Definition and Meaning

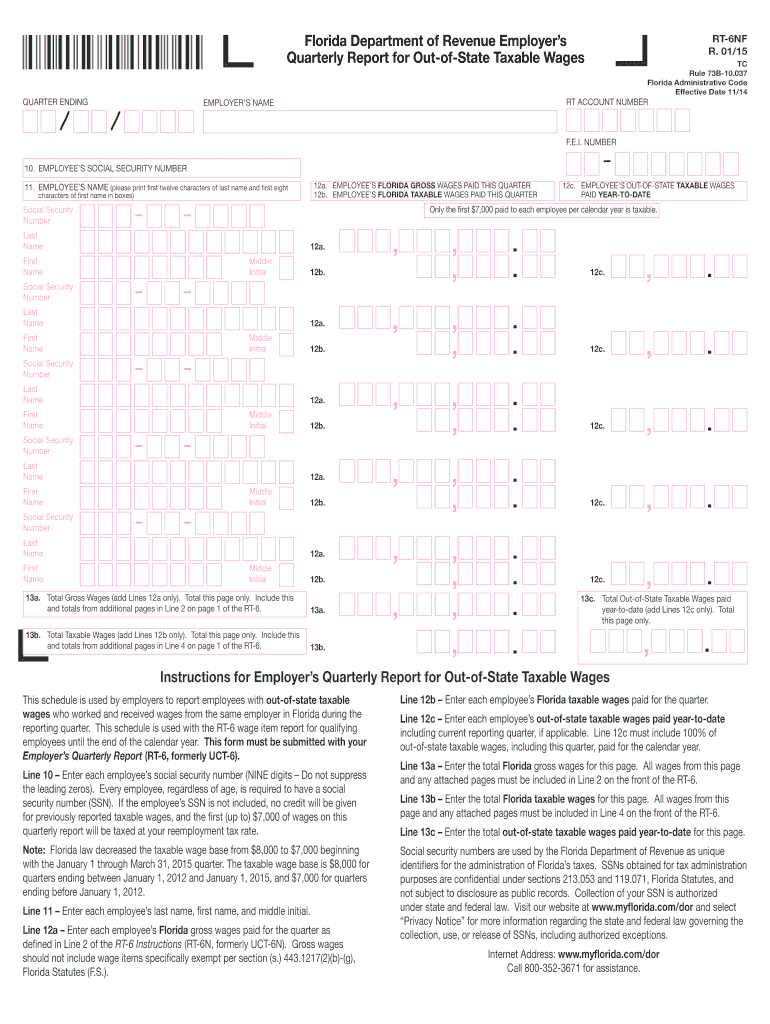

The RT-6, known within the Florida Administrative Code, is a crucial document used primarily for reporting employee wages. It serves as the Employer’s Quarterly Report for Out-of-State Taxable Wages. Employers based in Florida or those employing workers who earn wages while working in Florida need this form to report employees' out-of-state taxable wages. The document shares essential information to support the tax credit process and ensure adherence to Florida's tax laws.

Steps to Complete the RT-6 Form

- Gather Employee Details: Include information such as employee names, social security numbers, and gross wages.

- Calculate Taxable Wages: Differentiate between out-of-state wages and those taxable in Florida.

- Report Total Wages: Use the form to record the sum of taxable wages for all employees.

- Ensure Compliance: Confirm all data aligns with Florida tax laws before submission.

- Submit the Completed Form: Choose from online, mail, or in-person submission methods according to preference and access.

Key Elements of the RT-6

- Employee Information Section: Requires detailed listing of each employee's wages and other identifying information.

- Out-of-State Wages: A specified section to report wages earned by employees out of Florida, relevant for tax credit applications.

- Gross and Taxable Wages: Requires calculation and entry of total gross wages and how much of that is taxable under Florida law.

- Employer Identification Number (EIN): Each form must include this unique identifier for the filing business.

Who Typically Uses the RT-6 Form

Employers operating within Florida or having employees earning wages within the state use the RT-6. This could include corporations, partnerships, or sole proprietorships, ensuring they comply with state wage reporting requirements. It is especially pertinent for employers with employees performing services outside Florida but requiring tax details within the state.

Obtaining the RT-6 Form

To acquire the RT-6 form, businesses registered with the Florida Department of Revenue can download it from the department’s official website. Additionally, registered users can access it through their account portal or request it via email or phone. Business owners must ensure they access the latest version to remain compliant.

Important Terms Related to the RT-6

- EIN (Employer Identification Number): The IRS-issued number for identifying a business entity in wage reporting.

- Taxable Wages: The portion of employee wages subject to tax under Florida law.

- Out-of-State Wages: Wages earned by working outside Florida but reported for state tax purposes.

- Tax Credit: Deductions made available for reported out-of-state wages, ensuring businesses aren’t taxed unfairly.

Penalties for Non-Compliance

Failure to file the RT-6 or present erroneous information can lead to severe penalties including financial fines, accruing interest on delayed payments, and potentially further legal action from the Florida Department of Revenue. Ensuring the form’s timely and accurate submission is vital for avoiding these repercussions.

Required Documents

Employers must provide accurate employee records, payment proofs, and prior wage reports while completing the RT-6 form. Additionally, having prior year's tax filings, current wage calculations, and employee withholding information ensures the reporting is consistent and complete.

Digital vs. Paper Version

The RT-6 is available in both digital and paper formats, allowing flexibility for employers. The digital version permits easy online submissions through the Florida Department of Revenue portal, offering real-time confirmations and faster processing times. In contrast, the paper form offers familiarity for traditionalists preferring physical records. However, digital submissions are often recommended for their efficiency and security features.

Filing Deadlines

RT-6 is due quarterly, specifically on the last day of the month following the end of each quarter. Adherence to these dates is critical to avoid penalties. The quarterly deadlines are:

- April 30 for Q1 (January to March)

- July 31 for Q2 (April to June)

- October 31 for Q3 (July to September)

- January 31 for Q4 (October to December)