Definition and Meaning

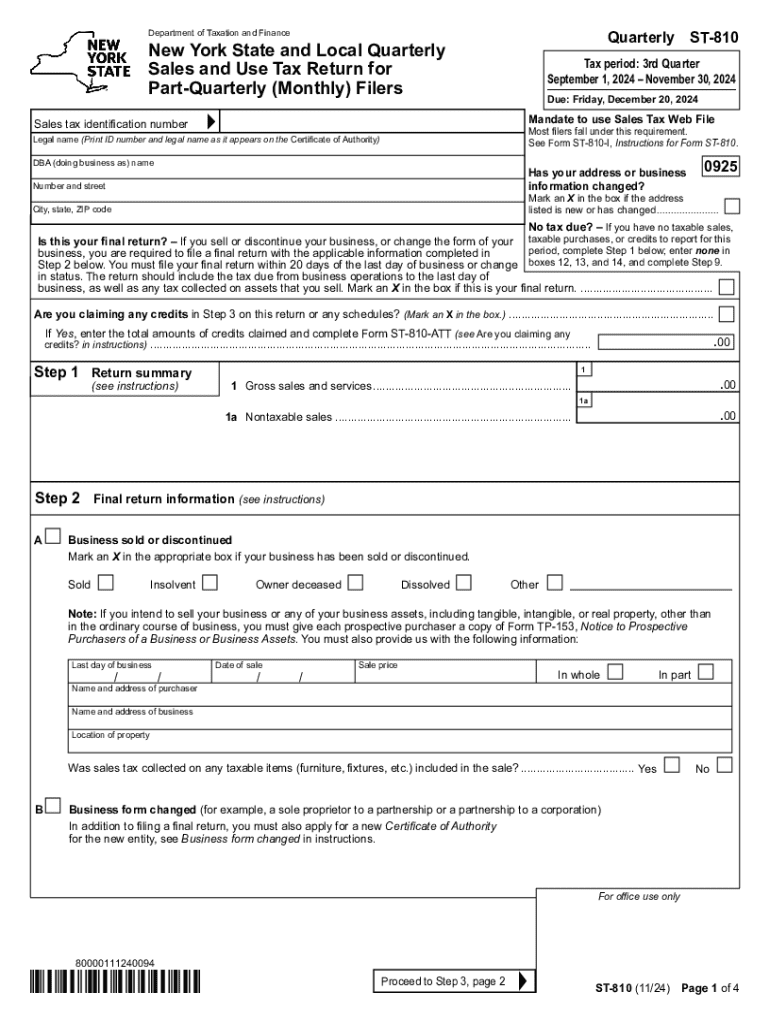

The Form ST-810, known as the New York State and Local Quarterly Sales and Use Tax Return for Part-Quarterly Filers, is a specific tax document used primarily by businesses operating in New York State. This form is designed for businesses required to report and remit sales and use tax on a quarterly basis, specifically within a part-quarterly filing schedule. This means that it serves businesses that have significant sales tax obligations, often caused by the volume or nature of their sales, and thus must report more frequently to remain compliant.

Key Elements of the Form ST-810

Completing the Form ST-810 requires detailed knowledge of several key elements. The form necessitates the inclusion of various critical details:

- Tax Identification Number: This is crucial for identifying the submitting business.

- Business Details: Includes the company's name, address, and relevant contact information.

- Sales and Use Tax Amounts: Detailed figures of taxable sales, use taxes due, and any applicable exemptions must be accurately reported.

- Credit Claims: Businesses can report credits they are eligible for, which may reduce their overall tax liability.

Steps to Complete the Form ST-810

A thorough understanding of each step is necessary for accurately completing the form:

- Gather Required Documents: Collect all sales records, purchase invoices, and any previous tax filings essential for completing the form.

- Complete the Identification Section: Fill out your tax identification number and business information clearly as inaccuracies here can lead to penalties.

- Report Sales Tax: Enter figures for taxable sales made during the period, applying any applicable exemptions.

- Calculate Use Tax: Include any taxes due on out-of-state purchases that did not have sales tax applied.

- Claim Credits: Carefully calculate and document any eligible credits, ensuring they match your records.

- Finalize and Submit: Review all entries for accuracy before submitting, ensuring all required fields are filled and supporting documents are attached if necessary.

Filing Deadlines and Important Dates

It is essential to adhere to the predefined deadlines to avoid penalties:

- Quarterly Schedule: Typically, reports are due by the 20th of the month following the end of the reporting quarter.

- Extended Deadlines: In certain circumstances, businesses may apply for extensions, but it is crucial to understand the specific conditions under which extensions are granted.

Who Typically Uses the Form ST-810

The primary users are businesses obligated to file quarterly tax returns due to their intensive sales activities within New York. This encompasses:

- Retailers: Businesses with significant customer sales volume.

- Manufacturers and Distributors: Companies dealing with large transactions and reselling goods in New York.

- Service Providers: Those offering taxable services that accrue sales tax obligations.

Important Terms Related to Form ST-810

Understanding key terms is critical for proper form completion:

- Taxable Sales: The total sales amount that is subject to state and local sales taxes.

- Use Tax: A tax from purchases made out-of-state for use within New York, where sales tax has not been paid.

- Exemptions: Specific transactions that are not subject to sales tax based on state legislation.

Legal Use of the Form ST-810

The form enforces legal compliance for businesses operating within New York state:

- Ensuring Tax Obligation Fulfillment: It serves as proof of a business's adherence to state tax laws.

- Protection Against Penalties: Accurate and timely filing mitigates risks of financial penalties and audits.

Penalties for Non-Compliance

Failure to file accurately and on time can lead to:

- Monetary Fines: Penalties proportionate to unpaid taxes, often initiated by late submission or inaccurate reporting.

- Legal Action: Continued non-compliance can lead to further investigations or legal pursuits by tax authorities.

State-Specific Rules for New York

New York's rules for sales and use tax have unique aspects:

- Local Variations: Tax rates can vary by county, necessitating accurate county-specific reporting.

- Exemption Criteria: Certain goods or services may have state exemptions, which do not apply elsewhere.

By covering these essential blocks, businesses can ensure they're fully prepared for the reporting requirements of the Form ST-810. Proper completion reflects an understanding of New York's tax obligations and at the same time mitigates any risks associated with non-compliance.