Definition and Meaning of CT-399-I

The CT-399-I form is a crucial document from the New York State Department of Taxation and Finance. It primarily assists corporations in calculating their entire net income by outlining the procedures for computing depreciation adjustments. This form is instrumental for companies seeking to align their federal and New York State depreciation deductions accurately. By understanding the CT-399-I, corporations can manage their depreciation modifications effectively, ensuring compliance with tax reporting requirements.

How to Use the CT-399-I

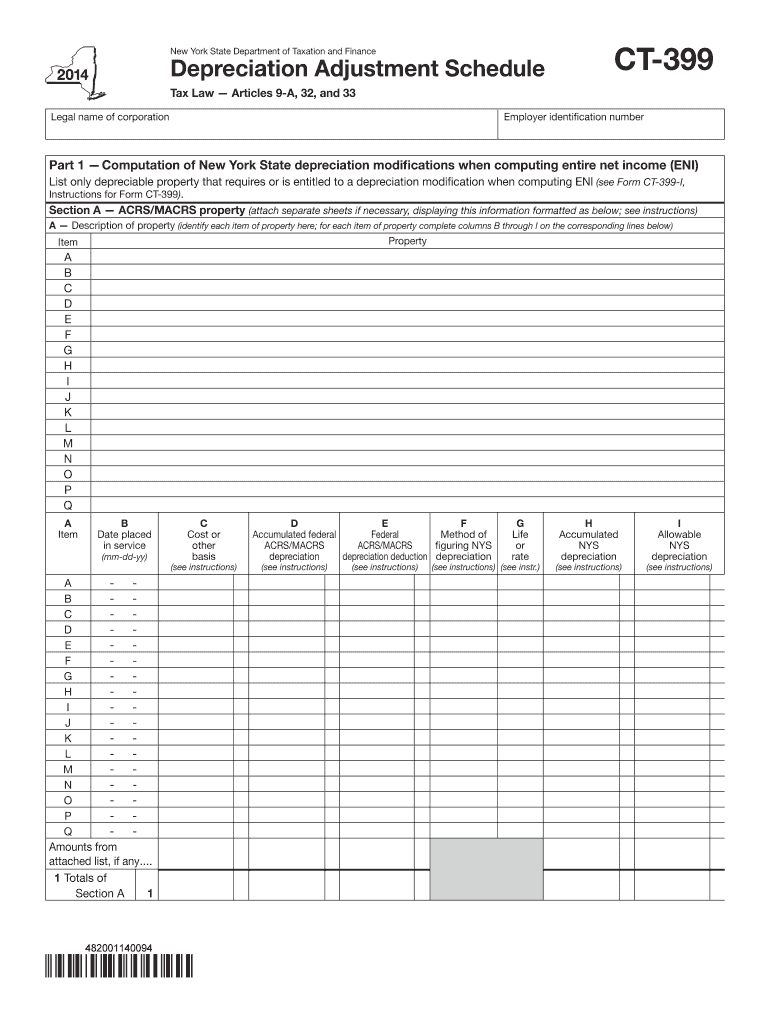

When using the CT-399-I form, corporations need to detail depreciable property and indicate both federal and New York State depreciation deductions. Key steps involve:

- Listing Depreciable Assets: Begin by cataloging all assets subject to depreciation.

- Federal Depreciation Deduction: Enter the depreciation deduction claimed federally for each asset.

- State Depreciation Deduction: Note the depreciation deduction according to New York State law.

- Adjustment Calculations: Calculate any necessary adjustments related to property dispositions or other changes affecting depreciation.

This detailed approach allows corporations to accurately present depreciation data in their tax filings.

Steps to Complete the CT-399-I

- Gather Relevant Financial Data: Collect information about all assets in use, including their cost and date of acquisition.

- Identify Depreciation Methods: Determine the methods used for depreciation under both federal and state guidelines.

- Complete Asset Listing: Accurately complete sections detailing each asset's depreciation.

- Calculate Adjustments: Make adjustments for any discrepancies between federal and state depreciation methods.

- Review and Verify: Ensure all information matches financial records before submission.

This process ensures the most accurate and compliant submission of the CT-399-I form.

Important Terms Related to CT-399-I

- Depreciable Property: Assets that are eligible for depreciation deductions over time.

- Net Income: Total income minus expenses, which includes depreciation adjustments.

- Depreciation Deduction: The reduction in taxable income reflecting the wear and tear of property over time.

- Depreciation Adjustment: Modifications made to account for differences in federal and state depreciation reporting.

Understanding these terms is critical for completing the CT-399-I accurately.

Legal Use of the CT-399-I

The CT-399-I form is a legal document mandating accurate reporting of depreciation for tax purposes. Corporations must adhere to both federal and New York State guidelines when completing this form to ensure compliance and avoid potential legal issues. Proper use of the CT-399-I helps in maintaining accurate financial records and minimizing the risk of audits or penalties.

Who Typically Uses the CT-399-I

Corporations operating in New York State primarily use the CT-399-I form. This document is essential for businesses that own significant amounts of depreciable property and need to reconcile depreciation differences between federal and state tax guidelines. Both large enterprises and smaller corporations can benefit from accurately completing this form to optimize their tax liability.

Filing Deadlines and Important Dates

The CT-399-I form must be filed in conjunction with a corporation's annual tax return. It is imperative for businesses to be aware of the following:

- Tax Return Due Date: Typically aligns with the federal tax deadline, with possible extensions available.

- Estimated Payments: If applicable, estimated tax payments might also factor into timing considerations.

Missing these deadlines can result in penalties, so timely submission is crucial.

Key Elements of the CT-399-I

- Asset Details: Information on each piece of depreciable property.

- Depreciation Claimed: Federal and state amounts must be clearly indicated.

- Adjustments Required: Highlight any necessary modifications based on discrepancies between federal and state reporting.

- Compliance Evidence: Proper documentation supporting calculations and claims.

These elements ensure the form's comprehensive coverage of all necessary depreciation details.

Penalties for Non-Compliance

Failure to properly complete and submit the CT-399-I form can lead to several penalties:

- Monetary Fines: Imposed for inaccuracies or failures to file on time.

- Interest Charges: Accrued on any unpaid taxes due to incorrect depreciation reporting.

- Potential Audits: Increased likelihood of audits from both state and federal tax authorities.

Understanding these penalties emphasizes the importance of accuracy and adherence to deadlines when utilizing the CT-399-I.