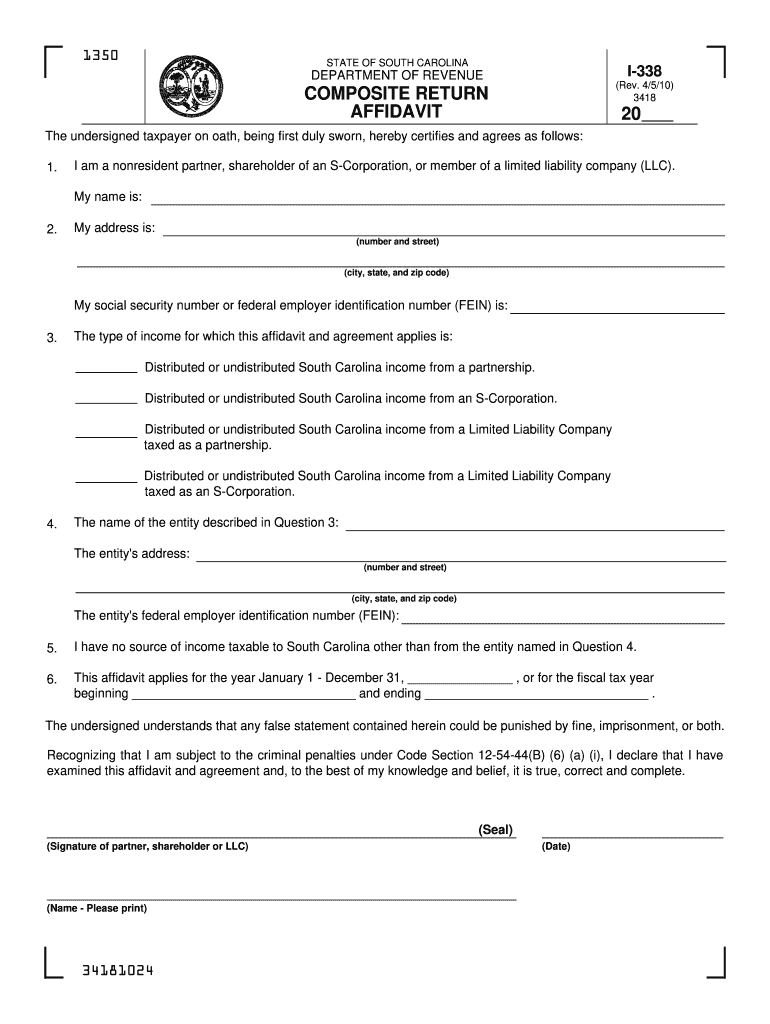

Definition and Purpose of the I-338 Composite Return Affidavit

The I-338 Composite Return Affidavit, specific to South Carolina, is integral for nonresident partners, shareholders of S-Corporations, and LLC members. This document certifies income sources for tax purposes without their direct filing. It aids in filing composite returns collectively, presenting two methods for calculating South Carolina income tax. The affidavit acts as an annual document essential for maintaining compliance with state tax regulations.

Obtaining the I-338 Form

To acquire the I-338 form, the South Carolina Department of Revenue is the primary source. Forms can be downloaded directly from their official website, ensuring you have the most current version. For those preferring traditional methods, paper copies may be requested by contacting the department. Consulting with a tax advisor or legal professional can also facilitate this process, especially for newcomers to the South Carolina tax landscape.

Steps to Complete the I-338 Form

Filing the I-338 involves several meticulous steps.

- Gather Necessary Information: Require identification details of all participants, including names, addresses, and taxpayer identification numbers.

- Compile Income Sources: Accumulate data on income relevant to South Carolina taxation, ensuring accuracy.

- Determine Tax Calculation Method: Choose between the apportionment method or special income tax computations as outlined in the form.

- Complete Affidavit: Fill out the affidavit carefully, adhering to guidelines for each section. This includes specifying each participant's role and income allocation.

- Review and Sign: After completion, thorough checking is crucial before application of authorized signatures.

- Submit Form: Submission may be done electronically if the infrastructure supports it or by mail to designated addresses.

Who Typically Uses the I-338 Form

The I-338 is predominantly used by nonresident entities in partnership with South Carolina-based businesses. Owners or partners of S-Corporations, LLCs, or partnership members who are not residents of South Carolina are primary users. This system streamlines tax filing, particularly for those outside the state yet generating income within it. It significantly reduces individual filing demands, offering a collective approach to tax compliance.

Key Elements of the I-338 Form

Key elements integral to the successful completion of the I-338 form include the participant information sections, which capture all affiliated parties and their respective income figures. The income allocation section is vital for outlining each participant's share of the total income subjected to South Carolina taxation. Another crucial component is the method selection area, dictating the tax calculation approach and the summarized total tax liability.

State-Specific Rules for Utilizing the I-338 Form

The I-338 is bound by South Carolina-specific tax laws and regulations. Participants must adhere strictly to the state's composite return rules, requiring the group to collectively agree on filing this form. Rules dictate that tax payments are based on the aggregate income computed within the state, presenting unique obligations compared to direct individual filings in other jurisdictions.

Legal Use and Compliance of the I-338 Form

Utilizing the I-338 form requires adhering to legal compliance with the state’s tax codes. It represents a formal agreement among nonresident participants and the South Carolina Department of Revenue, ensuring no individual participant can claim exemption from compliance under this model. Legal disputes or inaccuracies in reporting can lead to audits or penalties, underscoring the importance of exact compliance.

Important Terms Related to the I-338 Form

Familiarizing oneself with terms like "composite return," which denotes the group's collective tax filing, and "apportionment method," a way of dividing income across jurisdictions, is essential. Understanding "participant" in context refers to each individual's role in the structure, whether as a nonresident partner, shareholder, or member. Clarity on these terms aids in navigating the form accurately.

Submission Methods for the I-338 Form

Submission methods for the I-338 afford both traditional and modern options. While online submission introduces efficiency and quick turnaround, paper submissions remain acceptable, catering to different user preferences. Mailing the completed form to designated state departments remains a reliable method for those who opt for a paper trail. Confirmation of receipt via certified mail is advisable where possible.