Definition & Meaning

Form 1099-A, officially known as "Acquisition or Abandonment of Secured Property," is a tax document used primarily in the United States. It provides critical information to both the Internal Revenue Service (IRS) and taxpayers regarding the acquisition or abandonment of property that was used to secure a loan. This form must be filed by lenders when a borrower fails to meet the obligations of the secured loan, leading to either the acquisition or abandonment of the secured property.

How to Use the Form 1099-A

Lenders use Form 1099-A to report to the IRS and the borrower the details of the transaction involving secured property. Borrowers might use this form to determine if they have realized gains or losses due to the transaction. This form includes necessary details like the date of acquisition or abandonment, the outstanding loan balance, and the fair market value of the property. This data contributes to determining the taxable income for the borrower if any deficiencies occur during the transaction.

Who Typically Uses the Form 1099-A

Form 1099-A is typically used by lenders, which can include financial institutions and individuals who have lent money using secured property as collateral. Borrowers, on their part, will receive this form when their lender forecloses and repossesses the secured property or when they abandon the property. Understanding who utilizes this form is crucial for ensuring both parties fulfill their tax-reporting obligations accurately.

Key Elements of the Form 1099-A

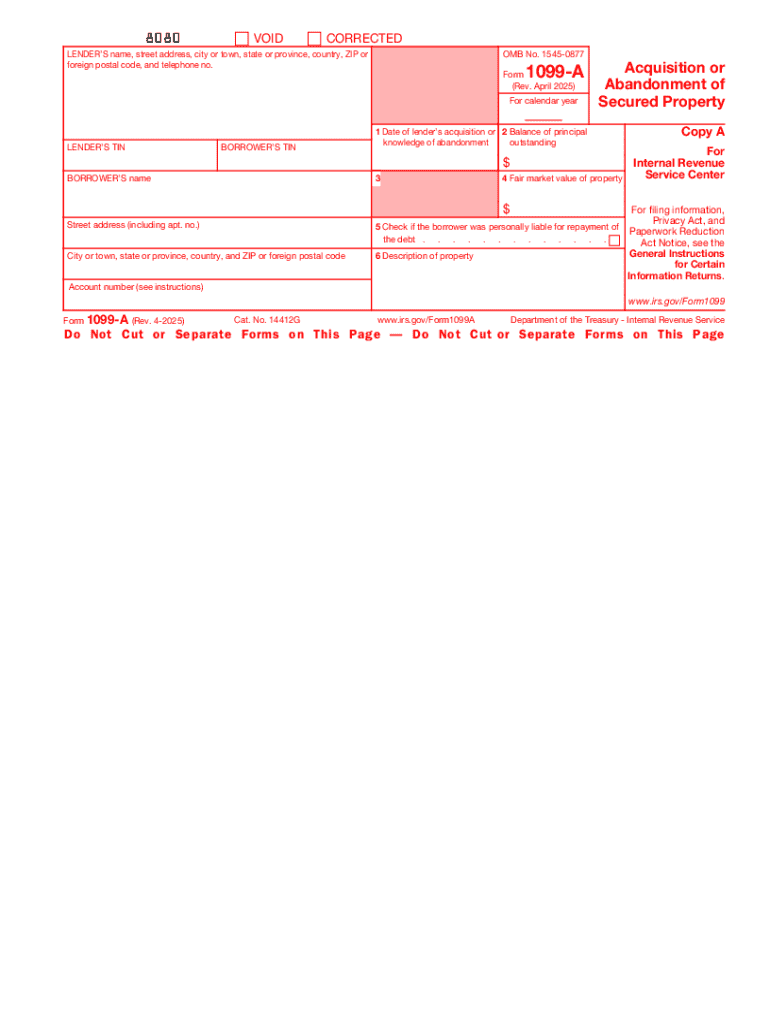

- Lender's Information: Includes the lender's name, address, and taxpayer identification number.

- Borrower's Information: Contains the borrower's name and taxpayer identification number.

- Balance of Principal: The remaining balance on the loan at the time of the acquisition or abandonment.

- Fair Market Value (FMV): Reflects the FMV of the property at the time of acquisition or abandonment.

- Acquisition/Abandonment Date: The specific date when the property transaction was completed.

These key components are essential for filling out the form accurately and ensuring compliance with IRS regulations.

Steps to Complete the Form 1099-A

- Gather Necessary Information: Collect all relevant details about the borrower, lender, and property.

- Enter Borrower and Lender Details: Fill out the sections with the borrower and lender's information.

- Fill in Loan Details: Include the fair market value of the property and the outstanding balance on the loan.

- Provide Transaction Dates: Accurately note the date of acquisition or abandonment.

- Double-Check Data: Review all entered information for accuracy to avoid any potential issues with the IRS.

Legal Use of the Form 1099-A

The Form 1099-A serves as a legal document that informs all parties involved of a significant financial transaction regarding secured property. This form must be completed accurately to ensure compliance with federal tax laws and to avoid any legal repercussions. Filing this form is a requirement for lenders, as it serves as a notice to borrowers and the IRS of the event of foreclosure or abandonment.

IRS Guidelines

The IRS provides guidelines to ensure the correct use of Form 1099-A. These guidelines detail the responsibilities of the lender to report the transaction and clarify how borrowers should utilize this form to report gains or losses when filing taxes. The IRS guidelines emphasize the importance of using accurate and current information when completing the form, and they outline the deadlines for submitting it.

Filing Deadlines / Important Dates

Lenders are required to file Form 1099-A to the IRS and provide a copy to the borrower by the end of January following the year of acquisition or abandonment. This deadline ensures that borrowers have the necessary information for their tax returns. Missing these deadlines can lead to penalties for lenders, emphasizing the importance of timely filing.