Definition and Meaning

The -114 7 UBT Paid Credit 61112391 is designed to assist partners in partnerships to claim credits against their Unincorporated Business Tax (UBT) liability. This form allows partners to offset their tax obligations by utilizing credits based on their share of the partnership's income, gains, losses, and deductions. The purpose is to ensure that partnerships accurately account for UBT paid and to facilitate effective tax management for individuals and businesses engaged in such entities.

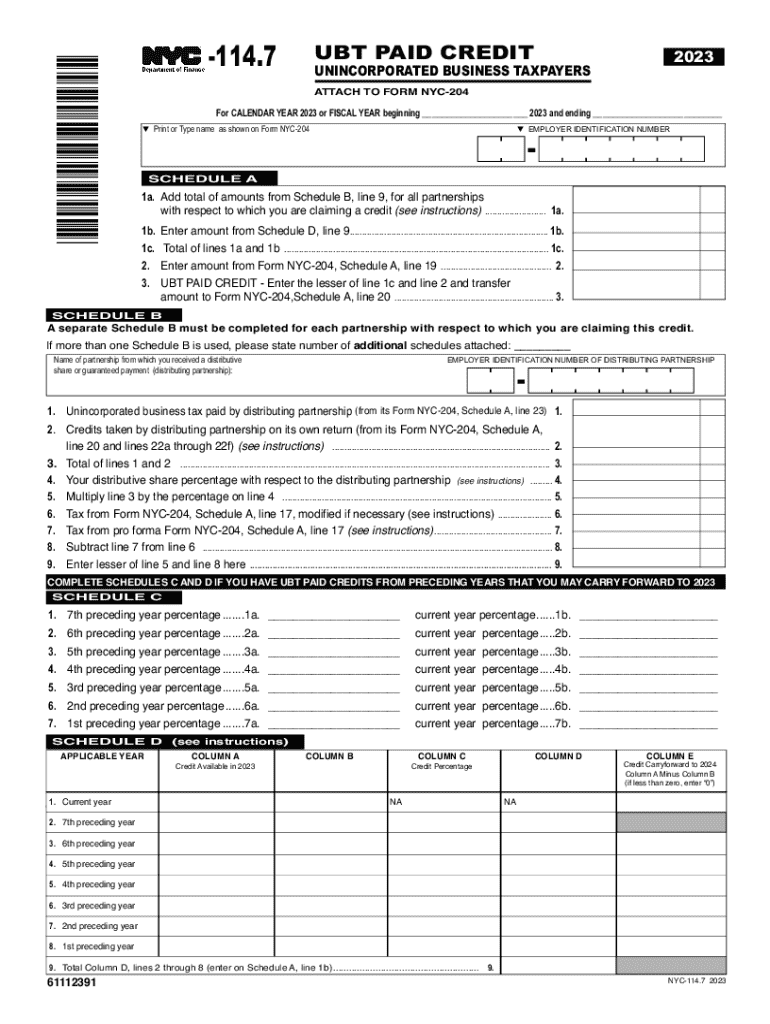

How to Use the -114 7 UBT Paid Credit

To effectively use the -114 7 UBT Paid Credit, partners need to determine their distributive share of the partnership's financial outcomes. This involves:

- Calculating Income and Losses: Assess the income and losses distributed by the partnership to the individual partner.

- Utilizing Schedules: Complete the necessary schedules (A, B, C, and D) to document and justify the UBT paid and credits claimed.

- Submitting the Form: Ensure all required information is accurately recorded and submit the form along with your tax return.

Steps to Complete the -114 7 UBT Paid Credit

Completing the -114 7 UBT Paid Credit form requires careful attention to detail. Here is a step-by-step guide:

- Gather Necessary Financial Information: Collect data on the partnership's income, losses, gains, and deductions.

- Fill Out Relevant Schedules:

- Schedule A: Calculate and enter the partnership's UBT paid.

- Schedule B: Document any carryforward credits from previous years.

- Schedule C and D: Provide additional calculations and justifications.

- Review and Verify: Double-check all entries for accuracy and completeness.

- Submission: File the form as part of your tax return package by the appropriate deadline.

Key Elements of the -114 7 UBT Paid Credit

The -114 7 UBT Paid Credit form consists of several key components:

- Partnership Information: Details about the partnership and its operations.

- Schedules for Credit Calculation: Comprehensive sections that outline credit eligibility and calculation.

- Carryforward Provisions: Sections that address the handling of credits from previous years.

Who Typically Uses the -114 7 UBT Paid Credit

Typical users of the -114 7 UBT Paid Credit form include:

- Partners in Business Partnerships: Those engaged in profit-sharing setups that fall under unincorporated business structures.

- Tax Professionals: Accountants and tax consultants managing tax obligations for clients in partnerships.

- Small to Medium-sized Business Owners: Individuals who rely on accurate tax credit claims to optimize their tax situations.

IRS Guidelines

The IRS provides specific guidelines surrounding the use of the -114 7 UBT Paid Credit. These include:

- Eligibility Criteria: Not all partnership forms are eligible; adherence to established criteria is necessary.

- Submission Deadlines: Mandatory filing dates to ensure compliance and avoidance of penalties.

- Documentation Requirements: Detailed records of income, gains, losses, and tax credits must be kept for verification.

Filing Deadlines and Important Dates

Partnerships and partners need to be aware of crucial filing deadlines associated with the -114 7 UBT Paid Credit:

- Year-End Documentation: Compile all relevant financial records before the fiscal year-end.

- April 15 Deadline: Typically aligns with federal tax filing deadlines unless extensions apply.

- Extension Application Dates: Dates by which to apply for extensions if additional time is required to complete the form.

Penalties for Non-Compliance

Failing to comply with -114 7 UBT Paid Credit requirements can result in significant repercussions:

- Financial Penalties: Fines and interest accrued on unpaid taxes due to erroneous credit claims.

- Legal Implications: Potential audits or legal action from the IRS for deliberate non-compliance.

- Reputational Impact: A history of non-compliance may influence business credibility and partnership opportunities.

Form Submission Methods

The -114 7 UBT Paid Credit can be submitted through various channels:

- Online Filing: Preferred for efficiency and speed, using authorized e-filing platforms.

- Mail Submission: Traditional method, ensuring all documents are properly addressed and posted.

- In-Person Delivery: Direct submission to IRS centers where applicable, ensuring receipt confirmation.

Eligibility Criteria

To qualify for the -114 7 UBT Paid Credit, applicants must ensure:

- Correct Partnership Type: Validation that the partnership is an eligible unincorporated business entity.

- Accurate Income Reporting: Full transparency and correctness in reporting financial outcomes.

- Compliance with Tax Laws: Adherence to all relevant laws and regulations governing UBT and related credits.