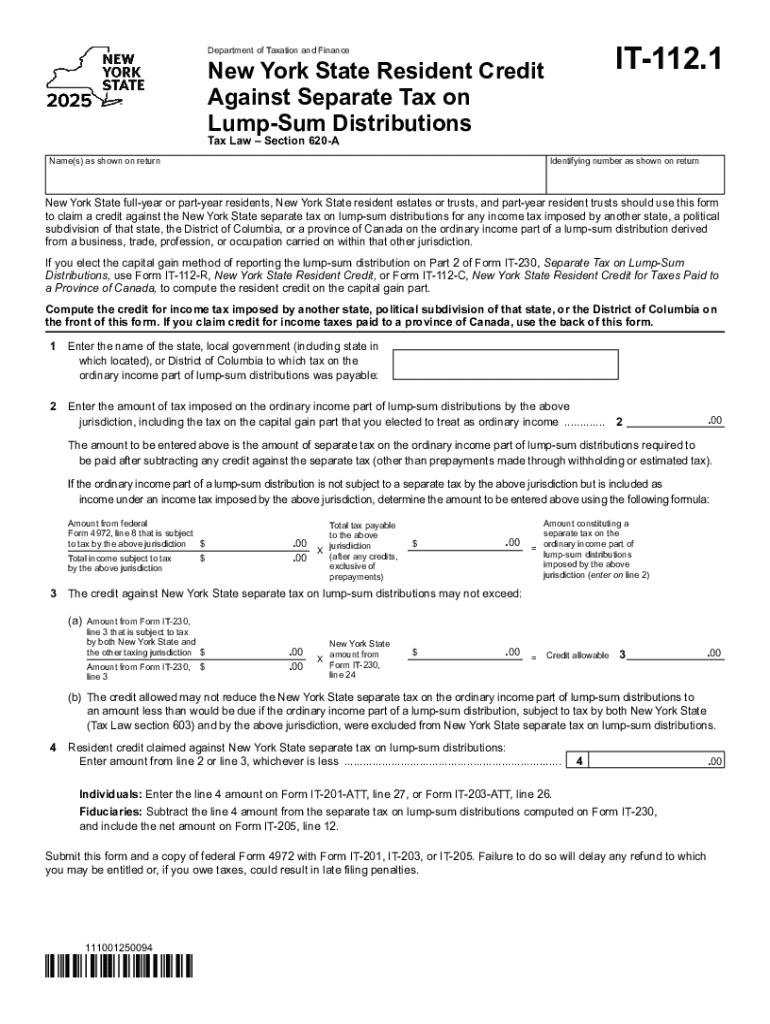

Form IT-112, also known as the New York State Resident Credit Against Separate Tax on Lump-Sum Distributions, is designed to provide tax credits to residents who have paid taxes on lump-sum distributions in other jurisdictions. This form serves to prevent double taxation for New York State residents by allowing them to claim a credit against their New York State taxes for taxes paid to another state on specific retirement distributions.

Key Features of Form IT-112

- Applicable to residents of New York State who pay taxes on lump-sum distributions in other states.

- Targets distributions from retirement accounts or pension plans.

- Provides a mechanism to claim a credit and reduce the tax liability in New York.

Eligibility Criteria for Claiming the Credit

To utilize Form IT-112, taxpayers must meet certain eligibility requirements which ensure that they rightfully claim the credit against their New York State taxes.

Eligibility Requirements

- Must be a resident of New York State.

- Should have received lump-sum distributions subject to taxation in another state.

- Must have paid taxes on these distributions to the other state.

Common Scenarios

- Retired individuals receiving distributions from out-of-state pension plans.

- Individuals who have relocated to New York but had contributions taxed elsewhere.

Steps to Complete Form IT-112

Completing Form IT-112 involves several systematic steps that facilitate accurate reporting and credit claims.

-

Gather Relevant Information

- Organize documentation for lump-sum distributions.

- Acquire tax statements from the out-of-state jurisdiction.

-

Calculate Eligible Credit

- Determine taxes paid to the other state on these distributions.

- Assess the limit of credits as allowed by New York State tax laws.

-

Fill Out the Form Accurately

- Enter names and identifying numbers as shown on previously submitted returns.

- Carefully complete each section based on gathered information.

-

Review and Submit

- Double-check calculations and ensure all form fields are filled.

- Submit through designated channels (mail or electronic submission).

Important Terms Related to Form IT-112

Understanding the terminology associated with Form IT-112 enhances comprehension and ensures correct usage.

- Lump-Sum Distribution: A one-time payout from a retirement or pension account.

- Resident Credit: A tax credit provided to residents to offset taxes paid to other states.

- Double Taxation: Paying taxes on the same income in more than one jurisdiction.

Legal Use and Compliance

Ensuring legal compliance when submitting Form IT-112 is crucial for avoiding penalties and securing eligible tax benefits.

Legal Considerations

- Accurately report all pertinent financial data.

- Maintain transparency regarding out-of-state tax payments.

Consequences of Non-Compliance

- Possible denial of credit claims.

- Penalties or additional interest on incorrectly reported taxes.

Methods to Obtain Form IT-112

Accessing the Form IT-112 is a straightforward process, with multiple channels available for convenience according to taxpayer preference.

Available Methods

- Online Access: Direct download from the New York State Department of Taxation and Finance website.

- Physical Copies: Request via mail or obtain from local tax offices.

Benefits of Different Methods

- Digital Download: Quick access; environmentally friendly.

- Paper Forms: Suitable for those less comfortable with digital formats.

State-Specific Rules for New York Residents

New York State residents must adhere to specific regulations when claiming credits through Form IT-112.

State Regulations

- Credits must only be claimed for taxes paid on distributions recognized by New York State.

- Each credit claim should align with state thresholds and income brackets.

Notable Exceptions

- Certain municipal or county taxes may not qualify for credit.

- Income types distinct from lump-sum distributions might require separate forms.

Filing Deadlines and Important Dates

Taxpayers must be mindful of deadlines associated with submitting Form IT-112 to ensure timely processing and acceptance of their claims.

Key Deadlines

- Submit alongside state tax returns, typically due April 15th.

- Extensions might apply under specific conditions, subject to approval.

Impact of Missing Deadlines

- Delays in refunds or credits.

- Potential fines and interest on underpaid tax liabilities.