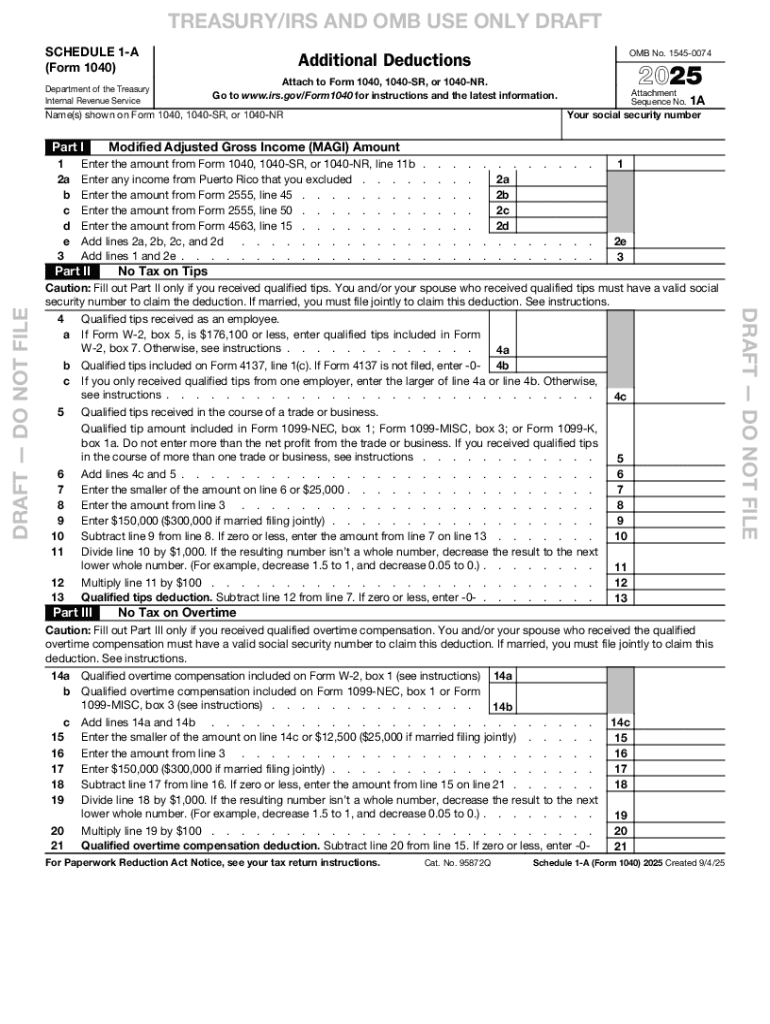

Definition and Meaning of Schedule 1-A (Form 1040)

Schedule 1-A (Form 1040) is a supplemental form issued by the Internal Revenue Service (IRS). It accompanies the standard Form 1040, 1040-SR, or 1040-NR to report additional income and adjustments to income that may not be included directly on the main tax return form. The form allows for the declaration of various types of income, such as capital gains, unemployment compensation, and other sources not captured on the main form, as well as deductions like student loan interest and educator expenses.

How to Use Schedule 1-A (Form 1040)

To effectively use Schedule 1-A, taxpayers must first determine if they have any income or adjustments that need to be reported. This form is relevant for those receiving income from unusual sources or claiming specific deductions. It involves listing the income types and amounts in designated sections. Care must be taken to ensure all figures correspond to the relevant categories and are transferred accurately to the main 1040 form. Detailed instructions on using this form are available from the IRS, ensuring compliance and accuracy.

Steps to Complete Schedule 1-A (Form 1040)

- Gather Necessary Documents: Collect all relevant documentation, such as W-2s, 1099s, and proof of deductions.

- Identify Additional Income: Determine all sources of additional income that must be reported.

- Record Adjustments: List all applicable adjustments to income, including education deductions and others.

- Follow IRS Instructions: Use the IRS-provided guidelines to accurately fill out each section.

- Transfer Totals: Carefully record figures onto Form 1040 in the designated areas.

- Review and Submit: Ensure all information is accurate and complete before submitting.

Why Use Schedule 1-A (Form 1040)

Schedule 1-A is crucial for taxpayers with complex financial situations, providing a mechanism to report diverse income streams and deductions. Using this form ensures compliance with tax laws, potentially reducing taxable income through eligible deductions, and helps avoid underreporting, which could lead to penalties.

Who Typically Uses Schedule 1-A (Form 1040)

The form is commonly used by taxpayers with multiple income sources, such as self-employed individuals, investors, or those who receive unemployment compensation. It is also relevant for students and educators seeking specific deductions, retirees with pension income, or any taxpayer who needs to report additional income or adjustments not available on the main 1040 form.

Important Terms Related to Schedule 1-A (Form 1040)

- Additional Income: Includes sources such as rental income, alimony, and prizes.

- Adjustments to Income: Encompasses deductions like IRA contributions and health savings account contributions.

- Taxpayer: The individual or entity completing and filing the form.

- IRS: The U.S. government agency responsible for tax collection and tax law enforcement.

IRS Guidelines for Schedule 1-A (Form 1040)

The IRS provides detailed guidelines to assist taxpayers in accurately completing Schedule 1-A. These guidelines outline eligible income and deductions, provide examples of classifications, and offer step-by-step instructions. Adhering to these guidelines ensures compliance and reduces errors.

Filing Deadlines and Important Dates

Schedule 1-A must be submitted alongside the standard Form 1040 by the federal tax deadline, typically April 15. Taxpayers should be attentive to variations due to weekends or holidays and consider applying for extensions if necessary.

Form Submission Methods

Schedule 1-A can be submitted electronically using tax software or through the IRS's e-File system, which is recommended for its efficiency and error reduction. Alternatively, taxpayers can print and mail the completed form to the IRS address specified for their location.

Penalties for Non-Compliance

Failure to file Schedule 1-A, when required, can lead to penalties, interest on unpaid taxes, and potential audits. Accurate and timely submission prevents these consequences and ensures that all income and credits are properly reported.