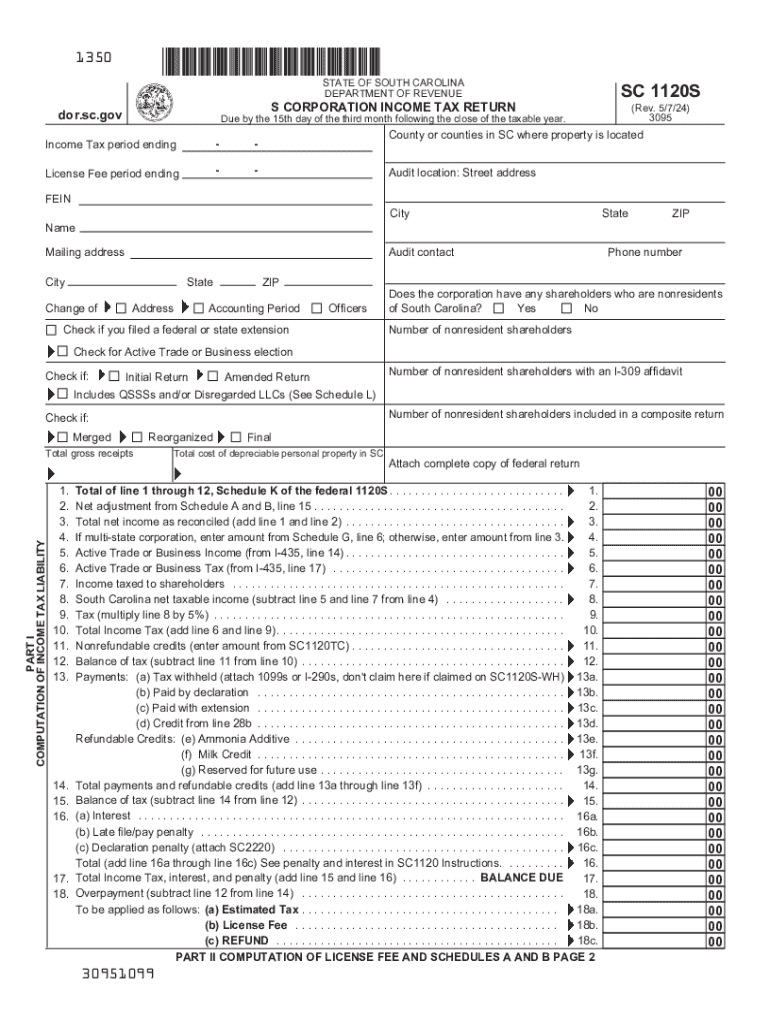

Definition and Meaning of SC1120S

The SC1120S form is the South Carolina S Corporation Income Tax Return. It is specifically designed for S corporations operating within South Carolina to report their income, calculate taxable income, determine license fees, and provide necessary corporate information. This form assists in ensuring compliance with state tax regulations, enabling corporations to meet their fiscal responsibilities efficiently.

How to Use SC1120S 3095

To use the SC1120S 3095 form effectively, begin by gathering all pertinent financial documentation related to the corporation's income and expenses. This form requires detailed entries for gross receipts, deductions, and other financial activities of the corporation. Ensure that all sections are completed accurately to avoid potential legal or financial complications. It is advisable to review the instructions provided with the form for any specific guidelines on filling each section.

Steps to Complete the SC1120S 3095

- Gather Required Information: Collect all financial documents, such as balance sheets and income statements, that reflect the corporation's annual financial activities.

- Complete Corporate Information: Enter the corporation's name, address, and employer identification number.

- Report Gross Receipts: Input the corporation's total gross receipts for the taxable year.

- Calculate Taxable Income: Deduct permissible expenses from gross receipts to determine the taxable income.

- Determine License Fees: Use the form's instructions to compute any applicable state license fees based on the corporation's income.

- Review and Sign: Verify that all information is accurate, and obtain the signatures required for submission.

Filing Deadlines and Important Dates

The SC1120S must be filed by the 15th day of the third month following the close of the taxable year, aligning with federal deadlines to facilitate streamlined tax management for corporations in South Carolina. Corporations should be aware of these timelines to ensure timely submission and avoid late penalties.

Who Typically Uses the SC1120S 3095

This form is predominantly used by South Carolina-based S corporations. These entities elect to pass corporate income, losses, deductions, and credits through to their shareholders for federal tax purposes, allowing them to avoid double taxation. Companies engaging in various industries, such as manufacturing, services, or retail operating as S corporations, will find this form essential for compliance.

Taxpayer Scenarios and Eligibility Criteria

To be eligible to file the SC1120S, a corporation must have elected to be an S corporation at the federal level and meet South Carolina's requirements for transacting business within the state. The form is designed for companies that have no more than one hundred shareholders, all of whom must be eligible individuals or certain trusts and estates.

Examples of Using the SC1120S 3095

Consider a South Carolina-based tech startup classified as an S corporation. This entity would use the SC1120S form to report its annual taxable income, which might include revenue from software sales minus deductions for business expenses like research and development. Another example could be a regional restaurant chain structured as an S corporation, leveraging the form to calculate license fees based on its annual gross sales.

Penalties for Non-Compliance

Failure to file the SC1120S on time may result in penalties ranging from late fees to interest charges on unpaid taxes. Additionally, inaccuracies or omissions can lead to audits or additional assessments. It is critical for corporations to adhere to all form guidelines and deadlines to avoid operational disruptions or legal challenges.

Form Submission Methods

Corporations can submit the SC1120S form via multiple channels:

- Online: Through the South Carolina Department of Revenue's online portal, offering a fast and secure method.

- Mail: By sending a printed version to the state department's address, providing a traditional approach for those who prepare documents manually.

- In-Person: Submission may be possible at designated state revenue offices, though this method typically requires prior appointment and checking whether the service is available.