Definition and Meaning of IRS Form 4180

IRS Form 4180 is utilized primarily during the interview process by the Internal Revenue Service to gather extensive details regarding an individual's involvement with a business's tax obligations. This form is essential in assessing whether individuals such as business owners or responsible officers should be held liable for trust fund recovery penalties due to unpaid excise taxes. Key sections of the form include personal information, business information, and an individual's understanding of their tax responsibilities, allowing for a comprehensive evaluation of their role in decision-making processes related to tax compliance.

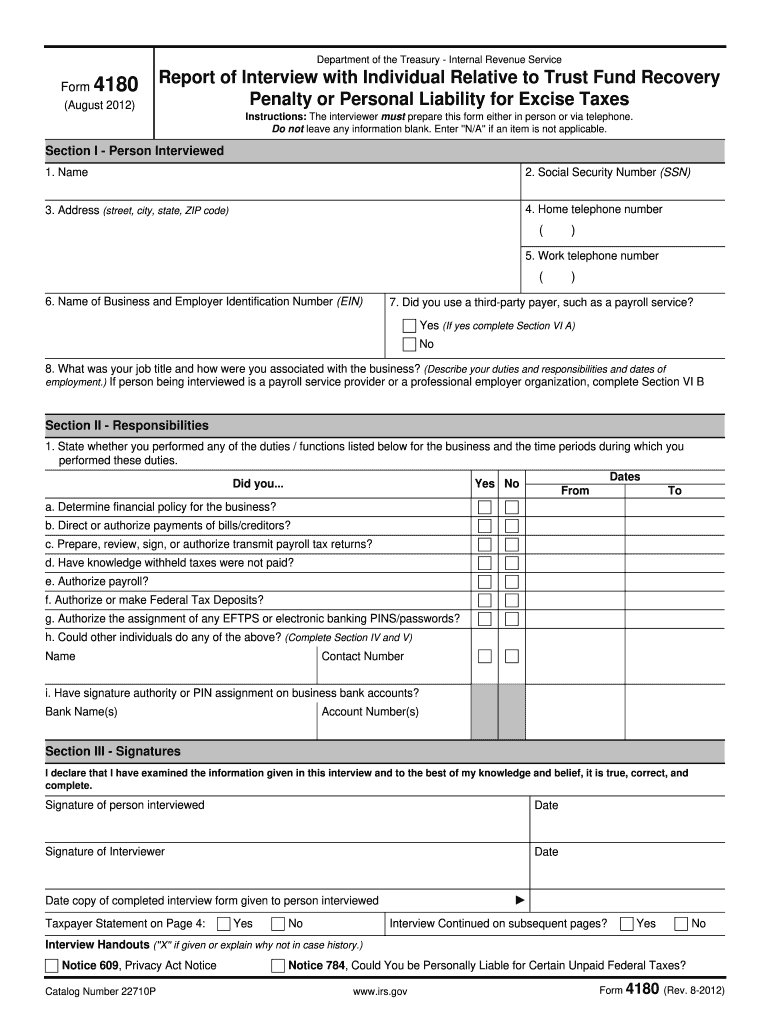

Key Elements of IRS Form 4180

-

Personal Information: This section gathers necessary personal details about the interviewee, such as their full name, address, and social security number. Providing accurate information is crucial for maintaining precise records and ensuring proper identification.

-

Responsible Person Involvement: The form delves into the individual's specific responsibilities and duties within the business, focusing on aspects like their role in financial decisions and who is authorized to sign checks or make financial transactions.

-

Business Details: Information about the business, including its name, address, tax withholding ID, and organizational structure, is collected. This section ensures that the IRS has an accurate profile of the entity in question.

-

Understanding of Tax Obligations: The form inquires about the individual's knowledge of the business's tax obligations, including payroll taxes and filing practices, to determine their awareness and involvement in potential tax discrepancies.

How to Use IRS Form 4180

The IRS Form 4180 is used by the IRS to interview individuals potentially responsible for unpaid taxes. During the interview process, IRS agents will use this form to confirm the roles and duties of individuals regarding tax obligations and determine if penalties should be applied.

Interview Process

Interviews are generally conducted in person or over the phone. The IRS may also request supporting documents, such as financial statements or payroll records, to verify the details provided. Individuals should be prepared to explain their specific duties and involvement in tax-related decisions thoroughly.

Completing the Form

When filling out the form, be sure to:

- Provide accurate and complete information in each section

- Clearly describe your duties in the organization, especially concerning financial management

- Highlight any delegation of tax-related duties to other team members

Steps to Complete IRS Form 4180

-

Gather Necessary Information: Collect all relevant personal, business, and financial information required for form completion. Accurate data ensures the form is executed correctly.

-

Detail Personal Responsibilities: Clearly outline your role in the business, focusing on decision-making processes related to taxes and financial management.

-

Provide Business Information: Include comprehensive details about your organization such as business name, structure, and Employer Identification Number (EIN) to facilitate accurate IRS records.

-

Demonstrate Knowledge of Tax Matters: Articulate your understanding of payroll and tax obligations to address potential IRS concerns about compliance.

-

Review and Submit: Double-check all entered information for accuracy and submit the form following IRS guidelines, either via mail or in-person during an audit meeting.

Important Terms Related to IRS Form 4180

Understanding the specific terms associated with IRS Form 4180 is crucial for proper form completion. Important terminology includes:

- Trust Fund Recovery Penalty (TFRP): A significant penalty imposed on business officers and owners found responsible for unpaid federal taxes.

- Federal Employment Taxes: Taxes withheld from employees' wages, including Social Security and Medicare taxes, for which businesses are responsible.

Other Relevant Terms

- Responsible Person: Any individual or officer who has the duty to perform and the power to direct the collecting, accounting, and paying of trust fund taxes.

- Payroll Taxes: Taxes imposed on employers or employees, usually calculated as a percentage of the salaries that employers pay their staff.

IRS Guidelines and Eligibility

The IRS imposes specific guidelines on who can be held accountable for unpaid taxes through Form 4180. Typically, individuals such as owners, officers, or employees with significant decision-making authority are scrutinized.

Determining Eligibility

- Financial Responsibility: Only those who had control over financial decisions and tax payments are considered responsible persons.

- Knowledge and Willful Failure: To be deemed liable, the person must have been aware of the unpaid tax obligations and willfully chose not to comply.

Penalties for Non-Compliance

Non-compliance with tax obligations can result in steep penalties:

- Trust Fund Recovery Penalties (TFRP): These penalties can be personally imposed on those identified as responsible persons.

- Interest Charges: Additional fees may accrue on due taxes from the date they were supposed to be paid.

Penalties are severe, and avoiding them requires a clear understanding of and adherence to tax obligations. Businesses and individuals are encouraged to maintain up-to-date and accurate records to avoid misunderstandings with the IRS.

Required Documents for IRS Form 4180

When preparing for the IRS interview, certain documents may be requested for submission:

- Financial Statements: Income statements and balance sheets to provide a detailed overview of business finances.

- Payroll Records: Comprehensive payroll documentation showing how and to whom payments have been made within the company.

- Corporate Minutes and Resolutions: Documents indicating who within the company holds the authority to make financial decisions.

Maintaining accurate records is vital to support assertions made during the IRS interview process, helping individuals to avoid penalties related to misinformation or discrepancies.

Examples of Using IRS Form 4180

Case Example: Small Business Owner

A small business owner responsible for payroll decisions is found to have missed multiple payroll tax deadlines. During the IRS interview, the owner completes Form 4180 to demonstrate that another officer was delegated this responsibility, potentially mitigating personal liability for tax penalties.

Case Example: Financial Officer

A financial officer at a mid-sized corporation is questioned regarding the mismanagement of withheld payroll taxes. Through Form 4180, they illustrate that payroll processes were outsourced to a third-party service, which may shift the focus of responsibility away from the officer.

By understanding the intricate details captured in Form 4180 and depicting it through examples, businesses and individuals can better navigate the compliance obligations imposed by the IRS.