Definition and Meaning

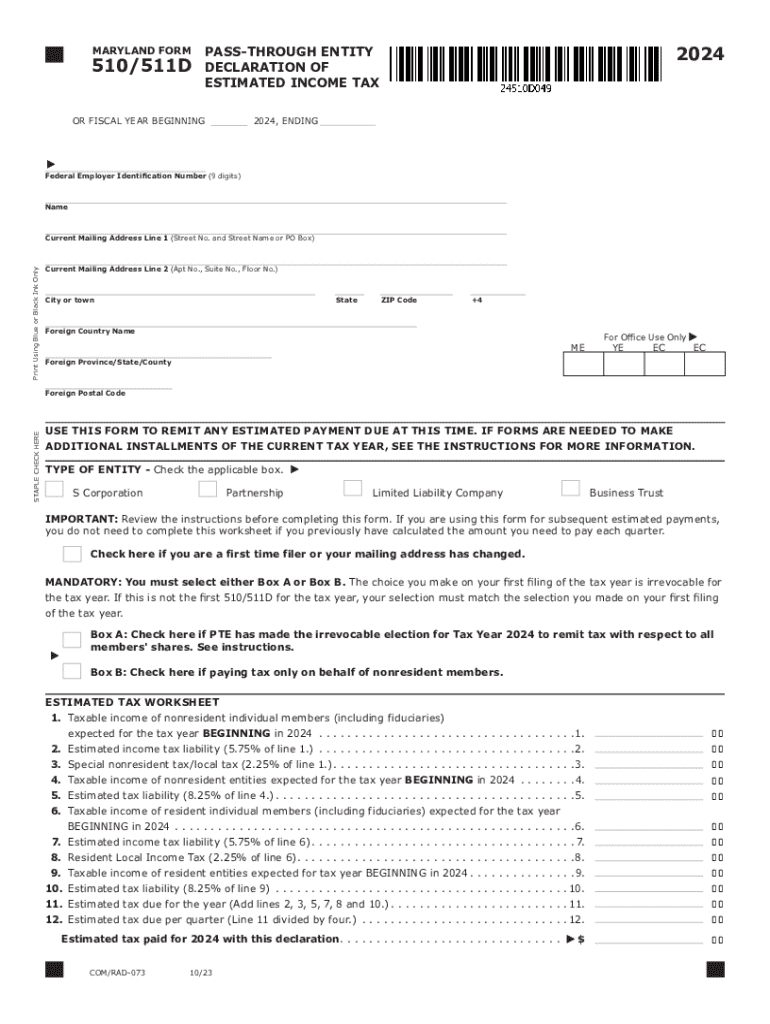

The Maryland Form 510/511D, commonly referred to as Form 510D, is a crucial document for pass-through entities (PTEs) such as partnerships, S-corporations, and limited liability companies in Maryland. This form is a declaration used to report and remit estimated income tax liabilities for the calendar year 2024. It allows PTEs to elect whether to pay taxes on behalf of all members or only on behalf of nonresident members. Understanding this form is essential for the accurate reporting of income and tax obligations, ensuring compliance with state tax regulations.

How to Use the Maryland Form 510D

Completing the Maryland Form 510D involves several steps. Below is a structured approach:

- Gather Required Information: Start by collecting necessary details such as the entity’s Federal Employer Identification Number (FEIN), business name, and address.

- Estimate Income and Tax: Calculate the estimated taxable income for the year. This involves reviewing past financial records and forecasting future earnings.

- Allocate Member Shares: Determine the share of income attributable to each member of the PTE to accurately assess tax obligations.

- Complete the Worksheet: Use the form's worksheet to calculate estimated taxes based on your income projections.

- Filing the Form: Submit the completed form to the Maryland Comptroller’s office. The form must be filed by the due date to avoid penalties.

Steps to Complete the Maryland Form 510D

To fill out the Maryland Form 510D efficiently, follow these detailed steps:

- Identify the Reporting Period: Choose the correct tax period for which the form is being filed.

- Calculate Estimated Liabilities: Use the worksheet included in the form to compute your estimated tax liability.

- Select Payment Method: Decide if payments will be made on behalf of all members or only for nonresident members, then enter the total estimated payment amount.

- Review for Accuracy: Double-check all entries to ensure that calculations and personal/business information are correct.

- Submit the Form: Send the document to the appropriate state tax office by the specified deadline.

Key Elements of the Maryland Form 510D

Understanding the core components of Form 510D can enhance its accurate completion:

- Entity Information: Includes the FEIN, name, and address of the entity.

- Member Distribution: Details concerning each member’s share of income and corresponding tax payments.

- Tax Calculation Worksheet: A worksheet provided within the form to aid in calculating estimated payment amounts.

- Signature and Date: An attestation section validating the form with signatures and the submission date.

Important Terms Related to Maryland Form 510D

Familiarity with specific terms can aid in successfully navigating Form 510D:

- Pass-Through Entity (PTE): Business structures that pass tax obligations to individual members, avoiding corporate taxes.

- Estimated Tax Amount: The projected tax payment for a given period, based on expected income.

- Nonresident Member: A member of the PTE who does not reside within the state of Maryland but is subject to state tax on earned income.

State-Specific Rules for the Maryland Form 510D

Maryland state tax rules influence how Form 510D is used:

- Obligation for Nonresident Members: PTEs must remit taxes on behalf of nonresident members unless an exemption applies.

- Filing Deadlines: Adherence to state-defined deadlines is essential to avoid penalties and ensure tax obligations are met.

Filing Deadlines / Important Dates

- Quarterly Estimated Payments: The state of Maryland requires estimated payments to be made quarterly. Typically, due dates are April 15, June 15, September 15, and January 15 of the following year.

Penalties for Non-Compliance

Failing to file or pay estimated taxes using Form 510D can result in penalties:

- Late Payment Penalty: If the estimated payments are not made by their respective due dates, penalties may be applied.

- Underpayment Penalties: When the estimated tax payments are substantially lower than the actual taxes due, underpayment penalties may be assessed.