Understanding Material Participation in Business Operations for 2016

Material participation refers to an individual's active engagement in a business during the year 2016. It is vital for determining specific tax implications and whether an individual's business activities can be classified under non-passive income, affecting eligibility for certain deductions and credits. The IRS defines material participation through several quantitative and qualitative tests, which vary based on time spent and the nature of involvement in the business operations.

Steps to Prove Material Participation in 2016

-

Track Your Hours:

- Ensure you track time accurately, quantifying if you worked more than 500 hours during the year.

- Compile any records or logs that can substantiate this involvement.

-

Review Involvement Levels:

- Consider whether your involvement was the only active participation in the business.

- Take account of whether you effectively controlled the business operations without delegating most tasks.

-

Document Management Decisions:

- Record key management decisions, highlighting your active role in decision-making and business strategies.

Importance of Material Participation in 2016 Business Operations

Understanding material participation is crucial because it impacts your tax filings and financial responsibility:

- It determines whether your income is active or passive, affecting how it is taxed.

- Active participants can enjoy deductions on losses, which might not be available for passive participants.

Who Typically Establishes Material Participation

Material participation is often a concern for business owners, self-employed individuals, and stakeholders in small businesses:

- Small Business Owners: Need to differentiate between passive investments and active incomes for tax purposes.

- Self-Employed Individuals: Determine their tax liabilities accurately by proving their active role in the business.

IRS Guidelines for Material Participation

The Internal Revenue Service (IRS) has established tests to verify if you materially participated in 2016:

- Meeting Time Requirements: More than 500 hours participating in the business.

- The Exact Tasks: Engaged in regular, continuous, and substantial business operations.

- Exclusivity of Participation: If no other individual had worked more on the business than you.

Legal Implications of Material Participation

Properly documenting material participation ensures compliance with tax laws:

- Non-Compliance Penalties: Failing to document can lead to fines, audits, and adjustments in your declared income.

- Deductions and Credits: Only those meeting the material participation criteria can avail certain IRS tax benefits.

Documentation Needed to Prove Material Participation

- Timesheets or Logs: Showing hours worked throughout the year.

- Business Records: Meeting notes, business decisions documentation, logs of business trips.

- Financial Records: Demonstrating active management of income, costs, and profits.

How to Acquire and Use Relevant Forms

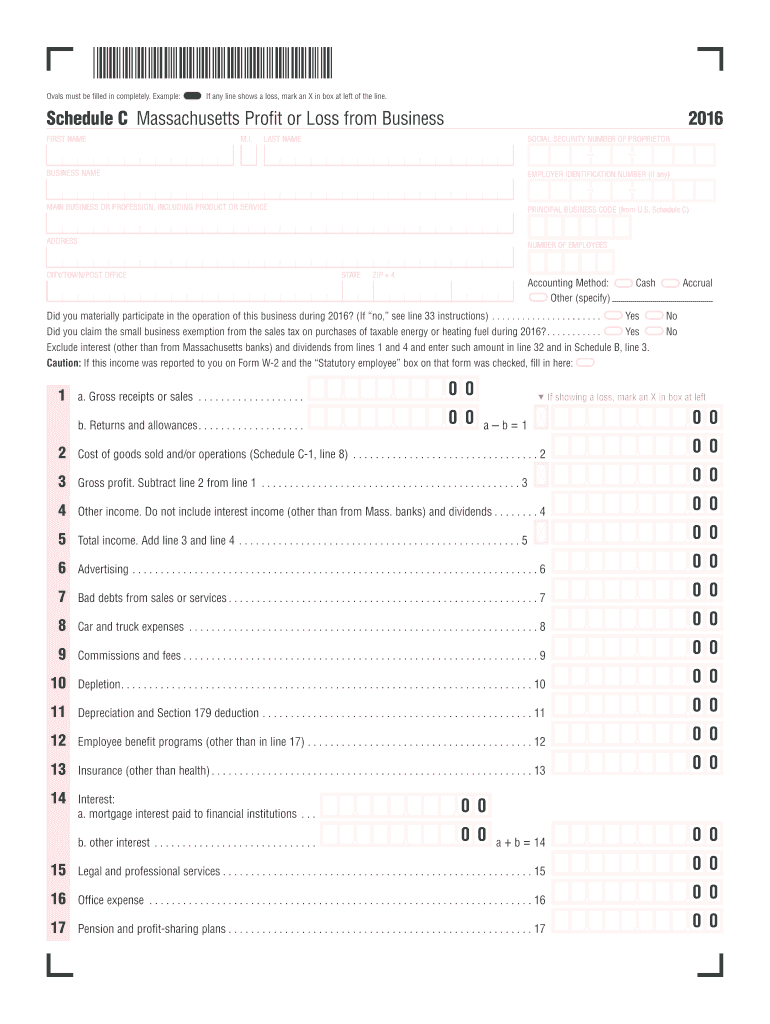

The form related to documenting your participation typically involves a Schedule C for reporting profit and loss from business activities. Here's how you use it:

- Acquisition: Obtain forms either from the IRS website or through tax preparation software.

- Usage: Report on income, expenses, and detail your involvement within the designated sections.

Key Takeaways on Material Participation in 2016

- Understanding Standards: Familiarize yourself with the IRS tests to determine material participation.

- Thorough Documentation: Keep comprehensive records as proof of your involvement for auditing purposes.

- Implications for Deductions: Active participation grants certain financial advantages during tax assessments.

This comprehensive guide provides clarity on understanding and documenting material participation in a business for the year 2016, ensuring compliance with tax laws and benefiting from any available deductions and credits.